Best GLP-1 for Self-Employed Workers in 2026: Cash-Pay, HSA, or Insurance?

By the Weight Loss Provider Guide Editorial Team · · · · Affiliate disclosure

Weight Loss Provider Guide is an independent comparison resource for GLP-1 telehealth providers. We may earn a commission when readers sign up through our links. Our rankings are based on verified pricing, route fit, and policy transparency — not commissions.

The 30-second answer

The best GLP-1 for self-employed people in 2026 isn’t one medication — it’s the right access route for your situation. For most freelancers, contractors, and 1099 workers paying cash, Embody is a strong low-cost starting point (from $99 for the first month of compounded semaglutide injection, then $299/month ongoing, with HSA/FSA cards advertised as accepted at checkout, a needle-free GLP-1 gum option, and 24/7 support). If you want FDA-approved Wegovy, Zepbound, or Foundayo — and you have a marketplace plan worth checking first — start with Ro ($39 first month, then as low as $74/month with the annual prepay plan, plus a free insurance coverage checker).

Here’s the part most “best GLP-1” pages skip: per KFF’s June 2024 analysis of 2024 federally facilitated Marketplace formularies, about 1% of those Marketplace prescription drug plans covered Wegovy for weight loss, while 82% covered Ozempic — same molecule (semaglutide), but only when prescribed for type 2 diabetes. Translation: if you’re self-employed on a federally facilitated Marketplace plan and you’re chasing weight-loss-only Wegovy coverage, expect an out-of-pocket path.

We compared eight GLP-1 telehealth providers head-to-head on the things that actually matter for 1099 income: predictable pricing, HSA/FSA acceptance at checkout, cancellation friction, and what they show you before you pay. Here’s the route map.

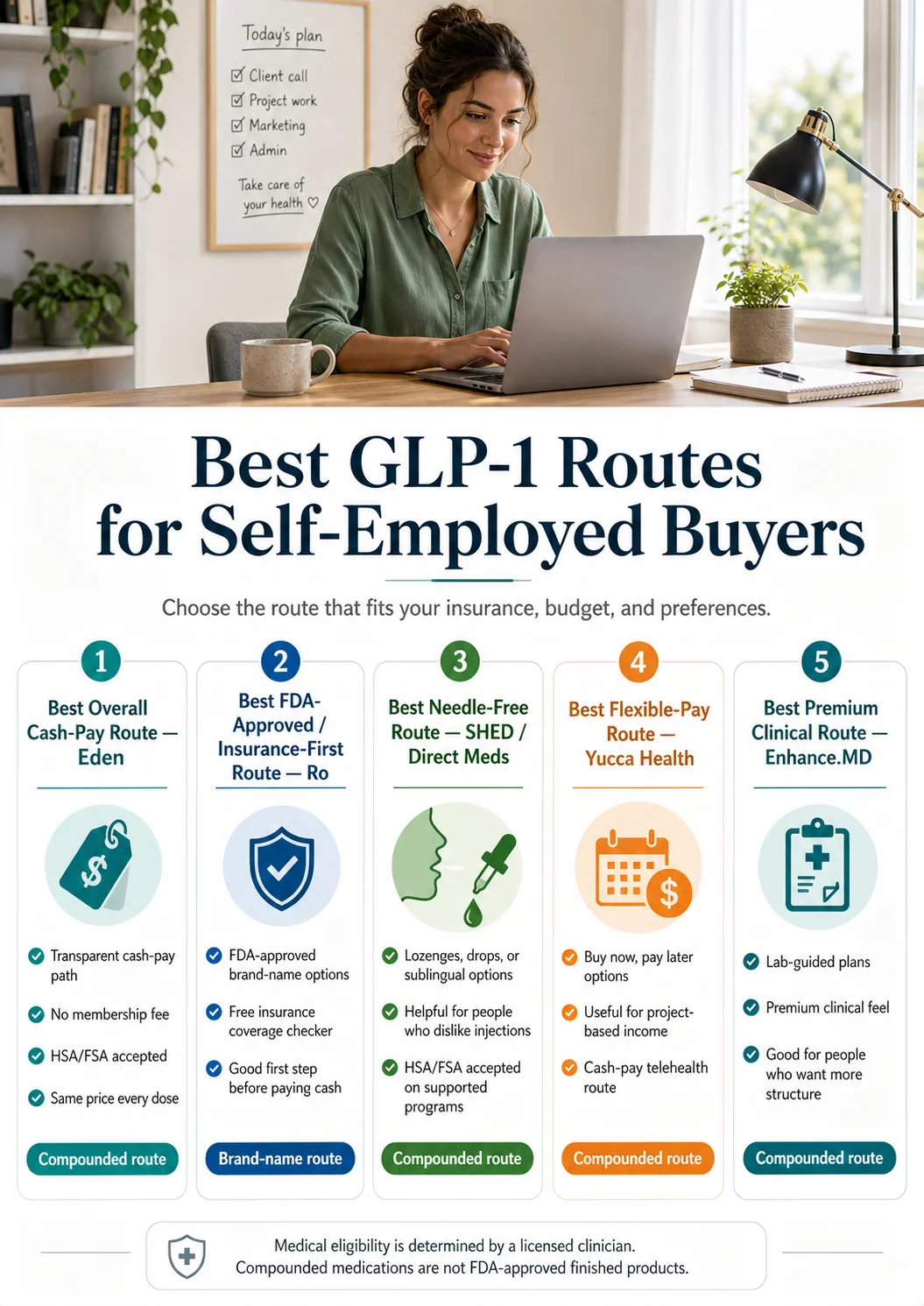

Verified picks at a glance

Quick verdict: Embody is a strong pick for cash-pay self-employed buyers who want the lowest first-month price and a needle-free GLP-1 gum option. Ro wins when insurance is worth checking or you specifically want FDA-approved brand-name medication. The other picks below are for narrower fits.

| If you are… | Best provider | Medication category | Why | Starting cost |

|---|---|---|---|---|

| Cash-pay buyers who want the lowest first-month price | Embody | Compounded | Low $99 first-month entry, HSA/FSA at checkout, needle-free GLP-1 gum option, 24/7 support | $99 first month, then $299/mo ongoing (sema injection) |

| Want FDA-approved Wegovy / Zepbound / Foundayo | Ro | FDA-approved brand-name | Free insurance coverage checker, brand-name medication, prior auth concierge | $39 first month, then as low as $74/mo (annual prepay) |

| Want brand-name with provider choice | Sesame Care | FDA-approved brand-name | Membership as low as $59/mo annually, branded GLP-1 menu | $59/mo membership (med separate) |

| Hate needles, want oral or sublingual | SHED or Direct Meds | Compounded | Lozenges, drops, sublingual options; HSA/FSA accepted | SHED ~$199/mo; Direct Meds from $249/mo |

| Income comes in lumps (project-based) | Yucca Health | Compounded | Klarna, Affirm, Afterpay at checkout | From $146/mo (6-month sema plan) |

| Want labs and a premium clinical feel | Enhance.MD | Compounded | Metabolic labs every 6 months included | Core $49 first / $212 after |

Not for: If you have Medicare or Medicaid, this guide isn’t your starting point — see our Medicare GLP-1 guide instead. If you only want FDA-approved brand-name medication, skip the compounded picks and start with Ro or Sesame Care.

Best low-cost cash-pay starter — Embody

From $99 first month (semaglutide injection), then $299/month ongoing. HSA/FSA at checkout. Needle-free GLP-1 gum option. 24/7 support.

Check Embody EligibilityBest for FDA-approved + insurance check — Ro

$39 first month, then as low as $74/month annual. Free insurance coverage checker for Wegovy / Zepbound / Foundayo.

Check Your Insurance With Ro’s Free Coverage ToolNot sure which route fits you? Take the 60-second matching quiz.

Find My Self-Employed GLP-1 Route →What we actually verified for this page

Here’s what we checked, when, and what still needs your own verification at checkout:

- Provider pricing — pulled directly from each provider’s pricing or checkout page on May 1–2, 2026

- HSA/FSA language — verified on each provider’s payment or FAQ page where disclosed (not all providers accept HSA/FSA cards)

- Insurance support — confirmed Ro’s coverage checker and concierge language on Ro’s official insurance page

- FDA-approved manufacturer pricing — pulled from NovoCare Pharmacy and LillyDirect official pages

- Tax framework — based on IRS Publication 502, IRS Publication 969, IRS guidance on weight-loss-related medical expenses, and IRS Form 7206 instructions

- ACA Marketplace coverage data — sourced from KFF’s June 2024 analysis of 2024 federally facilitated Marketplace formularies (state-run Marketplaces excluded)

- FDA regulatory standing — checked the FDA warning letter database; we disclose any open letters in the provider sections below

We did not purchase from each provider to test fulfillment, and we did not verify HSA/FSA card acceptance at checkout for every provider — Embody, SHED, Direct Meds, NovoCare, and LillyDirect have explicit HSA/FSA language; Enhance.MD’s FAQ states it does not accept HSA/FSA cards; Yucca’s FAQ states it does not provide itemized receipts or letters of medical necessity; Ro, Sesame Care, and MEDVi require checkout-level verification before assuming card acceptance.

We are not a medical authority, a tax authority, or your accountant. Verify with your prescriber, your tax professional, and your HSA administrator before acting on anything you read here.

Why “best GLP-1 for self-employed” is a different question than “best GLP-1”

Answer: Self-employed workers face a different set of rules than W-2 employees: no employer GLP-1 coverage, ACA Marketplace plans that almost never cover weight-loss medication (about 1% Wegovy coverage rate per KFF’s 2024 federally facilitated Marketplace analysis), and unpredictable monthly income that makes a $200–$400 recurring expense feel risky. Self-employed people also have tax-positioning levers — HSA contributions, the self-employed health insurance deduction, and the Schedule A medical-itemizing threshold — that change the effective net cost of a GLP-1.

When a Fortune 500 employee gets Zepbound, they often pay a $25 copay because their employer’s plan covers it. When you’re self-employed on a Bronze marketplace plan, your insurance pays $0 and you pay the full retail of $1,000+/month — unless you go cash-pay through a compounded telehealth provider or buy direct from the manufacturer through programs like NovoCare or LillyDirect.

Three things working against you:

- About 1% of federally facilitated Marketplace prescription drug plans cover Wegovy for weight loss (KFF, 2024 federal data)

- About 82% of those same plans cover Ozempic — same molecule (semaglutide), but only when prescribed for type 2 diabetes

- Most self-employed workers don’t have access to employer HRAs, ICHRAs, or GLP-1 carve-outs

Three things working for you:

- HSA contributions — if you have an HSA-eligible high-deductible health plan (HDHP — for 2026, at least $1,700 self-only or $3,400 family deductible, with out-of-pocket maximums not exceeding $8,500 self-only or $17,000 family), 2026 contribution limits are $4,400 self-only and $8,750 family. HSA contributions are deductible for federal income-tax purposes, grow tax-free, and qualified withdrawals (including for prescribed GLP-1s) are tax-free.

- Self-employed health insurance deduction — an above-the-line deduction reported on Schedule 1, Line 17 (calculated using IRS Form 7206). Lowers your AGI even if you don’t itemize. Covers premiums, not the medication itself.

- Schedule A itemized medical expense deduction — out-of-pocket medical costs above 7.5% of your AGI are deductible if you itemize. Most self-employed people won’t, but if you have a high-medical year, it can stack.

We’ll get into the dollar-for-dollar tax math further down. The headline: pick the access route first, then layer the tax work on top.

The 5 best GLP-1 providers for self-employed buyers, ranked

Answer: After comparing eight GLP-1 telehealth platforms on cash-pay pricing, HSA acceptance, cancellation flexibility, and medication menu, Embody is a strong low-cost route for cash-pay self-employed buyers, Ro is the best route for FDA-approved brand-name medication and insurance help, MEDVi is a strong cash-pay alternative with one important regulatory disclosure, SHED is the best needle-free option, and Yucca Health is best for project-based income that needs payment flexibility.

1. Embody — Best low-cost cash-pay starter for self-employed buyers

Best for: Freelancers, consultants, and 1099 workers who want the lowest first-month price, HSA/FSA at checkout, and a needle-free GLP-1 gum option.

Verified pricing (as of May 2, 2026):

- Compounded semaglutide injection: $99 first month, then $299/month ongoing

- Compounded tirzepatide injection: $149 first month, then $399/month ongoing

- Needle-free GLP-1 gum option for needle-averse patients

- Cash-pay; HSA/FSA cards advertised as accepted at checkout

- 24/7 care team messaging

Insurance: Embody does not take insurance (cash-pay only).

HSA/FSA at checkout: Yes — Embody advertises HSA/FSA cards as accepted at checkout.

Cancellation: Embody is a cash-pay program with no insurance contract — confirm its specific cancellation and refill timing during intake.

Why this fits self-employed people specifically:

For self-employed buyers paying cash, the appeal of Embody is the low barrier to start: $99 for the first month of compounded semaglutide injection lets you begin treatment without a large upfront commitment, and you can pay with an HSA/FSA card at checkout. Budget for the ongoing rate — standard semaglutide-injection refills run $299/month — rather than only the intro price. For needle-averse buyers, Embody also offers a needle-free GLP-1 gum option, and the care team is available 24/7.

The HSA/FSA-at-checkout piece matters more than people realize. With most providers, you pay with a regular card and submit for reimbursement later — meaning your HSA dollars sit unused while your bank account takes the hit. Embody advertises HSA/FSA cards as accepted at checkout, which helps keep your cash flow clean.

Honest tradeoff: Embody is not the right first choice if you want FDA-approved brand-name medication or if your priority is using insurance. Embody’s shipped options are compounded GLP-1 medications, not FDA-approved finished drugs, and refills cost more than the intro first month — readers who specifically searched “Wegovy” or “Zepbound” should check Ro first. Embody’s strength is a low first-month entry price, cash-pay simplicity, and a needle-free GLP-1 gum option for people who don’t want weekly injections.

2. Ro — Best for FDA-approved medication and insurance-first checking

Best for: Self-employed people with commercial or marketplace insurance who want to check coverage before paying cash, OR who specifically want FDA-approved Wegovy, Zepbound, Foundayo, or Ozempic.

Verified pricing (as of May 2, 2026):

- Ro Body membership: $39 for the first month, then $149/month (or as low as $74/month with annual plan paid upfront)

- Get started for $39, then as low as $74/month with annual plan paid upfront

- Medication cost is separate from membership and matches LillyDirect, NovoCare, and TrumpRx pricing

Medications offered: Foundayo (orforglipron), Wegovy pill, Wegovy injection, Zepbound pen, Zepbound KwikPen.

Insurance: Ro offers a free GLP-1 Insurance Coverage Checker. An insurance specialist contacts your insurer and creates a personalized coverage report. Ro states it cannot coordinate GLP-1 coverage for government insurance plans, with an FEHB (Federal Employees Health Benefits) exception.

HSA/FSA: Medication costs may be HSA/FSA-reimbursable when they qualify as a prescription medical expense; Ro membership and card acceptance should be confirmed at checkout.

Why this fits self-employed people:

If you bought a marketplace plan and want to know whether anything will be covered before you commit to cash-pay, Ro is the lowest-friction path. The insurance specialist runs the coverage check for you and handles prior authorization paperwork — which, if you bill clients $75–$300/hour, is real money in time saved.

There’s also a workflow benefit: if your coverage check comes back negative, you’ve already got the brand-name path lined up at Ro at LillyDirect/NovoCare-matched pricing. One provider, two paths.

A real Ro member quote (from Ro’s official member testimonial section, where Ro discloses members were paid in exchange for testimonials): “I was not expecting insurance help.” — Hannah, Ro member.

Honest tradeoff: Ro is not the cheapest cash-pay route if your insurance ends up denying coverage. Membership ($149/month standard) plus medication can run $300–$700/month total depending on the drug and dose. If pure cash-pay is your only path and FDA-approved isn’t critical, Embody or MEDVi will be cheaper.

3. MEDVi — Cash-pay alternative (with one disclosure you need)

Best for: Cost-conscious buyers who want a broad menu of compounded GLP-1 options and have read and considered the regulatory disclosure below.

Verified pricing (as of May 2, 2026):

- Compounded semaglutide: starting $179 first month / $299/month refills

- Plans include physician review, 1:1 guidance, metabolic report, medication shipped

Insurance: Cash-pay model.

HSA/FSA: Verify card acceptance directly at MEDVi checkout before purchase.

The disclosure we have to make plainly:

The FDA issued a warning letter to MEDVi LLC dba MEDVi on February 20, 2026 (FDA warning letter 721455). The letter flagged marketing claims about compounded semaglutide and tirzepatide, including phrasing that the FDA said implied compounded products had been FDA-evaluated when they had not. This is a material regulatory event that any reasonable buyer would want to know about before signing up. We don’t know how MEDVi has remediated since the letter was issued — that’s something to verify directly with MEDVi before deciding.

What this means practically:

- If you want a cash-pay compounded option, Embody is an alternative; if you want FDA-approved medication, Ro is the cleaner regulatory path

- If you’re comfortable evaluating compounded providers individually and MEDVi’s pricing fits your budget, ask them directly about the warning letter status before signing up

- This is not a recommendation to avoid MEDVi — it’s a disclosure that lets you make the call

Honest tradeoff: MEDVi’s pricing is competitive. But a February 2026 FDA warning letter is the kind of fact a self-employed buyer needs to know about before signing up, not after. We’re listing MEDVi because it’s a real option and the price reflects that, but if you want to compare other cash-pay compounded options, Embody is one to look at, and Ro covers the FDA-approved path.

If you want to compare other options: Check Embody for cash-pay compounded or Check Ro for FDA-approved.

4. SHED — Best for needle-free GLP-1 access

Best for: Self-employed buyers who don’t want to inject themselves weekly and specifically want to discuss oral, sublingual, or lozenge-based compounded options.

Verified pricing (as of May 2, 2026):

- GLP-1 lozenges starting around $199/month (verify current checkout pricing — page elements have shown both $149/month and $199/month)

- Multiple formats: lozenges, drops, weekly injections

Insurance: Cash-pay.

HSA/FSA: SHED states HSA/FSA cards are accepted for medical prescription supplies, provider visits, and shipping (receipts may be required).

Commitment: HSA Store SHED listings reference a two-month minimum commitment with non-refundable payments — verify current terms at checkout.

Why this fits self-employed people specifically:

If your work involves client meetings, video calls, or travel, the lozenge or sublingual route eliminates the weekly injection workflow plus the cold-chain shipping coordination. For a freelancer who travels between Airbnbs or works from coworking spaces without a fridge, this is genuinely useful.

Honest tradeoff: Compounded oral and sublingual GLP-1s are not FDA-approved finished drug products and have not been individually reviewed by the FDA for safety, effectiveness, or quality. If you specifically want an FDA-approved oral GLP-1, that’s the Wegovy pill or Foundayo via Ro, Sesame Care, or NovoCare/LillyDirect — not a compounded lozenge.

Compliance note: We don’t describe compounded oral or sublingual semaglutide as “the same as,” “equivalent to,” or “FDA-evaluated like” Wegovy or Foundayo. They are different products with different regulatory status.

5. Yucca Health — Best for project-based / lumpy income

Best for: Consultants, agency owners, and freelancers whose income comes in big chunks once or twice a quarter and need payment flexibility between client invoices.

Verified pricing (as of May 2, 2026):

- Compounded semaglutide: starting $146/month for new-patient 6-month plans

- Compounded tirzepatide: starting $258/month for new-patient 6-month plans

- Klarna, Affirm, and Afterpay accepted at checkout

Insurance: Cash-pay.

HSA/FSA: Yucca does not accept insurance. Many patients use HSA/FSA funds, but Yucca’s FAQ states it does not provide itemized receipts or letters of medical necessity — that affects HSA/FSA reimbursement defensibility, so factor this into your decision if you’re planning to claim the expense.

Cancellation: Per Yucca’s terms, subscriptions renew on schedule (monthly, quarterly, or six-month), renewals are processed 5–7 days early, and compounded medications are final sale once shipped.

Why this fits self-employed people specifically:

A consultant who just landed a $40k engagement can pay annually upfront and lock in lower per-month pricing. The next month, when no client has paid yet, BNPL (buy-now-pay-later) handles the cash flow gap without forcing a cancellation. This is a real 1099 problem most providers ignore.

Honest tradeoff: That $146/month “starting at” price requires a 6-month plan commitment. True month-to-month pricing is higher. BNPL adds consumer credit reporting if you miss a payment — it’s a tool, not free money. And the missing itemized receipts/LMNs can complicate HSA/FSA reimbursement if your administrator wants documentation. If you’re consistently struggling to make $200+/month work, the more honest answer is probably to wait until cash flow stabilizes rather than financing the medication.

Honorable mentions (briefly)

Sesame Care — Membership as low as $59/month annually with a branded GLP-1 menu (Wegovy pill, Zepbound KwikPen, Wegovy pen, Foundayo). Best as the secondary FDA-approved option after Ro when provider choice matters. Medication costs are separate.

Enhance.MD — Premium clinical feel with metabolic labs every 6 months. Core (semaglutide) at $49 first month / $212 after; Advanced (tirzepatide) at $99 / $280; Elite (sema + tirz combo) at $189 / $322. Best for higher-income self-employed buyers who want lab-guided care, especially after a plateau. Note: Enhance.MD’s FAQ states it does not accept HSA/FSA cards — reimbursement would require separate administrator verification.

Direct Meds — Direct pricing model (no subscription framing) starting at $249/month for sublingual semaglutide and $297/month for injections. HSA/FSA accepted with documentation provided.

The 12-month total cost comparison

Answer: Year 1 cash cost for compounded semaglutide programs ranges from roughly $1,800–$3,800/year depending on provider and dose. FDA-approved Wegovy or Zepbound through manufacturer self-pay programs varies significantly by drug, dose, refill timing, and promo windows. After layering HSA-paid medication and the self-employed health insurance deduction (for premiums), effective net cost can drop meaningfully for buyers in higher tax brackets.

The number that matters isn’t the first-month intro price. It’s what you actually pay over 12 months at the dose your prescriber settles on. This table assumes ongoing pricing at the dose listed; dose escalation, promo windows, and refill-timing requirements can move the actual number.

| Provider / route | Med Type | Month 1 | Month 2–12 | Year 1 cash total | HSA/FSA at checkout | Notes |

|---|---|---|---|---|---|---|

| Embody (semaglutide injection) | Compounded sema | $99 | $299 × 11 | $3,388 | Yes | Intro first-month price; needle-free GLP-1 gum option also available |

| Embody (tirzepatide injection) | Compounded tirz | $149 | $399 × 11 | $4,538 | Yes | Refills rise after intro month |

| MEDVi (semaglutide) | Compounded sema | $179 | $299 × 11 | $3,468 | Verify | FDA warning letter (Feb 20, 2026) — see disclosure |

| Ro (annual prepay) | FDA-approved brand | $39 + med | ~$74/mo + med | Membership ~$888 + medication | Verify | Insurance concierge included |

| Ro (monthly) | FDA-approved brand | $39 + med | $149 × 11 + med | Membership ~$1,678 + medication | Verify | |

| Sesame Care (annual) | FDA-approved brand | $59 + med | $59 × 11 + med | ~$708 membership + medication | Verify | Branded med costs vary |

| SHED (lozenges) | Compounded oral | $199 | $199 × 11 | ~$2,388 | Yes | Two-month minimum per HSA Store listing |

| Yucca (6-mo sema plan) | Compounded sema | $146 | $146 × 11 | ~$1,752 | Yes (no itemized receipts/LMN) | BNPL via Klarna/Affirm/Afterpay |

| Enhance.MD Core (sema) | Compounded sema | $49 | $212 × 11 | $2,381 | No (FAQ: no HSA/FSA cards) | Labs every 6 months |

| NovoCare Wegovy pill 1.5/4 mg | FDA-approved | $149 | $149 × 11 | $1,788 | Yes | 4 mg $149 offer through Aug 31, 2026 |

| NovoCare Wegovy pen (new) | FDA-approved | $199 | $199 (m2) then $349 × 10 | ~$3,888 | Yes | $199 intro through December 31, 2026 |

| LillyDirect Foundayo (low dose) | FDA-approved | $149 | $149 × 11 | $1,788 | Yes | Higher doses up to $349/mo |

| LillyDirect Zepbound | FDA-approved | varies | varies | Range varies by dose | Yes | $299–$699 by dose; Journey may be $449 |

Pricing verified May 1–2, 2026 from each provider’s pricing page or NovoCare/LillyDirect official self-pay pages. Promo windows, dose escalation, and policy changes can move these numbers. The FDA-approved row totals depend heavily on dose, medication, promo window, refill timing, and whether telehealth membership fees are separate. Re-verify before purchase.

Three takeaways for self-employed buyers:

- The cheapest first month is rarely the cheapest year. Embody’s $99 first month is the lowest entry on this list, but plan for the $299/month ongoing rate; Enhance.MD Core looks great at $49 in month one but settles at $212/month; and Yucca’s $146 starting price requires a 6-month commitment. Compare the 12-month total, not the intro price.

- Membership-plus-medication math beats medication-only sometimes — but only when insurance helps. Ro’s ~$888 annual membership + medication is the best deal if your insurance covers the medication. If it doesn’t, a cash-pay compounded program like Embody (about $99 first month, then $299/month) can be simpler to budget — just price the ongoing rate, not only the intro month.

- Brand-name pricing escalates with dose. A reader on Wegovy 0.25 mg pays $199 in months 1–2, but at the maintenance dose pays $349/month. A reader on Zepbound 2.5 mg pays $299/month, but at 10 mg pays $699/month (or $449 with the Journey 45-day refill window). Plan for the maintenance dose, not the starter dose.

Want this run for your specific situation?

Take the 60-second route quiz →Should you use insurance, HSA/FSA, or pay cash?

Answer: Always check insurance first if you have a marketplace plan (it’s free and takes minutes via Ro’s coverage checker), but don’t expect coverage for weight-loss-only Wegovy — only about 1% of federally facilitated Marketplace plans covered it per KFF’s 2024 data. Use HSA dollars when you have an HDHP and your prescriber documents the medication for a qualifying condition. Pay cash when predictability matters more than chasing coverage that probably won’t come through.

Path 1: Check insurance first if you have a marketplace plan

This is free. It takes 5 minutes. Do it before paying cash.

KFF’s June 2024 analysis of 2024 federally facilitated Marketplace plan formularies found:

- About 1% of those Marketplace prescription drug plans covered Wegovy (semaglutide for weight loss)

- About 82% covered Ozempic (same molecule, but FDA-approved for type 2 diabetes)

That gap tells you everything: insurers will cover semaglutide as a diabetes drug but rarely as a weight-loss drug. If you have type 2 diabetes, your odds change dramatically. If you don’t, expect denial — but check anyway because it’s free and there are sometimes coverage paths through obstructive sleep apnea (now an FDA-approved Zepbound indication) or cardiovascular disease (now an FDA-approved Wegovy injection indication).

State-run Marketplaces aren’t covered in the KFF analysis, so coverage there could differ. Either way, the fastest path to find out is Ro’s free GLP-1 Insurance Coverage Checker. They run the coverage check for you and produce a personalized report. No charge, no commitment.

Path 2: Use HSA/FSA dollars if you have an HDHP

If you have a high-deductible health plan (HDHP — for 2026, at least $1,700 self-only or $3,400 family deductible per IRS guidance), you can fund a Health Savings Account (HSA). 2026 HSA contribution limits:

- $4,400 for self-only coverage

- $8,750 for family coverage

HSA contributions made by self-employed people directly are deductible for federal income-tax purposes, grow tax-free, and qualified withdrawals (including for prescribed GLP-1s) are tax-free. Important caveat for self-employed people: unlike W-2 cafeteria-plan HSA contributions made through payroll, direct HSA contributions made by self-employed individuals generally do not reduce self-employment tax. Talk to your accountant before assuming SE tax savings.

The qualifying-condition rule: the medication has to be a qualified medical expense. Per IRS guidance, weight-loss treatment qualifies only when prescribed for a specific physician-diagnosed disease — obesity, diabetes, hypertension, heart disease. Cosmetic weight loss does not qualify.

For most telehealth GLP-1 prescriptions, this is straightforward — your prescriber can document obesity (BMI ≥ 30) or overweight with a comorbidity (BMI ≥ 27 with hypertension, sleep apnea, etc.) on the prescription note. If your HSA administrator asks for a Letter of Medical Necessity, ask your provider — most will issue one (Yucca is an exception per their FAQ; Enhance.MD does not accept HSA/FSA cards directly).

Which providers accept HSA/FSA at checkout (verified):

- Embody — yes, HSA/FSA cards advertised as accepted at checkout

- SHED — yes, accepted for medical prescription supplies, provider visits, and shipping

- Direct Meds — yes, with documentation provided

- NovoCare and LillyDirect — yes for FDA-approved medication

- Ro, Sesame, MEDVi — verify at checkout

- Yucca — accepts HSA/FSA cards but does not provide itemized receipts or LMNs (administrator may require these)

- Enhance.MD — does not accept HSA/FSA cards per their FAQ

Path 3: Pay cash when predictability beats chasing coverage

Pay cash when:

- Your insurance has confirmed it doesn’t cover GLP-1s for weight loss

- You don’t want to wait 3–6 weeks for prior authorization

- You want to start treatment now while your cash flow is good

- You can’t justify a higher-premium plan on the chance of GLP-1 coverage

- You’re comfortable evaluating compounded providers individually

For most self-employed buyers, this ends up being the path. Embody is a strong first stop for compounded cash-pay because of its low $99 first-month entry price, HSA/FSA cards advertised as accepted at checkout, a needle-free GLP-1 gum option, and 24/7 support. Plan for the $299/month ongoing rate.

Don’t buy a health plan just to cover Wegovy

Answer: Buying a more expensive marketplace plan in hopes of GLP-1 coverage is usually a worse deal than paying cash. Even Gold plans rarely cover weight-loss GLP-1s, and prior authorization, formulary changes, and deductibles can leave you paying the medication price anyway — on top of the higher premium.

This is the trap most “best GLP-1 for self-employed” pages won’t warn you about because there’s no affiliate revenue in talking you out of switching plans.

A typical scenario: You’re paying $400/month for a Bronze marketplace plan. You look at a Gold plan at $650/month thinking it’ll cover Wegovy. Even if it does (and it probably won’t — most marketplace plans of any tier exclude weight-loss medications), you’re paying $250 extra per month — that’s $3,000 a year — plus whatever the medication costs after deductible and coinsurance. Compare that to roughly $3,388/year all-in on Embody cash-pay (about $99 first month, then $299/month), with no premium increase.

The exception: if you have type 2 diabetes, cardiovascular disease, or obstructive sleep apnea, the math changes. Those conditions create coverage pathways for Ozempic, Wegovy, or Zepbound that don’t exist for weight-loss-only prescriptions. In that case, talk to a broker before open enrollment.

The rule for everyone else: Run the cash-pay numbers against the higher-premium plan numbers including deductible and likely denial outcomes before switching plans. Most of the time, paying cash through a transparent provider beats trying to game the marketplace.

Compounded vs. FDA-approved: which makes sense for a self-employed budget?

Answer: Compounded semaglutide and tirzepatide programs typically run $129–$329/month, while FDA-approved Wegovy, Zepbound, or Foundayo through manufacturer self-pay programs run $149–$699/month depending on dose. Compounded medications are not FDA-approved finished drug products and have not been individually reviewed by the FDA for safety, effectiveness, or quality. The choice depends on your cost tolerance, your prescriber’s clinical judgment, and how much regulatory comfort you want.

Two terms first, before anything else:

FDA-approved medication means the FDA has reviewed the specific drug for safety, effectiveness, and quality. Wegovy, Zepbound, Ozempic, Mounjaro, Foundayo, and Saxenda are FDA-approved.

Compounded medication is prepared by a state- or federally-licensed pharmacy. A 503A pharmacy fills individual patient-specific prescriptions; a 503B outsourcing facility produces in larger batches under FDA inspection. Compounded medications are not FDA-approved finished products. Whether a compounded GLP-1 is legal depends on the specific prescription, formulation, pharmacy, patient-specific documentation, and current FDA rules — not just on a provider marketing a different dose, route, or combination.

On the shortage situation: the FDA determined the tirzepatide injection shortage was resolved in late 2024 and the semaglutide injection shortage was resolved in 2025. The shortage-based enforcement discretion that allowed mass compounding ended in 2025. Compounded products that are “essentially copies” of commercially available semaglutide or tirzepatide are restricted under current FDA policy. Compounded GLP-1 telehealth offerings now generally emphasize specific formulations like alternative routes (sublingual, oral lozenges) or different concentrations.

When compounded fits a self-employed buyer

- Cost is the binding constraint and you’d rather pay $200–$300/month than not start

- A specific formulation (oral, sublingual, microdose) is appropriate per your prescriber

- You’re comfortable with the regulatory tradeoff and have read FDA’s compounded drug guidance

- You’re using a provider that names its compounding pharmacy and follows recognized standards (PCAB accreditation, USP 797 sterile compounding, USP 795 non-sterile compounding)

When FDA-approved fits a self-employed buyer

- You have any chance of insurance coverage (use Ro’s free checker)

- You want maximum HSA/FSA reimbursement defensibility

- You want the underlying clinical trial evidence (Wegovy STEP trials, Zepbound SURMOUNT trials, Foundayo ATTAIN trials)

- You want the medication’s full FDA-approved label (Wegovy now FDA-approved for cardiovascular risk reduction in obese adults with established CVD; Zepbound FDA-approved for moderate-to-severe obstructive sleep apnea)

- You have any complex medical history that makes regulatory consistency more important to you

The compliance line we hold: We do not describe compounded semaglutide or tirzepatide as “the same as,” “equivalent to,” or “FDA-evaluated like” Wegovy, Zepbound, or Foundayo. Compounded products may be compounded semaglutide or tirzepatide preparations, but they are not those FDA-approved medications and have not been individually reviewed by the FDA.

For compounded

Check EmbodyFor FDA-approved

Get Started With Ro for $39Can self-employed people deduct GLP-1 medications on their taxes?

Answer: Possibly, under specific conditions. GLP-1 medications can be a qualified medical expense if they’re prescribed for a diagnosed condition like obesity, type 2 diabetes, hypertension, or heart disease (not cosmetic weight loss), and either (a) paid through HSA/FSA dollars or (b) deducted on Schedule A if your unreimbursed medical expenses exceed 7.5% of your AGI and you itemize. You can’t double-count: HSA-paid expenses are not also Schedule A deductible.

Most self-employed people miss this conversation because their accountant doesn’t proactively raise it. A few minutes of math here can save real money.

The three tax levers a self-employed GLP-1 buyer can stack

Lever 1: HSA contributions (most powerful for most people)

- Requires an HSA-eligible HDHP (2026: at least $1,700 self-only or $3,400 family deductible)

- 2026 HSA contribution limits: $4,400 self-only / $8,750 family

- Direct contributions reduce federal income tax (and most state income taxes)

- Important caveat: direct HSA contributions by self-employed people generally do not reduce self-employment tax (W-2 cafeteria-plan HSA contributions can — yours don’t, unless your accountant has structured your business differently)

- Withdrawals for qualified medical expenses are tax-free

Lever 2: Self-employed health insurance deduction

- Above-the-line deduction reported on Schedule 1, Line 17 (calculated using IRS Form 7206)

- Doesn’t require itemizing

- Reduces AGI directly

- Covers your health insurance premiums, not the GLP-1 medication itself

- Not allowed in months you (or your spouse) had access to subsidized employer coverage

Lever 3: Schedule A itemized medical expense deduction

- Out-of-pocket medical above 7.5% of AGI

- Requires itemizing — and most self-employed people take the standard deduction (2026: $16,100 single / $32,200 married filing jointly)

- The medication itself counts here only if not paid through HSA/FSA

The tax stacking math (illustrative — not personalized advice)

These examples use federal income-tax effects only; state tax treatment varies. They do not assume self-employment tax savings on direct HSA contributions.

Example A: Solo freelancer, $80k net income, no HSA, takes standard deduction

- Compounded semaglutide via Embody: $3,388/year

- Tax positioning on the medication: none

- Net cost: $3,388/year

Example B: Solo freelancer, $80k net income, HSA-eligible HDHP, contributes $4,400 to HSA, pays $3,388 of GLP-1 from HSA

- At a 22% federal marginal income-tax rate, deducting the $4,400 contribution reduces federal income tax by about $968

- Allocating the deduction proportionally to the $3,388 spent on GLP-1: about $745 in federal tax savings on the GLP-1 portion

- State tax treatment varies — most states follow federal treatment of HSA contributions, so additional state savings may apply

- Net effective federal cost on GLP-1: roughly $2,643 (before any state tax savings)

Example C: Solo freelancer, $150k net income, no HSA but itemizes (mortgage + SALT)

- Compounded tirzepatide: $4,538/year

- Other unreimbursed medical: $1,500

- Total medical: $6,038

- 7.5% of $150k AGI = $11,250

- Medical does NOT exceed the threshold

- Net cost: $4,538/year (no medical deduction triggered)

Example D: Same as C but with a $20k surgery in the same year

- Total medical: $26,038

- Above 7.5% threshold by $14,788

- At 24% federal marginal rate: about $3,549 in federal tax savings on the deductible portion

- Allocating proportionally to the GLP-1: about $619 in federal savings attributable to the GLP-1

- Net effective cost on GLP-1: roughly $3,919

The headline: for most self-employed buyers, the HSA route saves more than itemizing. If you don’t have an HSA-eligible plan, the medication is essentially fully out-of-pocket — which makes provider selection (transparent pricing, cancellation flexibility, and a clear ongoing refill rate) much more important.

Talk to your accountant — but raise it yourself

Most accountants don’t proactively ask about GLP-1s. Bring it up:

- “I’m paying $X/month for a prescribed GLP-1. Should we capture this anywhere?”

- “I have an HDHP — would maxing my HSA be more efficient than itemizing?”

- “If I have a high-medical year, can we make sure to capture all 12 months of GLP-1 costs?”

This section is informational, not tax advice. Consult a qualified tax professional before making decisions based on tax positioning.

What if your income drops mid-year? (The 1099 cash flow problem)

Answer: Self-employed income is rarely steady, and a $200–$400 recurring expense becomes risky during slow months. The four practical strategies: choose a provider with no annual lock-in, use BNPL strategically (Yucca offers Klarna/Affirm/Afterpay), front-load HSA contributions during high-income months, and verify each provider’s specific cancellation/pause terms before signing up so a slow month doesn’t trigger a charge you can’t reverse.

Strategy 1: Avoid annual prepay if your income is volatile

Annual prepay locks you in at lower per-month pricing but kills your flexibility. Ro’s annual plan brings membership down to as low as $74/month with annual plan paid upfront — great for steady-retainer consultants, but a problem if a major client churns.

For project-based income, a month-to-month approach is safer than a long prepaid bundle. Embody starts at $99 for the first month, then $299/month ongoing — a low-commitment way to begin, as long as you budget for the ongoing rate before you sign up.

Strategy 2: Use BNPL strategically (not as a default)

Yucca Health offers Klarna, Affirm, and Afterpay at checkout. Useful when a client invoice is delayed but your medication shipment is due. BNPL is a tool, not a strategy — missed payments hit your credit.

Strategy 3: Front-load HSA during high-income months

Front-load HSA contributions during high-income months and spend down during slow months. Keep a separate HSA balance roughly equal to 6–12 months of GLP-1 costs as a buffer.

Strategy 4: Know each provider’s actual cancellation and refund rules before you sign up

Generic “most providers allow pause” advice doesn’t help when your specific provider has a final-sale rule on shipped medication. Here’s what each provider’s published terms say:

| Provider | Cancellation / refund rule (per provider’s own pages) |

|---|---|

| Embody | Cash-pay program with no insurance contract; confirm specific cancellation and refill timing during intake |

| Ro | Monthly Body membership can be canceled per Ro's terms; annual prepay is committed for the prepay period |

| MEDVi | Verify current cancellation terms directly with MEDVi before signing up |

| SHED | HSA Store SHED listings reference a two-month minimum commitment with non-refundable payments — verify at SHED checkout |

| Yucca Health | Subscriptions renew on schedule (monthly, quarterly, six-month); renewals processed 5–7 days early; compounded medications are final sale once shipped |

| Enhance.MD | Verify current cancellation and refund terms directly with Enhance.MD |

| Direct Meds | Verify current refill and cancellation terms at Direct Meds checkout |

| Sesame Care | Membership cancellation per Sesame's terms; medication purchases per pharmacy/provider |

This isn’t comprehensive — read each provider’s terms before you commit, especially before any annual prepay. Verification dates: provider terms reviewed May 1–2, 2026.

If your income is project-based and BNPL fits:

Check Yucca Health’s BNPL optionsThe hidden costs nobody puts on the comparison page

Answer: The advertised monthly price often hides shipping, labs, dose-change fees, refill fees, cancellation windows, and required commitments. Self-employed buyers who only compare the headline number can end up with a 12-month total that’s 30–50% higher than expected.

Use this checklist before you click “subscribe” on any GLP-1 program:

- First-month price (intro vs. ongoing)

- Ongoing monthly price after intro window expires

- Is medication included in the price, or separate?

- Is there a membership fee?

- Are labs required, and are they included?

- Is shipping included or separate?

- Does the price change when your dose increases?

- Is there a required commitment (2 months, 3 months, 6 months, annual)?

- What's the cancellation window — how soon before next billing?

- Refund policy on unused or shipped medication?

- Is the pharmacy named, and is it 503A or 503B?

- Is HSA/FSA accepted at checkout, or reimbursement only?

- Will the provider issue an itemized receipt or Letter of Medical Necessity?

- Does the provider operate in your state? (Verify at intake/checkout)

- Is there real prescriber support, or just chat?

Provider-specific friction examples (from each provider’s verified pages)

- Ro: Membership and medication are separate billing lines. $39 first month is membership only — medication is additional.

- Embody: Cash-pay program with no insurance contract; confirm cancellation and refill timing at intake, and note refills cost more than the $99 intro first month.

- SHED: HSA Store SHED listings reference a two-month minimum commitment with non-refundable payments.

- Yucca: That $146/month “starting at” price requires a 6-month plan; itemized receipts and LMNs are not provided per their FAQ.

- Enhance.MD: Does not accept HSA/FSA cards per their FAQ.

- MEDVi: FDA warning letter from February 20, 2026 — verify remediation status directly.

Real customer testimonials (with attribution)

Answer: We use only publicly-published, attributed testimonials about service experience — not as proof of medical outcomes. Each quote below includes the source and the provider’s own disclosure where applicable.

Ro — insurance support:

“I was not expecting insurance help.”

Yucca Health — signup speed:

“The sign up process was fast and easy.”

MEDVi — clinician interaction:

“My clinician was kind.”

Required disclaimer: Testimonials reflect individual service experiences. They are not evidence of typical medical outcomes, medication safety, or weight-loss results. We may have an affiliate relationship with the providers mentioned.

How we picked these providers (methodology)

Answer: We scored eight GLP-1 telehealth providers on six factors weighted for self-employed buyers: predictable monthly cost (25%), no employer-insurance dependency (20%), HSA/FSA acceptance and documentation (15%), cancellation and commitment clarity (15%), clinical support and access (15%), and regulatory transparency (10%). We did not rank by lowest headline price.

| Factor | Weight | Why it matters for 1099 income |

|---|---|---|

| Predictable total monthly cost | 25% | Cash flow needs certainty |

| No employer-insurance dependency | 20% | Most self-employed have no group plan |

| HSA/FSA acceptance and documentation | 15% | Tax dollars change effective cost |

| Cancellation/commitment clarity | 15% | Income fluctuates month to month |

| Clinical support and access | 15% | Real care, not just a checkout |

| Regulatory transparency | 10% | YMYL trust matters more than conversion |

What we did:

- Loaded each provider’s pricing or checkout page on May 1–2, 2026

- Pulled HSA/FSA language from each provider’s payment or FAQ page

- Verified Ro’s coverage checker and concierge language on Ro’s official insurance pages

- Cross-checked manufacturer self-pay pricing with NovoCare and LillyDirect official sources

- Checked the FDA warning letter database for any open letters against listed providers

- Reviewed IRS Publication 502, IRS Publication 969, and IRS Form 7206 instructions

- Pulled ACA Marketplace coverage data from KFF’s June 2024 analysis of 2024 federally facilitated Marketplace formularies

What we didn’t do:

- We did not purchase from each provider to test fulfillment

- We did not determine medical eligibility — that’s between you and a licensed clinician

- We did not verify insurance approval or reimbursement outcomes — those depend on your specific plan

- We did not include providers we couldn’t verify on pricing or HSA/FSA at the time of writing

If we removed every affiliate link from this page, would it still be the most useful resource for self-employed people researching GLP-1 access? That’s the test, and the answer needs to be yes.

Self-Employed GLP-1 Decision Tree

Answer: Start with the constraint that would make the wrong choice most expensive — FDA-approved-only, insurance check, predictable cash-pay, needle preference, or BNPL. The tree below routes you to the matching provider in under a minute.

1. Do you only want FDA-approved brand-name medication (Wegovy, Zepbound, Foundayo, Ozempic)?

- Yes → Start with Ro. Secondary: Sesame Care.

- No → Continue to question 2.

2. Do you have commercial or marketplace insurance worth checking before paying cash?

- Yes → Run Ro’s free coverage checker first. It’s free.

- No → Continue to question 3.

3. Are you needle-averse?

- Yes → Check SHED for lozenges, or Direct Meds for sublingual.

- No → Continue to question 4.

4. Is your income steady or project-based?

- Steady → Embody for a low first-month entry price and a needle-free GLP-1 gum option.

- Project-based / lumpy → Yucca with BNPL for cash flow flexibility.

5. Do you want metabolic labs and a more clinical experience?

- Yes → Enhance.MD (Core, Advanced, or Elite plan).

- No → Stay with Embody, MEDVi, or Yucca depending on budget.

Still uncertain?

Take the quiz below — it asks six questions and matches you to the route that fits.

Find My Self-Employed GLP-1 Route — 60-Second Quiz →Frequently asked questions

What is the best GLP-1 for self-employed people in 2026?

A strong low-cost starting point for self-employed cash-pay buyers is Embody — from $99 for the first month of compounded semaglutide injection, then $299/month ongoing, with HSA/FSA cards advertised as accepted at checkout and a needle-free GLP-1 gum option. The best route for FDA-approved brand-name medication or insurance-first checking is Ro ($39 first month, then as low as $74/month with annual plan paid upfront). A licensed clinician determines which medication, if any, is appropriate for you.

How much does a GLP-1 cost a self-employed person without insurance?

Compounded GLP-1 programs typically run $129–$329/month from telehealth providers like Embody, MEDVi, SHED, and Yucca. FDA-approved Wegovy, Zepbound, or Foundayo through manufacturer self-pay programs runs $149–$699/month depending on dose, with promo windows that can change actual paid prices. Year 1 total cost ranges from about $1,800 to over $5,400 before any tax positioning, depending heavily on which medication and which dose you settle on.

Will my ACA Marketplace plan cover Wegovy or Zepbound?

Probably not for weight loss alone. KFF's analysis of 2024 federally facilitated Marketplace plans found about 1% of those prescription drug plans covered Wegovy. The KFF analysis didn't cover state-run Marketplaces, where coverage may differ. Coverage is more likely if you have type 2 diabetes (for Ozempic or Mounjaro), obstructive sleep apnea (for Zepbound), or established cardiovascular disease with obesity (for Wegovy injection).

Can I use my HSA for compounded semaglutide?

Possibly. IRS guidance says weight-loss treatment qualifies as a medical expense only when it treats a specific physician-diagnosed disease such as obesity, diabetes, hypertension, or heart disease — not general wellness or cosmetic goals. HSA/FSA administrator documentation rules can vary, so check with your administrator before assuming. Some providers (Embody, SHED, Direct Meds) explicitly accept HSA/FSA cards at checkout; Enhance.MD's FAQ says it does not accept HSA/FSA cards; Yucca's FAQ says it does not provide itemized receipts or letters of medical necessity.

Can self-employed people deduct GLP-1 medications on their taxes?

Possibly. GLP-1 medications can be a qualified medical expense if prescribed for a diagnosed condition (obesity, type 2 diabetes, hypertension, heart disease) and either paid through HSA/FSA dollars or deducted on Schedule A above the 7.5% AGI threshold (if you itemize). Cosmetic weight-loss prescriptions don't qualify. You can't double-count: HSA-paid amounts are not also Schedule A deductible. Talk to your tax professional — this is informational, not tax advice.

Should I buy a more expensive marketplace plan to get GLP-1 coverage?

Usually no. Most marketplace plans of any tier exclude weight-loss GLP-1s, and a higher premium plus deductible plus coinsurance often costs more than paying cash through a transparent provider. The exception is if you have type 2 diabetes, cardiovascular disease, or sleep apnea, which create coverage pathways for Ozempic, Wegovy, or Zepbound that don't exist for weight-loss-only prescriptions.

What's the cheapest GLP-1 option for freelancers?

The cheapest depends on the route. For compounded cash-pay, Yucca's 6-month sema plan at $146/month and Enhance.MD Core at $49 first month / $212 after are at the low end. For FDA-approved cash-pay, Foundayo via Lilly's self-pay program starts at $149/month for the 0.8 mg dose, and the Wegovy pill via NovoCare Pharmacy is $149/month for 1.5 mg and 4 mg doses (the 4 mg $149 offer is available through August 31, 2026, after which 4 mg moves to $199/month). Embody offers a low $99 first-month entry price, HSA/FSA acceptance at checkout, and a needle-free GLP-1 gum option for self-employed buyers paying cash for compounded.

Are compounded GLP-1 medications the same as Wegovy or Zepbound?

No. Compounded products may be compounded semaglutide or tirzepatide preparations, but they are not Wegovy, Ozempic, Zepbound, Mounjaro, or Foundayo, and they have not been individually reviewed by the FDA for safety, effectiveness, or quality. Compounded products are prepared by 503A or 503B pharmacies under state and federal regulations.

Which GLP-1 provider handles prior authorization for self-employed people?

Ro is the strongest first stop. Ro's free GLP-1 Insurance Coverage Checker has an insurance specialist run the coverage check with your insurer and produce a personalized report, and Ro's concierge handles prior authorization paperwork. Ro states it cannot coordinate GLP-1 coverage for government insurance plans, with an FEHB exception.

What if my income drops and I can't afford my GLP-1 next month?

It depends on your provider's specific cancellation and refund rules. Embody is a cash-pay program with no insurance contract — confirm its specific cancellation and refill timing during intake. Ro's monthly Body membership is more flexible than annual prepay. Yucca's terms describe renewals processed 5–7 days early and final-sale rules on shipped compounded medication. SHED has a two-month minimum commitment per HSA Store listings. Don't sign up assuming you can pause freely — read the actual terms before you commit, especially before any annual prepay.

What's the new Foundayo medication?

Foundayo (orforglipron) is an FDA-approved once-daily oral GLP-1 for chronic weight management, approved by the FDA on April 1, 2026. Foundayo is not the first FDA-approved oral GLP-1 specifically for weight loss — oral Wegovy (semaglutide pill for weight loss) was FDA-approved before Foundayo. Foundayo's main differentiator is that it can be taken any time of day without food or water restrictions. Through Eli Lilly's self-pay program, Foundayo regular pricing is $149 (0.8 mg), $199 (2.5 mg), $299 (5.5 mg and 9 mg), and $349 (14.5 mg and 17.2 mg). Available through Ro, Sesame Care, LillyDirect, and Walgreens Weight Management.

What if I just lost employer coverage?

Losing job-based coverage is a qualifying life event that opens a Special Enrollment Period through HealthCare.gov — typically a 60-day window tied to the loss-of-coverage date. Don't cancel current GLP-1 care until your replacement plan is set up. Keep prior prescriptions, labs, and any denial letters. If your new plan doesn't cover GLP-1s, switch to a cash-pay provider rather than going off treatment cold.

What if I have Medicare or Medicaid?

This guide is primarily for working-age self-employed people on commercial or marketplace insurance, or paying cash. Beginning July 1, 2026, eligible Medicare beneficiaries can access all formulations of Foundayo, all formulations of Wegovy, and the Zepbound KwikPen formulation through the Medicare GLP-1 Bridge demonstration ($50/month copay for eligible participants). Medicaid coverage of GLP-1s for obesity varies by state — only 13 states cover them as of January 2026 per KFF. If you're on Medicare or Medicaid, see our Medicare GLP-1 guide instead.

The bottom line for self-employed GLP-1 buyers

The best GLP-1 for self-employed workers in 2026 isn’t a single medication — it’s the access route that fits your income, your insurance situation, and your willingness to pay cash for predictability over chasing coverage that probably won’t come.

For most self-employed cash-pay buyers, Embody is a strong first option: a low $99 first-month entry price, HSA/FSA cards advertised as accepted at checkout, a needle-free GLP-1 gum option, and 24/7 support (plan for the $299/month ongoing rate). For self-employed people with marketplace insurance worth checking — or who specifically want FDA-approved Wegovy, Zepbound, or Foundayo — Ro is the better start because of the free coverage checker, the insurance concierge, and brand-name medication at LillyDirect/NovoCare-matched pricing.

Layer on the HSA tax lever if you have an HDHP (direct contributions reduce federal income tax even though they don’t reduce self-employment tax for most direct contributors), use the self-employed health insurance deduction for premiums, and keep an eye on Schedule A medical itemizing if you have a high-medical year. A $3,400 cash-pay year often comes out closer to $2,600 in net effective federal cost for buyers who can fund an HSA — and your accountant can fine-tune from there.

You don’t need an HR department to figure this out. You just need the right route.

Most cash-pay buyers

See Embody PricingInsurance-first / FDA-approved

Check Ro Insurance CoverageStill not sure which GLP-1 program is right for you?

Take our free 60-second matching quiz →Related guides on Weight Loss Provider Guide

- Highest-rated GLP-1 telehealth providers (general)

- GLP-1 providers that handle prior authorization

- HSA/FSA-eligible GLP-1 providers

- Cheapest FDA-approved GLP-1

- Compounded GLP-1 providers (503A)

- Oral and needle-free GLP-1 options

- 503B outsourcing facility providers

- Medicare and Medicaid GLP-1 coverage

- Cheapest GLP-1 without insurance

- Cheapest tirzepatide without insurance

Sources and verification

- KFF, “Costly GLP-1 Drugs Are Rarely Covered for Weight Loss by Marketplace Plans” (June 2024 analysis of 2024 federally facilitated Marketplace formularies)

- KFF, “Medicaid Coverage of and Spending on GLP-1s” (January 2026 update)

- IRS Topic 502, Medical and Dental Expenses

- IRS Publication 502, Medical and Dental Expenses

- IRS Publication 969, Health Savings Accounts and Other Tax-Favored Health Plans

- IRS Form 7206 instructions (Self-Employed Health Insurance Deduction)

- IRS FAQ on medical expenses related to nutrition, wellness, and general health

- IRS Revenue Procedure 2025-19 (2026 HSA/HDHP inflation-adjusted limits)

- IRS news release on 2026 inflation-adjusted standard deduction amounts

- HealthCare.gov self-employed coverage and Special Enrollment Period guidance

- HealthCare.gov HSA-eligible plan guidance

- FDA, “FDA Clarifies Policies for Compounders as National GLP-1 Supply Begins to Stabilize”

- FDA Warning Letter Database (MEDVi LLC dba MEDVi, 721455, February 20, 2026)

- FDA news release on Foundayo (orforglipron) approval

- Ro official “How Our Weight Loss Program Works,” GLP-1 Insurance Coverage Checker, and Zepbound KwikPen pages

- Embody (joinem.co) official program, pricing, and HSA/FSA pages

- MEDVi official program pricing and testimonial pages

- Sesame Care official online weight-loss program pricing

- SHED (ShedRx) GLP-1 lozenges product and FSA/HSA pages; HSA Store SHED listing terms

- Yucca Health official GLP-1 plan pricing, FAQ, and terms pages

- Enhance.MD official Core, Advanced, and Elite plan pages and FAQ

- Direct Meds official pricing and HSA/FSA acceptance page

- NovoCare Pharmacy official Wegovy self-pay pricing pages

- LillyDirect official Foundayo and Zepbound self-pay pricing and Self Pay Journey Program terms

- Centers for Medicare & Medicaid Services (CMS) official Medicare GLP-1 Bridge program guidance

Pricing, policies, and regulatory information were verified May 1–2, 2026. We reverify periodically and update this page on a quarterly schedule, with hard refresh dates calendared to manufacturer promo expirations and FDA policy changes. Please re-check provider pages directly before purchasing — pricing can shift without notice.

Weight Loss Provider Guide is an independent comparison resource for GLP-1 telehealth providers. We may earn a commission when readers sign up through our affiliate links. Affiliate relationships do not influence our editorial scoring or recommendations. We are not a medical authority, a pharmacy, or a tax advisor — please consult qualified professionals before acting on any information in this guide.