GLP-1 Cost With and Without Insurance (2026): What You'll Actually Pay

By WPG Research Team•Last Updated: April 10, 2026

Disclosure: Some links on this site are affiliate links. If you purchase through these links, we may earn a commission at no extra cost to you. Thank you for supporting our site.

The Short Answer

GLP-1 cost with and without insurance ranges from $25/month to over $1,300/month—and where you land depends on four things: which medication you need, what kind of insurance you have, whether your plan actually covers it, and if you qualify for savings programs. For real-time pricing across providers, see our GLP-1 pricing index.

Here's the reality most people discover:

- With good commercial insurance + a savings card: $25–$50/month

- With insurance that doesn't cover weight loss: $349–$499/month through manufacturer self-pay programs

- Without any insurance: $149–$499/month depending on whether you choose brand-name or compounded medications

- With Medicare: If your GLP-1 is covered for your diagnosis, out-of-pocket for covered drugs is capped at $2,100 in 2026. The Medicare GLP-1 Bridge launching July 1, 2026 and extended through December 31, 2027 provides eligible Part D beneficiaries access to Wegovy and Zepbound for weight management at $50/month.

The table below shows what real people are paying right now. Below that, we break down every scenario so you know exactly what to expect—and how to get the lowest price for your situation.

Quick Cost Snapshot: What GLP-1s Actually Cost in 2026

This table summarizes (1) current manufacturer list prices, (2) official savings/cash programs, and (3) typical telehealth subscription pricing. Prices can change; we note a "Last verified" date and link to primary sources.

| Medication | List Price | With Insurance + Savings Card | Manufacturer Self-Pay | Telehealth Compounded | Last Verified |

|---|---|---|---|---|---|

| Ozempic (semaglutide) | $1,027/mo | As low as $25 (max savings $100/mo) | $199 intro, then $349/mo; $499 for 2mg (NovoCare) | $119–$249/mo | Apr 2026 |

| Wegovy pen (semaglutide) | $1,349/mo | As low as $25 (max savings $100/mo) | $149/mo (1.5–4mg); $299/mo (9–25mg) (NovoCare) | $119–$249/mo | Apr 2026 |

| Wegovy pill (semaglutide) | $1,349/mo | As low as $25 (max savings $100/mo) | $149/mo (1.5mg, 4mg); $299/mo (higher doses) | N/A | Apr 2026 |

| Mounjaro (tirzepatide) | $1,112/mo | As low as $25 (max savings $150/mo) | Limited* | $249–$349/mo | Apr 2026 |

| Zepbound (tirzepatide) | $1,086/mo | As low as $25 (max savings $100/mo) | $299–$449/mo (LillyDirect vials/KwikPen) | $249–$349/mo | Apr 2026 |

| Foundayo (orforglipron) | TBD (newly launched) | As low as $25/mo (Lilly savings card) | $149/mo (starting dose), up to $349/mo | N/A | Apr 2026 |

| Rybelsus (oral semaglutide) | $998/mo | As low as $25 | Limited programs | N/A | Apr 2026 |

*Mounjaro doesn't have a robust self-pay program like Zepbound does. If you need tirzepatide without insurance, Zepbound vials through LillyDirect are your best brand-name option.

Key insight: Almost nobody pays list price. If your pharmacy is quoting you $900+, you have options—keep reading.

Sources: Manufacturer websites (Novo Nordisk, Eli Lilly), NovoCare Pharmacy, LillyDirect, verified telehealth provider pricing pages. See full source list at bottom.

Why GLP-1 Prices Are So Confusing

Before we dive into specific scenarios, let's clear up why you've probably seen wildly different numbers online.

List Price vs. What You Pay

The "list price" (also called WAC or wholesale acquisition cost) is what manufacturers charge wholesalers. It's the number you see in headlines: "$1,300 a month for Wegovy!"

But here's what actually happens:

- Insurance negotiates lower rates — Your insurer doesn't pay list price. They negotiate discounts and rebates.

- You pay your share — That might be a $25 copay, 20% coinsurance, or 100% until you hit your deductible.

- Savings cards reduce it further — Manufacturer coupons can drop commercial insurance copays to $25.

- Self-pay programs exist — Manufacturers now offer direct pricing at 60–75% below list price.

So when someone says "I pay $25 for Ozempic" and someone else says "My pharmacy quoted $900," they're both telling the truth—their situations are just different.

The 28-Day vs. 30-Day Thing

GLP-1 prescriptions are typically written for 28-day supplies (4 weeks), not calendar months. This means:

- 13 fills per year, not 12

- Annual costs are slightly higher than monthly cost × 12

- Some yearly totals online look weird because of this

We'll use "monthly" throughout this guide, but keep this in mind when budgeting.

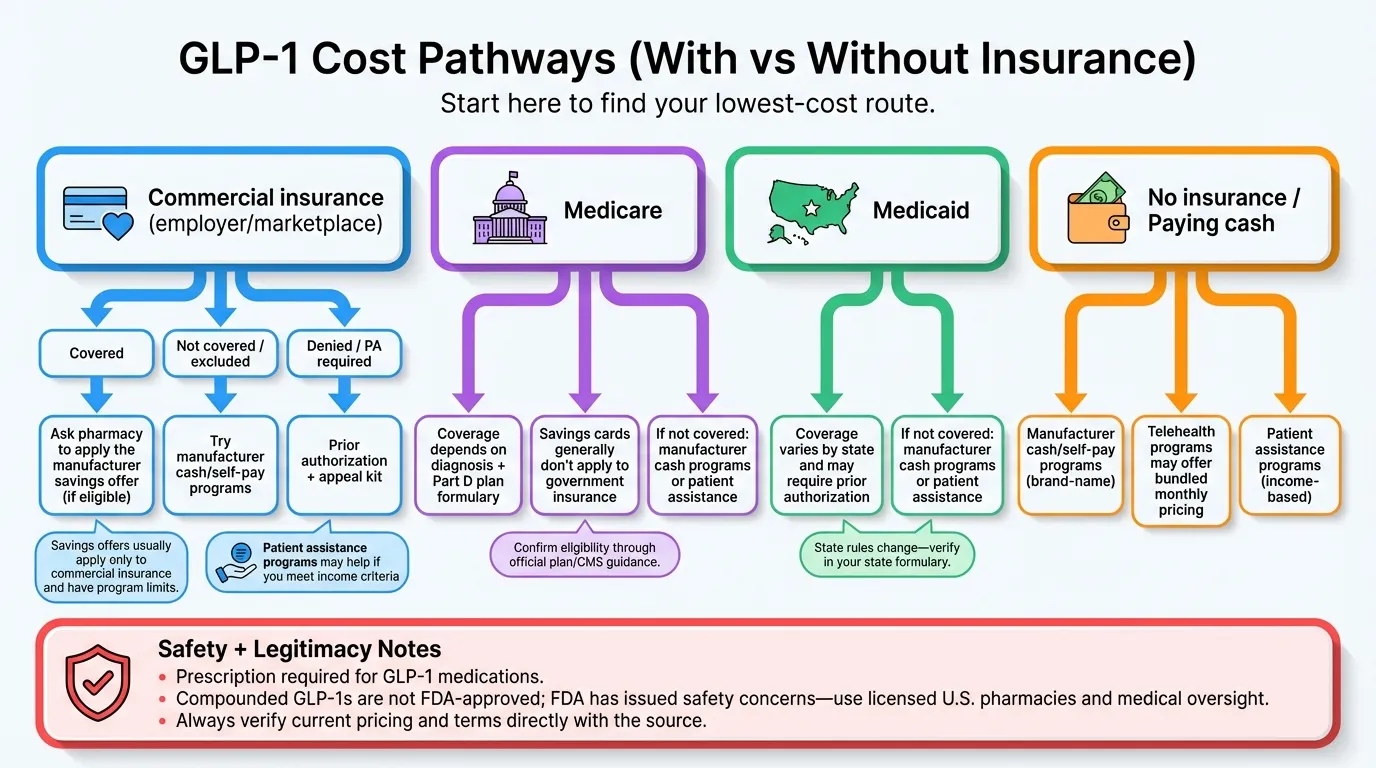

GLP-1 Cost With Commercial Insurance

If you get health insurance through an employer, the ACA marketplace, or buy it privately, this section is for you.

The Coverage Reality Check

Here's something most articles won't tell you directly: most employer health plans don't cover GLP-1s for weight loss.

The numbers from the 2025 KFF Employer Health Benefits Survey:

| Employer Size | Covers GLP-1 for Weight Loss |

|---|---|

| 200-999 workers | 16% |

| 1,000-4,999 workers | 30% |

| 5,000+ workers | 43% |

Coverage is still the exception, not the rule. If you work for a smaller company, the majority of plans exclude weight loss coverage. They'll cover Ozempic or Mounjaro for diabetes, but not Wegovy or Zepbound for weight management.

This is the single biggest factor determining what you'll pay.

To put this in perspective: tens of millions of privately insured adults are clinically eligible for GLP-1 medications based on their BMI. But only a fraction of them have insurance that will actually cover treatment for weight management.

The gap between "medically appropriate" and "covered by insurance" is the source of most of the confusion and frustration around GLP-1 costs.

Why Employers Are Hesitant to Cover GLP-1s

Understanding why helps you navigate the system:

- Cost concerns — GLP-1 drug costs now represent 10.5% of total employer health claims, up from 6.9% just two years ago. Employers are watching these numbers nervously.

- Unknown duration — GLP-1s typically need to be taken long-term. Employers worry about open-ended commitment.

- High demand — Once coverage is added, utilization tends to be higher than expected. Several employers in focus groups reported scaling back coverage after costs exceeded projections.

- Budget pressure — 36% of large employers said prescription drug prices contributed "a great deal" to premium increases in 2025.

The trend is slowly improving—more large employers added coverage this year than dropped it—but don't assume you're covered without checking.

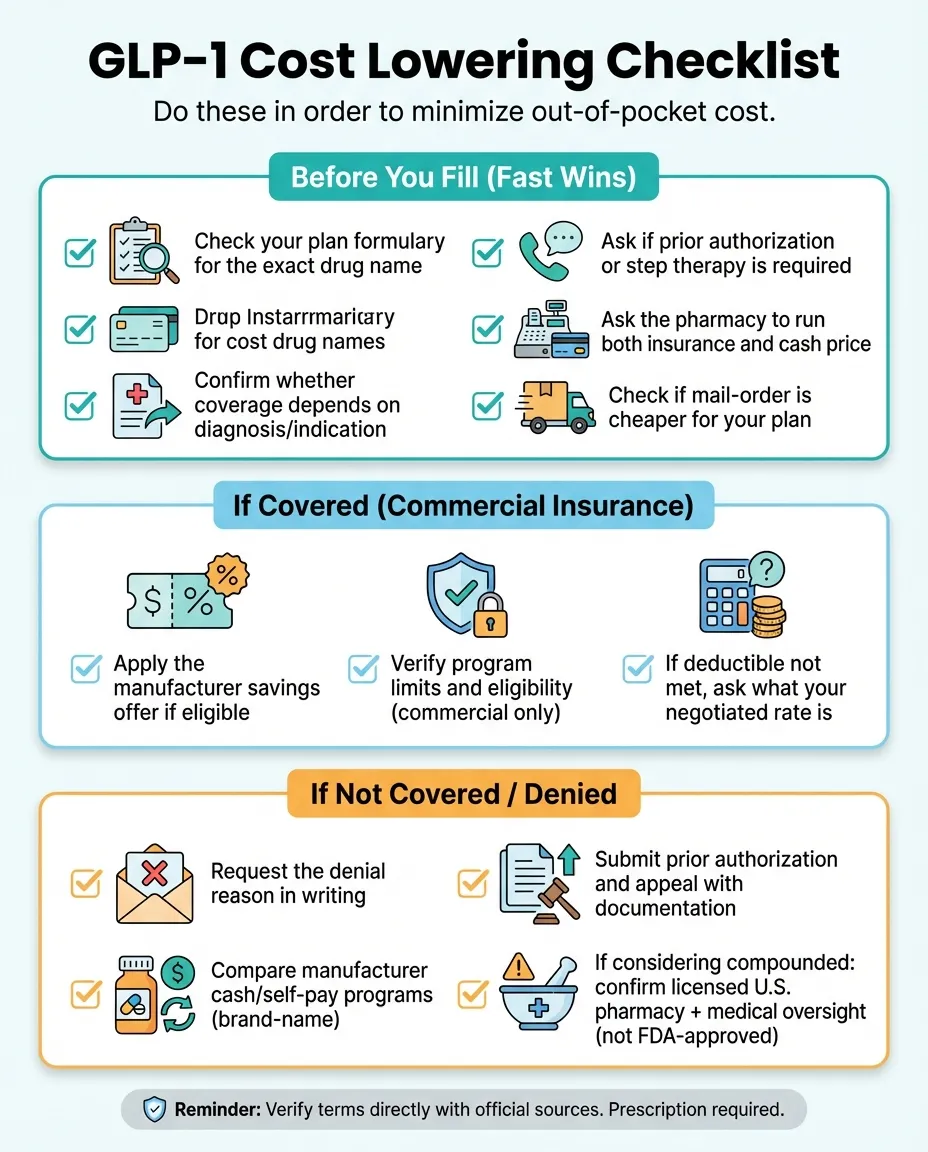

How to Check Your Coverage (5-Minute Process)

Before assuming you're covered or not covered, check:

- Log into your insurance portal and search the formulary (drug list) for: semaglutide, tirzepatide, Wegovy, Zepbound, Ozempic, Mounjaro

- Look for "prior authorization required" — This means your doctor needs to submit paperwork before the pharmacy will fill it

- Check the indication — "Covered for Type 2 diabetes" is different from "covered for weight management"

- Note your tier — Specialty tier drugs (where GLP-1s usually sit) have higher cost-sharing

If you can't find clear answers, call the member services number on your card and ask:

- "Do you cover [medication name] for weight loss/obesity?"

- "What's my cost-sharing for specialty tier drugs?"

- "Is prior authorization required?"

- "Are there step therapy requirements?" (meaning you have to try cheaper drugs first)

Scenario 1: Your Insurance Covers It + You Qualify for a Savings Card

This is the best-case scenario. Here's how the savings programs work:

"Pay as little as $25" only if your copay is already low enough; the offer has a maximum savings limit of $100/month. Government beneficiaries (Medicare, Medicaid, Tricare, VA) are excluded.

- Zepbound with coverage: As low as $25 (max savings $100/month, $1,300/year cap)

- Mounjaro with coverage: As low as $25 (max savings $150/month)

- Government beneficiaries are excluded.

How to get the savings card:

- Mounjaro: mounjaro.com/savings

- Zepbound: zepbound.lilly.com/savings

- Ozempic: ozempic.com/savings

- Wegovy: wegovy.com/coverage-and-savings

Important: Savings cards don't work with Medicare, Medicaid, or other government insurance. If you have commercial insurance through an employer or the marketplace, you're likely eligible.

Scenario 2: Your Insurance Covers It, But You Have a High Deductible

If you have an HDHP (high-deductible health plan), the first few months can be expensive.

How it typically works:

- Before deductible is met: You pay the negotiated rate (not list price, but still $300–$600+)

- After deductible: You pay copay or coinsurance (often 20–25% for specialty drugs)

- After out-of-pocket max: $0

The average deductible for covered workers in 2025 was $1,886. If you're starting GLP-1 treatment in January, expect to pay more until you hit that number.

Money-saving tip: Some manufacturer savings cards can be applied even before you meet your deductible. The Mounjaro and Zepbound cards, for example, cap your cost at $25 regardless of deductible status (for eligible patients with commercial coverage).

Scenario 3: Your Insurance Doesn't Cover Weight Loss

This is the most common situation. Your plan covers GLP-1s for diabetes but specifically excludes them for weight management.

Your options:

- Ask about a diabetes indication — If you have prediabetes or Type 2 diabetes, your doctor may prescribe Ozempic or Mounjaro (both approved for diabetes). Many people have undiagnosed prediabetes.

- Appeal the denial — If you have obesity with comorbidities (high blood pressure, sleep apnea, etc.), an appeal with documentation sometimes works. We cover this in detail below.

- Use manufacturer self-pay programs — More on this in the "without insurance" section, but you can bypass insurance entirely for $349–$499/month.

- Use telehealth with compounded medications — The most affordable option at $149–$299/month, though compounded drugs aren't FDA-approved. See our compounded vs name-brand comparison for details.

What Prior Authorization Means (and How to Handle It)

Prior authorization (PA) is your insurer requiring your doctor to justify why you need a specific medication before they'll cover it.

What insurers typically require for GLP-1 PA:

- BMI of 30+ (obesity), or BMI 27+ with a weight-related condition

- Documentation that you've tried diet and exercise

- Sometimes: proof you've tried older, cheaper medications first ("step therapy")

- Lab work showing relevant health markers

The PA process:

- Your doctor submits the PA request with supporting documentation

- The insurer reviews (usually 24–72 hours, sometimes longer)

- You get approved, denied, or they request more information

- If denied, you can appeal

Most denials can be overturned with proper documentation. The appeals section below has specific strategies. For a step-by-step walkthrough specific to Wegovy, see our Wegovy prior authorization guide.

GLP-1 Cost With Medicare

Medicare coverage for GLP-1s is complicated—and changing. Here's the current state and what's coming.

The Backstory: Why Medicare Doesn't Cover Weight Loss Drugs

This isn't just a policy choice—it's the law. The Social Security Act specifically excludes "agents when used for anorexia, weight loss, or weight gain" from Medicare Part D coverage. This dates back decades, when weight loss drugs were generally ineffective and sometimes dangerous.

The problem is that GLP-1s have fundamentally changed the equation. These aren't the diet pills of the 1990s. They're medications that produce 15-20%+ sustained weight loss while also reducing cardiovascular events, improving kidney function, and treating sleep apnea. But the law hasn't caught up.

The Biden administration proposed reinterpreting the statute in 2024 to allow coverage for obesity treatment. The Trump administration didn't finalize that proposal—but they found another path forward.

What Medicare Part D Covers Right Now (January 2026)

- GLP-1s for Type 2 diabetes (Ozempic, Mounjaro, Trulicity, etc.)

- Wegovy for cardiovascular risk reduction in people with established heart disease

- Zepbound for obstructive sleep apnea

- Any GLP-1 prescribed solely for weight loss/obesity

- This is a statutory exclusion—Medicare is literally prohibited by law from covering "weight loss drugs"

What this means practically: If you have diabetes, your Part D plan probably covers Ozempic or Mounjaro. If you're using a GLP-1 purely for weight management without diabetes or heart disease, Medicare won't help right now.

The cardiovascular indication for Wegovy (approved 2024) opened a door for some Medicare beneficiaries. If you have established cardiovascular disease and obesity, your doctor may be able to prescribe Wegovy and get it covered—not "for weight loss" but "for cardiovascular risk reduction." Same drug, same outcome, different justification.

The 2026 Medicare Part D Out-of-Pocket Cap

In 2026, Medicare's prescription drug law caps out-of-pocket drug costs for covered Part D drugs at $2,100. This cap applies to covered drugs only. Once you reach this threshold, you enter the catastrophic coverage phase and pay $0 for covered medications for the rest of the year.

The Game-Changer: BALANCE Model (Starting Mid-2026)

In December 2025, CMS announced the BALANCE (Better Approaches to Lifestyle and Nutrition for Comprehensive hEalth) Model—a voluntary test that will enable Medicare Part D plans and state Medicaid agencies to cover GLP-1 medications for weight management.

- This is a bridge program before the full model launches

- Medicare pays $245/month (negotiated price)

- Your copay: about $50/month (expected)

- Operates outside normal Part D, so your plan doesn't carry the risk

- Part D plans can choose to participate

- Same pricing structure

- Includes lifestyle support components (nutrition counseling, etc.)

- Model testing runs through December 2031

Eligibility will be defined by CMS + the participating plan/manufacturer requirements, and may vary as the model rolls out. CMS has announced the BALANCE Model and a July 1, 2026 demonstration pathway, but specific patient-level eligibility criteria should be confirmed through official CMS guidance and your plan/provider once enrollment opens.

The Money Behind the Deal

Here's what makes the BALANCE Model financially viable:

- Pre-deal: GLP-1s cost Medicare $5.7 billion annually (and growing), mostly for diabetes treatment

- Negotiated price: $245/month (down from $936-$1,349 list price)

- Patient responsibility: $50/month copay (expected)

- Manufacturer contribution: Significant discounts below even current market rates

The Trump administration's position was essentially: "We'll expand access, but only if it's cost-neutral." By negotiating prices down dramatically, they created room for expanded coverage without blowing up the Medicare budget.

What Medicare Beneficiaries Should Do Now

If you qualify under current rules (diabetes, heart disease, sleep apnea):

- Check your Part D formulary for Ozempic, Mounjaro, or Wegovy

- Ask your doctor which indication makes sense for your situation

- Remember the 2026 Part D out-of-pocket cap is $2,100/year—once you hit that, covered drugs cost $0

If you want GLP-1 for weight loss only:

You have three options:

- Wait until July 2026 — If you meet the eligibility criteria (to be confirmed by CMS), you'll have access to approximately $50/month pricing

- Use manufacturer self-pay now — NovoCare offers Wegovy starting at $199 intro, then $349/month; LillyDirect offers Zepbound at $299-$449/month

- Use cash-pay telehealth compounded — Cash-pay providers like Embody offer compounded GLP-1s (not FDA-approved) from $99 for the first month, then $299/month ongoing, if a provider approves. This is paid out of pocket and doesn't run through Medicare (HSA/FSA may be accepted).

The decision depends on urgency and budget. Waiting 6 months saves significant money if you qualify for the new program. But if weight-related health issues are urgent, starting treatment now may be worth the cost.

Why Medicare Savings Cards Don't Work

Manufacturer savings cards (the ones that drop costs to $25) are prohibited for Medicare beneficiaries. This is an anti-kickback law thing—manufacturers can't provide financial incentives to people in government programs.

Your alternatives:

- Use manufacturer self-pay programs (these bypass Medicare entirely)

- Check if you qualify for Extra Help (low-income subsidy)

- Wait for the July 2026 demonstration

GLP-1 Cost With Medicaid

Medicaid coverage varies dramatically by state—and it's been getting worse in some places, not better.

Current State Coverage (January 2026)

Only 13 state Medicaid programs cover GLP-1s for obesity/weight loss as of January 2026. Several states recently dropped coverage due to budget pressures.

| Coverage Status | States |

|---|---|

| Covers for obesity | DE, KS, MA, MD, MI, MN, MO, MS, NC, TN, UT, VA, WI |

| Dropped coverage (2025-2026) | CA, NH, PA, SC |

Coverage changes frequently. Several states (MI, RI, WI) have announced new restrictions for 2026. This list reflects data as of early January 2026. Always verify current coverage in your state's formulary before assuming you're covered.

If your state covers it: Prior authorization is typically required. Contact your state Medicaid office or managed care plan for formulary details.

If your state doesn't cover it: Your options are the same as being uninsured—manufacturer self-pay programs or telehealth compounded medications. See our guide on how to get GLP-1 without insurance.

Why States Are Pulling Back

The math is simple: GLP-1s cost $600–$800/month net (after rebates), and a lot of people want them. States facing budget pressures are cutting coverage rather than adding it.

The BALANCE Model announced in December 2025 may change this—states can opt into negotiated pricing that could make coverage more sustainable. But that's still months away from implementation.

GLP-1 Cost Without Insurance: Your Real Options

If you don't have insurance, or your insurance won't cover GLP-1s, you have more options than you might think. The days of "pay $1,300 or go without" are over.

Option 1: Manufacturer Self-Pay Programs (Brand-Name)

Both major GLP-1 manufacturers now offer direct-to-consumer pricing that's dramatically lower than list price.

Eli Lilly (Zepbound) via LillyDirect:

| Dose | Monthly Cost | Notes |

|---|---|---|

| 2.5mg vial | $299 | Starting dose |

| 5mg vial | $399 | — |

| 7.5mg–15mg vial | $449 | Requires refill within 45 days; otherwise $599-$1,049 |

Pro tip: If you want tirzepatide without insurance, get Zepbound, not Mounjaro. Same drug, but Zepbound has the self-pay vial option through LillyDirect.

Novo Nordisk (Ozempic, Wegovy) via NovoCare Pharmacy:

| Medication | Intro Price | Ongoing Price | Notes |

|---|---|---|---|

| Ozempic (0.25–1mg) | $199/mo (first 2 fills) | $349/mo | Intro offer through 3/31/26 |

| Ozempic (2mg) | — | $499/mo | No intro pricing |

| Wegovy pen (all doses) | $199/mo (first 2 fills) | $349/mo | Intro offer through 3/31/26 |

| Wegovy pill (1.5mg, 4mg) | $149/mo | $149-$199/mo | 4mg price increases after 4/15/26 |

| Wegovy pill (higher doses) | — | $299/mo | — |

How NovoCare works:

- Your doctor sends a prescription to NovoCare Pharmacy

- They text you to set up your account

- Free home delivery

These prices are available to:

- People without insurance

- People whose insurance doesn't cover GLP-1s

- People who choose not to use their insurance

Important: Cash/self-pay programs generally don't apply to your insurance deductible/OOP max, and NovoCare Pharmacy doesn't accept copay cards.

Option 2: Telehealth Compounded GLP-1s (Most Affordable)

If $299–$349/month is still too much, compounded GLP-1 medications through telehealth providers offer the lowest prices—starting around $119–$149/month for the first month.

What are compounded GLP-1s?

Compounding pharmacies create pharmacy-prepared formulations based on your prescription. These are not FDA-approved and have not been reviewed by the FDA for safety, effectiveness, or quality. They are not the same product as brand-name medications.

This practice isn't new or sketchy—compounding has been around for decades. Hospitals compound medications constantly. The difference is that compounded drugs aren't manufactured at scale with FDA oversight of the finished product.

Critical disclaimer: Compounded medications are not FDA-approved. The FDA has issued warnings about potential risks including dosing errors, contamination, and variability between batches. Only use compounded medications from reputable telehealth providers that work with licensed U.S. pharmacies.

Telehealth GLP-1 Pricing Comparison:

| Provider | Compounded Semaglutide | Compounded Tirzepatide | What's Included |

|---|---|---|---|

| Embody | From $99 first mo, then $299/mo ongoing | $149 first, then $399/mo ongoing | Online intake, provider review, injections or needle-free GLP-1 gum, shipping, 24/7 support |

| Hims | $199/mo (6-mo plan) | Limited | Provider access, medication, app support |

| Hers | $199/mo (6-mo plan) | Limited | Provider access, medication, app support |

| Ro | $349–$399/mo | N/A | Provider, medication, coaching |

| Henry Meds | $179–$297/mo | Available | Provider, medication |

*Prices depend on plan + what is prescribed. Verify current pricing on provider websites.

What to look for in a telehealth provider:

When choosing a telehealth provider for compounded GLP-1s, look for:

- Transparent, predictable pricing — Know what you'll pay at each dose level. Some providers increase prices as your dose goes up during titration.

- Complete program — Your monthly cost should include the physician review, medication, and shipping. Watch for hidden fees.

- Legitimate medical oversight — The provider should work with licensed physicians in your state and licensed U.S. compounding pharmacies.

- Flexibility — Month-to-month billing without long-term contracts is ideal.

Embody is a solid cash-pay option in this space, with a low entry price — from $99 for the first month of a compounded semaglutide injection, then $299/month ongoing — plus a needle-free GLP-1 gum for patients who'd rather avoid injections. They work with licensed providers and compounding pharmacies; medications are compounded and not FDA-approved. State eligibility is confirmed during intake.

Both manufacturer self-pay and telehealth compounded options have their place—the right choice depends on your budget and comfort level with FDA-approved vs. compounded medications.

How telehealth GLP-1 programs work:

- Complete an online health questionnaire (5–10 minutes) — They ask about your medical history, current medications, weight loss goals, and any contraindications

- A licensed provider reviews your information — This isn't instant. An actual healthcare provider in your state looks at your case.

- If appropriate, they prescribe medication — Not everyone is approved. If GLP-1s aren't right for you, they'll tell you.

- Medication ships to your door — Usually within a week, in temperature-controlled packaging

- Ongoing check-ins and dose adjustments — As you progress through the titration schedule, providers monitor your response and adjust as needed

The whole process typically takes 5-7 days from questionnaire to medication delivery. Some providers are faster, some slower.

Option 3: Discount Programs (GoodRx, RxSaver, etc.)

Discount programs like GoodRx can sometimes reduce the pharmacy cash price, but for GLP-1s they often don't beat official manufacturer cash programs (NovoCare Pharmacy, LillyDirect) or reputable telehealth subscription pricing. Use discount cards as a fallback if you prefer a local pharmacy or you can't use the manufacturer channel.

Option 4: Patient Assistance Programs (If You Qualify)

If your income is low enough, you may qualify for free medication:

Typical income requirements (based on Federal Poverty Level):

- Single person: Under approximately $47,000–$63,000/year (300–400% FPL)

- Family of four: Under approximately $97,000–$129,000/year (300–400% FPL)

Income limits vary by manufacturer and program. These are approximate reference ranges based on 2025 Federal Poverty Guidelines—always check the specific program's eligibility rules.

Programs to check:

- Lilly Cares (lilly.com/patient-assistance)

- NovoCare PAP (novocare.com/patient-assistance)

- NeedyMeds (needymeds.org)

- RxAssist (rxassist.org)

How to Appeal an Insurance Denial (Step by Step)

Got denied? Don't give up. Many denials can be overturned with proper documentation and persistence.

Step 1: Understand Why You Were Denied

Call your insurance company and request the specific reason for denial in writing. Common reasons include:

- "Not medically necessary"

- "Prior authorization not on file"

- "Weight loss is an excluded benefit"

- "Step therapy required" (try cheaper drugs first)

- "BMI requirements not met"

Step 2: Gather Your Documentation

Get these from your doctor:

- Complete medical history related to weight

- BMI and weight measurements over time

- List of obesity-related conditions (diabetes, hypertension, sleep apnea, etc.)

- Previous weight loss attempts (diets, exercise programs, medications)

- Lab results showing health impact

Step 3: Write a Strong Appeal

What to include in an appeal:

- Letter of medical necessity from your doctor explaining why this medication is appropriate for you specifically. This should be more detailed than the original PA—think 1-2 pages explaining your case.

- Clinical evidence showing the medication's effectiveness for your condition. Include citations to clinical trials (STEP trials for semaglutide, SURMOUNT trials for tirzepatide).

- Your personal statement describing how obesity/overweight affects your health and quality of life. Be specific: "I have difficulty walking up stairs," "My sleep apnea requires CPAP but I can't tolerate it," "My back pain limits my ability to exercise."

- Documentation of failed alternatives if you've tried other treatments. This could include diet programs (Weight Watchers, Noom, etc.), gym memberships, previous medications (phentermine, Contrave, etc.), or bariatric surgery consultation if not a candidate.

- Cost-effectiveness argument if relevant. GLP-1s may prevent expensive complications down the road (bariatric surgery, cardiovascular events, diabetes management).

Step 4: Know Your Rights

- Insurance companies must respond to appeals within specific timeframes (usually 30–60 days for standard appeals, 72 hours for urgent appeals)

- You have the right to an external review by an independent organization if internal appeals are exhausted

- Many states have additional consumer protections for prescription drug denials

- The appeals process is free—you can't be charged for exercising your rights

Step 5: Consider Alternative Paths

If appeals fail, you still have options:

- Ask about step therapy requirements — Some insurers require you to try metformin or older weight loss drugs first. Completing this step may unlock coverage.

- Explore different diagnoses — If you have prediabetes or Type 2 diabetes, Ozempic and Mounjaro may be covered when Wegovy and Zepbound aren't.

- Check for formulary alternatives — Your insurer may prefer a different GLP-1 (like Saxenda) over the one you requested.

- Use self-pay options — At some point, the time and energy spent on appeals may not be worth it compared to $299-$349/month self-pay. Use our GLP-1 cost finder to compare current prices across providers.

Compounded GLP-1: What You Need to Know

Compounded GLP-1s are a significant part of the market right now, so let's address them directly and honestly.

What Compounding Is

Compounding pharmacies create customized medications by mixing ingredients according to a doctor's prescription. It's a legitimate practice that's been around for decades—think custom hormone treatments, medications for people with allergies to certain fillers, or pediatric doses that don't exist commercially.

For GLP-1s, compounding pharmacies source the active ingredient (semaglutide base or tirzepatide) and formulate it into injectable or oral forms. This became widespread during the GLP-1 shortage of 2023-2024, when brand-name medications were nearly impossible to get.

Why compounded GLP-1s cost less:

- No brand-name markup

- No direct-to-consumer advertising costs

- Simpler supply chain

- Competition among compounding pharmacies

FDA Concerns (Read This Carefully)

The FDA has issued warnings about compounded GLP-1 products:

- Dosing errors — Some compounded products have had incorrect concentrations. The FDA tested samples and found variability.

- Salt form confusion — "Semaglutide sodium" or "semaglutide acetate" are different from the semaglutide base used in Ozempic/Wegovy. The molecular weight differs, so doses aren't directly equivalent. A provider using salt forms should adjust dosing accordingly—if they don't mention this, it's a red flag.

- Quality variability — Without FDA oversight of the finished product, quality can vary between batches and between pharmacies.

- Sterility concerns — Injectable medications require strict sterile manufacturing. Not all compounding facilities meet the same standards.

What this means for you: This doesn't mean all compounded GLP-1s are dangerous—millions of people have used them successfully. But it does mean you need to be careful about where you get them. The difference between a reputable telehealth provider and a sketchy one isn't just customer service—it's whether you're getting what you paid for at the dose you expect.

How to Vet a Compounded GLP-1 Provider

- Works with licensed U.S. compounding pharmacies (look for 503A or 503B designation)

- Uses semaglutide base (not sodium or acetate salts) or clearly explains dosing adjustments

- Has licensed healthcare providers reviewing every prescription

- Includes proper medical oversight and follow-up

- Transparent about what compounding means and its limitations

- Will tell you exactly which pharmacy fills their prescriptions

- Has clear refund/cancellation policies

- Won't tell you which pharmacy compounds their medications

- Uses vague terminology like "pharmaceutical grade" without specifics

- No medical provider involved in the prescribing process

- Prices dramatically lower than established competitors

- Ships from overseas or unclear locations

- Requires large upfront payments with no refund option

- No follow-up or dose adjustment process

When Compounded Makes Sense (and When It Doesn't)

- Brand-name medications are unaffordable ($349-$499/month is still too much)

- You understand and accept that they're not FDA-approved

- You're using a reputable provider with proper medical oversight

- You're comfortable with the monitoring process to catch any issues early

- You have specific health conditions that make dosing precision critical

- You prefer the assurance of FDA oversight

- The cost difference isn't significant for your situation

- You're risk-averse about medical decisions

There's no universally "right" answer here. Some people happily use compounded GLP-1s for years. Others prefer paying more for the peace of mind of FDA-approved products. Both are valid choices. Read our full guide on compounded vs name-brand GLP-1s for more details.

The GLP-1 Cost Decision Tree

Still not sure which path is right for you? Walk through this:

→ YES: Go to Question 2

→ NO: Skip to "Without Insurance Path" below

→ YES: Go to Question 3

→ NO / NOT SURE: Check your formulary or call member services. If not covered, go to "Without Insurance Path"

→ YES (commercial insurance, not Medicare/Medicaid): Enroll in savings card. Your cost: as low as $25/month (subject to savings caps)

→ NO (Medicare, Medicaid, or other government insurance): Your cost depends on your plan's copay/coinsurance structure. If too expensive, consider "Without Insurance Path"

Question A: What's your monthly budget for GLP-1 treatment?

→ $300–$450/month: Use manufacturer self-pay programs

- Zepbound: LillyDirect at $299–$449

- Wegovy/Ozempic: NovoCare at $199 intro, then $349

→ $120–$250/month: Use telehealth compounded options

- Embody: from $99 first month intro, then $299/month ongoing (cash-pay, compounded)

- Similar providers in the $150–$250 range (see our telehealth provider comparison for detailed reviews)

→ Under $120/month: Check patient assistance programs or consider waiting for Medicare/Medicaid expansion if applicable

Question M1: Do you have a qualifying condition (diabetes, heart disease, sleep apnea)?

→ YES: Check if your Part D plan covers the relevant GLP-1. You may have coverage now.

→ NO (obesity/weight loss only):

- Can you wait until July 2026? Your cost may be around $50/month under the new demonstration (eligibility criteria to be confirmed by CMS).

- Can't wait? Use manufacturer self-pay ($299–$449) or telehealth compounded ($119–$249).

How to Lower Your GLP-1 Cost: 12 Real Strategies

These actually work. We've seen real people use each one.

If You Have Insurance

- Always run the savings card — Even if you have good coverage, manufacturer cards often make it cheaper

- Check preferred pharmacies — Your PBM may have specific pharmacies with lower copays

- Try mail-order — 90-day supplies are often cheaper per dose than 30-day fills

- Appeal denials — Use the toolkit above. Many initial denials are reversed.

- Ask about step therapy alternatives — If they require you to try metformin first, doing so may unlock coverage

- Document everything — The stronger your medical record, the better your PA approval odds

If You're Paying Cash

- Compare all manufacturer programs — NovoCare vs. LillyDirect vs. Costco partnerships

- Ask the pharmacy to run cash price — Sometimes it's cheaper than running through insurance

- Consider compounded options — If cost is the primary barrier and you understand the tradeoffs

- Check patient assistance programs — You may qualify even with moderate income

- Use HSA/FSA funds — GLP-1s are eligible expenses. This effectively gives you a ~30% discount by using pre-tax dollars.

- Ask about dose optimization — Some people maintain results on lower maintenance doses, reducing cost

What to Expect: GLP-1 Cost Over Time

GLP-1 treatment isn't a one-time thing. Here's what a full year typically looks like—and why long-term cost planning matters.

First Year Cost Breakdown

Months 1–12: approximately $25/month (subject to caps) = ~$300–$400/year

This assumes your insurance covers the medication and you remain eligible for the savings card.

- Month 1: from $99 (intro)

- Months 2–12: $299 × 11 = $3,289

- Total Year 1: ~$3,388

That's about $282/month averaged over the year. The first month is discounted intro pricing; ongoing months are $299. Multi-month bundles from $199/month can lower the per-month cost if you commit upfront. Compounded, not FDA-approved; cash-pay (HSA/FSA may be accepted).

- Months 1–2: $199 × 2 = $398 (intro price)

- Months 3–12: $349 × 10 = $3,490

- Total Year 1: ~$3,900

The Dose Escalation Reality

Here's something that catches people off guard: GLP-1s use a titration schedule. You start at a low dose and increase every 4 weeks until you reach the target dose.

Typical semaglutide schedule (Wegovy):

- Weeks 1-4: 0.25mg

- Weeks 5-8: 0.5mg

- Weeks 9-12: 1mg

- Weeks 13-16: 1.7mg

- Week 17+: 2.4mg (maintenance)

Why this matters for cost: Some telehealth providers charge more as your dose increases. A program that's $149/month at the starting dose might be $399/month at the maintenance dose, so always ask a provider how pricing changes during titration before you commit. Embody is a cash-pay compounded option that starts from $99 for the first month, then $299/month ongoing for a semaglutide injection (tirzepatide and a needle-free GLP-1 gum are also offered).

Long-Term Considerations

Key facts about GLP-1 duration:

- GLP-1s typically need to be continued to maintain weight loss

- Clinical studies show most people regain significant weight within a year of stopping

- WHO guidelines (December 2025) define long-term use as 6+ months, often years

- This is similar to blood pressure or cholesterol medication—it manages a condition rather than curing it

The good news about maintenance:

Many people don't stay at the maximum dose forever. Once you reach your goal weight and stabilize, your provider may try reducing to a lower maintenance dose (which can lower cost), spacing injections further apart, or transitioning to lifestyle maintenance with medication as backup. Learn more about what happens when you stop taking GLP-1.

Are Prices Going Down?

Yes, and here's why:

Already happened:

- March 2025: Eli Lilly cut Zepbound vial prices to $349-$499 for self-pay

- November 2025: Novo Nordisk cut Wegovy/Ozempic self-pay to $349

- November 2025: Trump administration negotiated $245 Medicare pricing

Coming soon:

- July 1, 2026: Medicare GLP-1 Bridge launches at $50/month copay, extended through December 31, 2027 (BALANCE Part D delayed)

- 2027: More oral GLP-1 options expected, which typically come in cheaper

On the horizon:

- Semaglutide patents begin expiring around 2031-2032

- Once patents expire, lower-cost versions could eventually bring prices down

- Competition from new entrants (retatrutide, orforglipron) should pressure pricing

If you can wait, prices are trending downward. If you need to start now, the options above make treatment accessible—and you can always switch to cheaper options as they become available.

GLP-1 Cost FAQs

How much does GLP-1 cost per month?

GLP-1 cost ranges from as low as $25/month (with insurance + savings card, subject to caps) to $1,349/month (list price). Most people pay between $119–$449/month depending on insurance status and which program they use.

Why do some people pay $25 and others pay $1,000?

Insurance coverage and savings card eligibility. Someone with commercial insurance that covers the medication and a manufacturer savings card may pay as low as $25 (subject to savings caps). Someone paying list price at a pharmacy without any programs pays $1,000+.

Does Medicare cover GLP-1s for weight loss?

Yes, starting July 1, 2026. The Medicare GLP-1 Bridge provides eligible Medicare Part D beneficiaries access at $50/month copay. CMS extended the Bridge through December 31, 2027 after delaying BALANCE Part D implementation. Check cms.gov for the current BALANCE Model launch date.

What if my insurance covers Ozempic but not Wegovy?

This is common—they're both semaglutide, but Ozempic is approved for diabetes and Wegovy for weight management. If you have prediabetes or Type 2 diabetes, your doctor may be able to prescribe Ozempic instead.

Is compounded semaglutide safe?

Compounded medications are prepared by licensed pharmacies but are not FDA-approved. The FDA has raised concerns about dosing accuracy and quality variability. Use established telehealth providers that work with licensed U.S. pharmacies and include proper medical oversight.

Can I use a savings card if I have Medicare?

No. Federal anti-kickback laws prohibit manufacturer savings cards for people in government insurance programs (Medicare, Medicaid, Tricare, VA). Your options are using Part D coverage (if you have a qualifying condition) or paying through manufacturer self-pay programs.

What is the cheapest GLP-1 without insurance?

Compounded semaglutide through cash-pay telehealth providers like Embody (from $99 first month, then $299/month ongoing). For brand-name FDA-approved medications, NovoCare (Wegovy/Ozempic starting at $199 intro, then $349) and LillyDirect (Zepbound starting at $299) offer the best prices.

Why is my pharmacy quoting me $900+ when I see prices of $299 online?

Your pharmacy is quoting list price or their cash price. Manufacturer self-pay programs (NovoCare, LillyDirect) bypass regular pharmacies with direct pricing. Ask your doctor to send the prescription to the manufacturer's pharmacy instead.

Do I need a prescription for GLP-1 medications?

Yes, always. GLP-1s are prescription medications. Telehealth services include a licensed provider who evaluates you and writes the prescription—you don't need a separate doctor's visit, but you do need medical oversight.

How much does GLP-1 cost per year?

Annual costs range from ~$300–$400 (excellent insurance + savings card) to over $16,000 (list price). Most self-pay patients using telehealth compounded options spend $2,900–$3,500/year. With manufacturer self-pay, expect $3,900–$5,000/year.

Can I use HSA or FSA to pay for GLP-1s?

Yes. GLP-1 medications are eligible HSA/FSA expenses when prescribed by a healthcare provider. Using pre-tax dollars effectively saves you 20–30% depending on your tax bracket.

What is the difference between Ozempic and Wegovy?

Same drug (semaglutide), different dosing and approved uses. Ozempic is approved for Type 2 diabetes at doses up to 2mg. Wegovy is approved for weight management and goes up to 2.4mg. Your insurance may cover one but not the other depending on your diagnosis.

What is the difference between Mounjaro and Zepbound?

Same drug (tirzepatide), different approved uses. Mounjaro is for Type 2 diabetes. Zepbound is for weight management (and obstructive sleep apnea). Zepbound has a self-pay program through LillyDirect ($349-$499/month) while Mounjaro does not.

How long do I need to take GLP-1 medications?

Most people need to take them long-term to maintain results. Clinical studies show that stopping GLP-1s typically leads to weight regain. The WHO's December 2025 guidelines define long-term use as 6+ months, often years.

Do GLP-1s actually work?

Yes. Clinical trials show average weight loss of 15-20% of body weight over 12-18 months for semaglutide (Wegovy), and 20-25% for tirzepatide (Zepbound). Beyond weight loss, studies show cardiovascular benefits, improved blood sugar control, and reduced rates of kidney disease progression.

How We Research GLP-1 Pricing

We take accuracy seriously because wrong information wastes your time and money.

Our Sources (In Order of Priority)

- Official manufacturer websites and press releases — Novo Nordisk (ozempic.com, wegovy.com), Eli Lilly (lillydirect.com, zepbound.lilly.com)

- Government sources — FDA drug information, CMS announcements, Congressional Research Service reports

- Peer-reviewed research and reputable health organizations — KFF, Peterson Center on Healthcare, EBRI

- Direct verification — We check telehealth provider pricing pages and confirm current offers

What "Last Verified" Means

When we say "pricing last verified January 2026," it means we checked the source within that month. GLP-1 pricing changes frequently—manufacturer programs update terms, telehealth providers adjust rates, insurance coverage shifts.

If you see a price that doesn't match what you're being quoted, the discrepancy is usually one of:

- Your specific situation (location, insurance status, dose)

- A very recent change we haven't caught yet

- A misunderstanding about which program applies

When in doubt, check the source directly. We link to everything.

Corrections Policy

If we get something wrong, we fix it and note the correction. Healthcare information is too important to let errors stand.

Sources & Citations

- Wegovy Coverage and Savings — Novo Nordisk

- Zepbound Coverage & Savings — Eli Lilly

- LillyDirect — Eli Lilly

- NovoCare Pharmacy — Novo Nordisk

- 2025 Employer Health Benefits Survey — KFF

- BALANCE Model Announcement — CMS

- FDA Concerns About Unapproved GLP-1 Drugs — FDA

- STEP Clinical Trials — New England Journal of Medicine

Medical Disclaimer: This content is for informational purposes only and does not constitute medical advice. GLP-1 medications require a prescription from a licensed healthcare provider. Always consult with your doctor before starting any new medication. Pricing information is subject to change and should be verified directly with providers before making decisions.

Related Guides

Complete Cost & Insurance Guide

Explore all 8 guides in this topic.

Cheapest GLP-1 Without Insurance Online

Verified cheapest GLP-1 options available online without insurance ranked by real prices.

Cheapest Tirzepatide Online Without Insurance

Real prices for the cheapest tirzepatide available online without insurance coverage.

Cheapest Semaglutide

Where to find the lowest semaglutide prices including compounded and brand-name options.

How to Get GLP-1 Without Insurance

Step-by-step guide to accessing GLP-1 medications affordably without insurance coverage.

Wegovy Pill Cost & Where to Buy

Current Wegovy pill pricing, availability, and the best places to buy it in 2026.

Wegovy Prior Authorization

How to navigate Wegovy prior authorization including timelines, appeals, and approval tips.

GLP-1 Pricing Index

Live pricing data tracking GLP-1 medication costs across major telehealth providers over time.

Zepbound Cost Without Insurance

Verified Zepbound cash prices by dose, device, and buying path — every pricing path from $299 LillyDirect to $1,272 retail.