Best GLP-1 Provider for Medicare Patients With No Prior Authorization: What Actually Works in 2026

By the Weight Loss Provider Guide editorial team — an independent comparison resource for GLP-1 telehealth providers. Some links below are affiliate links; we may earn a commission at no extra cost to you. It never changes our ranking. We rank by what’s true for your situation first — and on this page, that means telling you when not to pay us anything. Affiliate disclosure

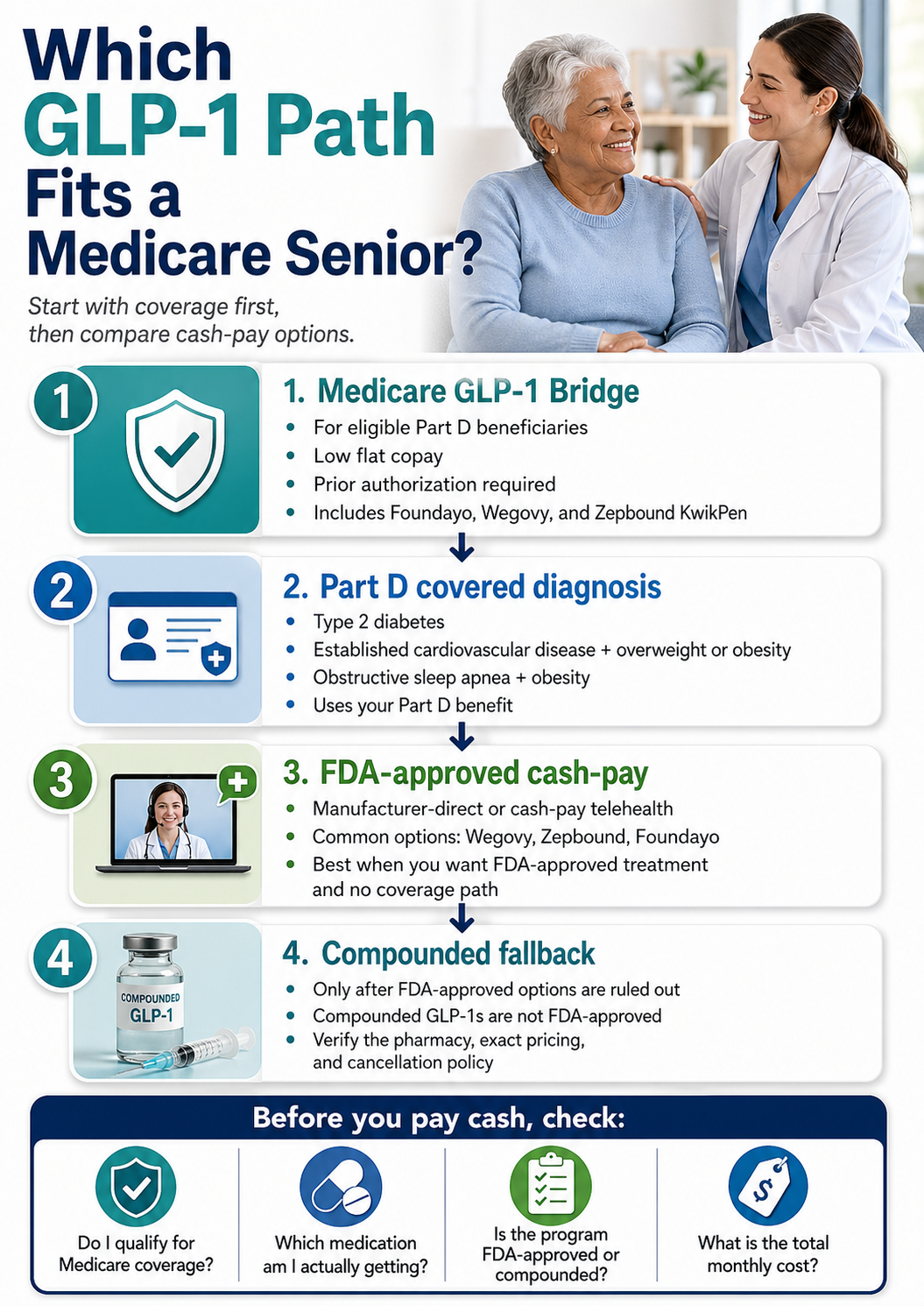

If you searched for the best GLP-1 provider for Medicare patients with no prior authorization, here is the honest answer most pages won’t give you: there isn’t one — not the way you’re picturing it. Every Medicare path that helps pay for a GLP-1 involves the insurance approval process. The brand-new $50-a-month Medicare program starting July 1, 2026 requires prior authorization. Standard Part D coverage usually adds prior authorization, step therapy, or quantity limits on top of plan rules. The only way to get a GLP-1 with truly zero prior authorization is to pay cash and leave insurance out of it. For most Medicare patients, that’s the wrong move. For some, it’s exactly the right one. Below, we’ll show you which group you’re in — and the cleanest path for each.

The fast verdict (so you can stop scrolling)

- →

Want Medicare to help pay? Expect paperwork. The $50/month Bridge requires prior authorization; Part D plans usually have their own rules too. It’s almost always cheaper than cash, so the paperwork is usually worth it.

- →

Likely qualify for the $50/month Medicare Bridge, or have a covered indication (type 2 diabetes, established cardiovascular disease, or moderate-to-severe sleep apnea)? That path will almost certainly beat cash. Full stop.

- →

Been denied, can’t wait until July, or simply want it now with no insurance paperwork? Pay cash through an FDA-approved telehealth provider. Ro is our top pick — Wegovy, Zepbound, and Foundayo at manufacturer-matched prices, no insurer, no prior authorization. Get started for $39, then as low as $74/month for the membership, plus medication from $149/month.

- →

Want more medication choices and a real video visit with a doctor you pick? Sesame Care is the strong alternative, with a care fee from $59/month.

Not sure which group you’re in? That’s the whole game.

Take the free 60-second matching quiz →The one table that answers the whole question

Nobody else puts this in one place. Here is every Medicare and cash-pay GLP-1 path side by side.

The Medicare GLP-1 No-Prior-Authorization Pathway Matrix — verified May 28, 2026

| Your path | Uses Medicare? | Prior auth? | FDA-approved meds? | Real cost signal | Best for | Verified via |

|---|---|---|---|---|---|---|

| Medicare GLP-1 Bridge | Yes (runs outside normal Part D) | Yes | Yes — Foundayo, Wegovy, Zepbound KwikPen | $50/month copay | Part D members who meet BMI rules and can wait until July 1, 2026 | CMS Medicare GLP-1 Bridge page |

| Part D for a covered indication | Yes | Plan-specific (often PA, step therapy, or quantity limits) | Yes — when used for a covered indication | Your plan's copay (2026 Part D cap: $2,100/yr) | People prescribed for type 2 diabetes, Wegovy's CV-risk indication, or Zepbound's OSA indication | Medicare.gov; KFF |

| Ro — cash-pay | No | No (no insurer involved) | Yes | Membership: $39 first month, then $149/mo — or as low as $74/mo annual; meds from $149/mo | Medicare patients who want FDA-approved meds now, no paperwork, and can pay cash | ro.co pricing & insurance pages |

| Sesame Care — cash-pay | No (for the program) | No (no insurer involved) | Yes | Care fee from $59/mo annual ($99/mo standard); meds separate | People who want a broad med menu, a video visit, and to pick their provider | sesamecare.com |

| Manufacturer-direct (LillyDirect / NovoCare) | No (if self-pay) | No (cash) | Yes | Varies by drug and dose — lower-dose oral options start ~$149/mo; injectable forms can run $349–$499+/mo | People who already have a prescriber | LillyDirect; NovoCare |

| Compounded cash-pay | No | No (cash) | No — not FDA-approved | Varies | Only when FDA-approved drug isn't medically appropriate or commercially available — see FDA note below | FDA guidance |

Does Medicare cover GLP-1s for weight loss right now?

No. As of 2026, Medicare does not cover GLP-1 drugs when they’re prescribed only for weight loss. It can cover them for other FDA-approved reasons — and even then, plan rules like prior authorization or step therapy usually apply. This is set to change in a limited way starting July 1, 2026, through a temporary program we’ll explain below.

For years, Medicare was barred by law from paying for weight-loss drugs. That rule still applies. What changed is that Medicare now covers some GLP-1s when your doctor prescribes them for a medical condition the drug is approved to treat:

- ·Ozempic, Mounjaro, Rybelsus — may be covered when used for type 2 diabetes.

- ·Wegovy — may be covered for adults with established cardiovascular disease who are also overweight or obese, to reduce the risk of heart attack and stroke.

- ·Zepbound — may be covered when used for moderate-to-severe obstructive sleep apnea in adults with obesity.

If that describes you, you may already have a path through your regular Part D plan today. If you just want a GLP-1 to lose weight and you don’t have one of those conditions, Medicare won’t pay for it right now — and that’s the gap the new Bridge program is meant to fill.

Does Medicare require prior authorization for GLP-1 medications?

For practical purposes, yes. The new Medicare GLP-1 Bridge specifically requires your doctor to submit a prior-authorization attestation before you can get the medication. Standard Part D coverage for a covered indication typically comes with plan rules — prior authorization, step therapy (try a cheaper drug first), or quantity limits. There is no realistic Medicare path where you walk straight into the pharmacy with no paperwork between your doctor and your plan.

Let’s clear up what “prior authorization” even means, because it causes most of the confusion. Prior authorization (PA) is just the insurance company’s permission slip. Before they’ll pay, they make your doctor send paperwork proving you meet their rules. It’s annoying. It causes delays. It’s why people get denied. We get why you want to avoid it.

The expensive trap to avoid

People type “no prior authorization” when what they really mean is “no paperwork, no delay, no denial, no surprise bill.” So they go looking for a provider that promises “no PA” — and they find one. What they often don’t realize is why that provider has no PA: it’s because that provider isn’t using insurance at all. You’re paying cash. “No prior authorization” and “no insurance” are usually the same sentence.

So when a telehealth ad says “no prior authorization,” ask: “Does that mean no insurance is being used, and I’m paying full price myself?” Nine times out of ten, the answer is yes.

The $50/month Medicare GLP-1 Bridge (starts July 1, 2026)

The Medicare GLP-1 Bridge is a temporary CMS demonstration that lets eligible Medicare Part D members get certain weight-loss GLP-1s for a flat $50 a month, from July 1, 2026 through December 31, 2027 (per CMS). It is not a no-prior-authorization program — your doctor still has to submit a PA request — but at $50 a month, it’s the cheapest legitimate path for people who qualify.

If you can possibly use this, you should. Cash-pay can’t touch $50. Here’s how it works.

Which drugs the Bridge covers

The Bridge covers these three, and only when prescribed for weight loss (per CMS):

- ✓Foundayo (orforglipron — Eli Lilly's newer GLP-1 pill), all forms

- ✓Wegovy (semaglutide), both the injection and the tablet, all forms

- ✓Zepbound KwikPen (tirzepatide) — the KwikPen only, not the single-dose vials or pens

Mounjaro and Ozempic are not on the Bridge list. Those carry a diabetes label, so if you need them, they run through your regular Part D plan instead. If you’re already getting Wegovy for cardiovascular-risk reduction or Zepbound for obstructive sleep apnea, those uses go through your normal Part D plan too — not the Bridge.

Who qualifies

You must be enrolled in a Medicare Part D plan (either a standalone drug plan or a Medicare Advantage plan with drug coverage) in 2026. Then you have to meet one of three medical “tiers.” Importantly, your doctor checks these based on the date you first started a GLP-1 — not your numbers today (per CMS). So if you started Wegovy two years ago at a BMI of 37 and you’ve since dropped to 33, you can still qualify.

BMI of 35 or higher — no other condition needed.

BMI of 30 or higher, plus one of: heart failure with preserved ejection fraction, uncontrolled high blood pressure (above 140/90 even while on two blood-pressure medications), or chronic kidney disease stage 3a or higher.

BMI of 27 or higher, plus one of: prediabetes, a past heart attack, a past stroke, or symptomatic peripheral artery disease (poor circulation in the legs).

All three tiers also require pairing the medication with structured lifestyle changes — nutrition and physical activity — consistent with the drug’s FDA-approved label.

What it costs — and the catches

You pay $50 a month, no matter the dose, no matter which of the three drugs. Behind the scenes, manufacturers accept a $245 net price and Medicare covers the rest through a special payment flow run by Humana (the central processor). Read this part carefully, because it surprises people:

- !The $50 does not count toward your Part D out-of-pocket cap of $2,100. The Bridge runs on its own track, separate from your normal drug benefit.

- !Manufacturer coupons and savings cards can't be applied to Bridge claims.

- !It's temporary. It runs through December 31, 2027. A longer-term program (the "BALANCE Model") is supposed to take over for 2027 and beyond, but it's voluntary for insurance plans and KFF notes the post-2027 path isn't guaranteed for every beneficiary. Don't build a five-year plan around the Bridge.

Bring this to your doctor (Bridge readiness checklist)

The Bridge starts July 1, 2026. If you want to be ready on day one, walk into your next appointment with these answers and ask your provider to start the paperwork.

- Your BMI on the day you first started a GLP-1 (or current BMI if you haven't started one). This number — not today's — sets your tier.

- Which tier you're claiming: BMI ≥35 alone, BMI ≥30 plus a Tier 2 condition, or BMI ≥27 plus a Tier 3 condition.

- Documentation of the qualifying condition (if BMI is under 35) — date diagnosed, who diagnosed it, current management.

- The Bridge drug you're requesting: Foundayo, Wegovy injection, Wegovy tablet, or Zepbound KwikPen.

- Your lifestyle-modification plan (nutrition + activity consistent with the FDA label).

- Your Part D plan information (PDP or MA-PD).

- Confirmation your prescriber isn't on Medicare's Preclusion List. Per CMS, prescribers don't have to be enrolled in Medicare to write a Bridge prescription, but they can't be on the Preclusion List.

- Where the PA goes: to the central processor (Humana) — not your Part D plan.

Think you might qualify? Get the paperwork ready before July so you’re not waiting.

Take the free 60-second matching quiz →So what’s the only way to get a GLP-1 with no prior authorization?

You pay cash and leave insurance out of it. When no insurer is involved, there’s nothing to “authorize” — so there’s no prior authorization, no insurance denial letter, and no PA wait. FDA-approved options through telehealth start around $149 a month for the medication, plus a membership fee. The trade-off is real: Medicare pays nothing, and you cover the full cost. (Of course, a licensed clinician still has to review your health and approve the prescription — no telehealth bypasses that — but you’re not waiting on an insurance company.)

This is the honest center of the whole question. “No prior authorization” lives on the cash-pay side of the line. The moment you ask Medicare (or any insurer) to chip in, paperwork comes with it.

Now, here’s the detail that even most affiliate pages get wrong — and it matters most for you specifically as a Medicare patient.

You may have seen telehealth ads bragging about “$25 a month” GLP-1s, or manufacturer savings cards that knock hundreds off the price. Those deals do not apply to Medicare patients. The Novo Nordisk and Eli Lilly copay programs specifically exclude anyone enrolled in a federal or state health program with drug coverage — which includes Medicare. So when a Medicare patient goes “cash-pay” through a telehealth provider, they pay the full cash price, not the discounted one a younger, commercially-insured person might get.

That’s exactly why we keep pushing you to check real coverage first. If you qualify for the Bridge, $50 beats the cash price every time. Cash-pay is the right answer only if one of these is true for you:

- ·You don't qualify for the Bridge or a covered indication.

- ·You can't wait until July 1, 2026.

- ·You were denied and don't want to fight an appeal.

- ·You simply value getting it now with zero insurance paperwork, and you can afford the full cash price.

If that’s you, keep reading. If it’s not — go pursue your coverage. We’d rather lose the click than send you to pay $200 a month when you could be paying $50.

When is Sesame Care the better choice?

Sesame Care is the better pick when you want a broad medication menu, a lower monthly care fee, or a real video visit with a provider you choose. Its weight-loss program (“Success by Sesame”) starts at $59 a month on an annual plan, with medication billed separately. Like Ro, it’s cash-pay and doesn’t bill Medicare for the program (per sesamecare.com).

Quick verify on Sesame

- ·Care fee: From $59/month on an annual plan, $99/month on the standard 28-day cycle. Medication is not included.

- ·Medication menu: One of the broadest in telehealth — Wegovy (pen + pill), Zepbound, Mounjaro, Ozempic, Saxenda, Rybelsus, plus oral options.

- ·Costco-member pricing: Through Costco's Member Prescription Program (CMPP), Costco members may see self-pay GLP-1 pricing such as Wegovy or Ozempic injection offers around $349/month, and the Wegovy tablet starting around $149/month. Important: Costco says CMPP is not insurance and isn't available when claims are submitted through Medicare, Medicaid, other publicly funded programs, or private insurance.

- ·Insurance help: Sesame providers can assist with prior-authorization paperwork for commercial insurance. Medicare and Medicaid generally don't cover GLP-1s for weight loss, so don't treat Sesame as a Medicare-coverage path.

Choose Sesame if:

- ✓You want options. A broad menu means your provider can match the drug to you, not the other way around.

- ✓You want a lower care fee. At $59/month annual, it runs below Ro's membership.

- ✓You want to pick your doctor and see them on video.

- ✓You're a Costco member and want cash-pay manufacturer-matched pricing through that channel.

More medication choices and a lower care fee, with a provider you pick?

See Sesame Care’s weight-loss program and pricing →Affiliate link

Can Ro or Sesame handle Medicare prior authorization for me?

For Medicare specifically: don’t count on it. Both Ro and Sesame can help with prior-authorization paperwork for people with commercial insurance. But Medicare generally doesn’t cover GLP-1s for weight loss, so for Medicare patients these are cash-pay paths, not Medicare-coverage paths. Treat them as the no-PA cash option, not as a way to get Medicare to pay.

This is the misunderstanding that costs people money, so let’s nail it down. Four phrases that sound alike but mean very different things:

"We handle prior authorization"usually means commercial insurance."We accept cash-pay"means no insurance is used at all."Medicare patients can join"means you're welcome to pay cash — not that Medicare pays."No prior authorization"almost always means no insurance is billing.What’s the cheapest GLP-1 path for Medicare patients with no prior authorization?

It depends on whether “no prior authorization” matters more to you than “lowest cost.” If you qualify for the Bridge, $50 a month is almost certainly your cheapest option — but it requires PA. If avoiding PA is non-negotiable, FDA-approved cash-pay starts around $149/month for the medication plus a care fee, and there’s no insurance paperwork. You usually can’t have the lowest price and zero paperwork.

| Your situation | Likely cheapest path | Prior auth? | Rough monthly cost |

|---|---|---|---|

| Likely qualifies for the Bridge and can wait until July | Medicare GLP-1 Bridge | Yes | $50 |

| Has type 2 diabetes, established cardiovascular disease, or moderate-to-severe sleep apnea | Part D through your prescriber | Plan-specific | Your plan's copay |

| Wants no insurance PA, already has a doctor | Manufacturer-direct cash | No insurer | Drug/dose-dependent |

| Wants no insurance PA + telehealth support | Ro or Sesame (cash) | No insurer | $149+/mo meds + care fee |

| Wants cheapest cash and understands the tradeoff | Compounded (not FDA-approved) | No insurer | Varies — read the FDA note below first |

Should I skip prior authorization or wait for the Medicare Bridge?

If you’re likely Bridge-eligible and can wait until July 1, 2026, waiting will almost certainly save you a lot of money. If you can’t wait, don’t qualify, or value speed over savings, cash-pay is the cleaner no-PA route.

Wait for the Bridge if:

- ·You're on a Part D plan (or MA with drug coverage).

- ·You likely meet one of the three BMI tiers.

- ·You can wait until July.

- ·Your doctor is willing to submit the PA.

- ·Saving real money is worth a little paperwork.

Go cash-pay (skip PA) if:

- ·You need to start before July.

- ·You were denied and don't want to appeal.

- ·Your situation doesn't qualify for any coverage.

- ·You can afford $149+/month for medication plus a care fee.

- ·You want FDA-approved treatment with no insurance hassle.

Don’t skip PA if:

- ·You have T2D, established CVD, or moderate-to-severe OSA and might qualify through Part D.

- ·You're clearly Bridge-eligible — $50 is hard to beat.

- ·Paying full cash would genuinely strain your budget.

If speed matters more than getting Medicare to pay, the cash-pay route is built for your situation.

Compare FDA-approved no-PA options on Ro →Should Medicare patients use FDA-approved or compounded GLP-1s first?

For Medicare patients, FDA-approved options are our default recommendation. FDA-approved drugs — Wegovy, Zepbound, Foundayo, Ozempic, Mounjaro — have gone through FDA review for safety, effectiveness, and quality. Compounded drugs have not. The FDA says compounded GLP-1 medication may be appropriate only when a patient’s medical needs cannot be met by an FDA-approved drug, or when the approved drug is not commercially available — not as a general lower-cost substitute.

We’re not here to lecture you. But for an audience that’s more likely to be managing heart, kidney, or blood-pressure conditions, the FDA-approved path is the safer default — and it’s the only path the Medicare Bridge covers anyway.

⚠️ A note from the FDA, in plain terms

Compounded drugs are not FDA-approved. The FDA reviews approved drugs for safety, effectiveness, and quality before they reach you; compounded products skip that review. The FDA has also warned about dosing errors, salt forms of semaglutide, adverse-event reports, counterfeit products, and unapproved online GLP-1 products. We never describe compounded medication as “the same as” Wegovy, Zepbound, or any other brand drug — because the FDA hasn’t reviewed it the same way. For full Important Safety Information on FDA-approved GLP-1s, see the FDA’s approved labeling and the manufacturer’s prescribing information for each drug. (Source: U.S. Food and Drug Administration.)

What to ask before you pay for any “no prior authorization” GLP-1 program

Before you enter a card number, get clear answers — because “no PA” is often a clue that you’re paying full price out of pocket. The goal is to never confuse “no prior authorization” with “Medicare covered.”

Ask these, in order:

- 1Does "no prior authorization" mean I'm paying cash and not using Medicare? (Usually yes.)

- 2Is the medication FDA-approved or compounded?

- 3What is the total monthly cost after the first month? (Intro prices end.)

- 4Is the care/membership fee separate from the medication? (It almost always is.)

- 5Can Medicare patients actually use any discount or copay card here? (Usually no — Medicare and other federal-program enrollees are excluded.)

- 6Can I cancel before the next refill bills me?

- 7Which pharmacy fills the prescription, and is it shipped to me?

- 8What happens if the medication isn't right for me medically?

What we actually verified

We don’t ask you to take our word for it. Here’s exactly what we checked, and when.

✅ Verified May 28, 2026

- ·Medicare doesn't cover GLP-1s for weight loss alone but may cover them for FDA-approved indications (CMS; KFF; Medicare.gov).

- ·The Medicare GLP-1 Bridge requires prior authorization. Part D plans typically use PA, step therapy, or quantity limits (CMS; Medicare.gov).

- ·Bridge dates (July 1, 2026 – Dec 31, 2027), $50 copay, covered drugs (Foundayo, Wegovy injection + tablet, Zepbound KwikPen) (CMS Medicare GLP-1 Bridge page).

- ·Bridge eligibility tiers (BMI 35; BMI 30 + Tier 2 condition; BMI 27 + Tier 3 condition), assessed at the time GLP-1 therapy started; manufacturer net price $245; central processor Humana (CMS).

- ·The $50 Bridge copay does not count toward your Part D out-of-pocket cap (CMS).

- ·Post-2027 BALANCE Model is voluntary for Part D plans; KFF notes the post-2027 path isn't guaranteed for every beneficiary (KFF).

- ·Ro is cash-pay; does not bill Medicare; concierge supports commercial-insurance PA; membership $39 first month, then $149/mo or as low as $74/mo annual; medication from $149/mo, manufacturer-matched (ro.co pricing and insurance pages).

- ·Sesame care fee from $59/mo annual ($99 standard); medication separate; broad FDA-approved menu; Costco CMPP is not insurance and excludes claims submitted through Medicare/Medicaid/other public programs or private insurance (sesamecare.com; costco.com).

- ·Manufacturer copay/savings cards exclude federal-program (Medicare) patients (Novo Nordisk and Eli Lilly program terms).

- ·FDA's position on unapproved and compounded GLP-1 drugs (fda.gov).

🔍 What we did NOT do (so you can judge for yourself)

- ·We did not enroll in each program or submit a test Bridge prior authorization.

- ·We did not verify every state’s checkout flow or live inventory by ZIP code.

- ·Prices and program rules change. Always confirm current pricing on the provider’s own site, and confirm Bridge details with your Part D plan or 1-800-MEDICARE, before you decide.

How we ranked these providers

We ranked by Medicare fit and honesty first — not by what pays us most. A provider scores highest when it clearly separates cash-pay from Medicare coverage, offers FDA-approved options, shows real prices, and doesn’t pretend it can make Medicare pay.

| What we score | Weight |

|---|---|

| Clear, honest Medicare/insurance explanation | 25% |

| FDA-approved cash-pay access | 20% |

| Total-cost transparency | 15% |

| Honesty about prior authorization | 15% |

| Easy to start / care model | 10% |

| Provider support and follow-up | 10% |

| Easy to cancel / low pricing friction | 5% |

What consistently trips Medicare GLP-1 shoppers up

From reading public reviews and forum threads about telehealth GLP-1 programs, four objections show up over and over before people pay. We grouped them so you don’t fall into the same traps:

"I don't want to wait weeks for prior authorization."

Fair — but only cash-pay avoids it, and Medicare won't pay if you go that route.

"I thought the monthly fee included the medication."

It almost never does. Care fees and medication are billed separately at every major telehealth provider.

"Does Medicare cover this or not?"

Sometimes, for a covered indication — never for weight loss alone, until the Bridge.

"Can I use Medicare and still just pay out of pocket?"

Yes — but if you pay cash, Medicare isn't paying, and you can't use the manufacturer copay cards either.

Frequently asked questions

The bottom line

Here’s the truth we wish someone had handed you at the start. The cheapest Medicare path is not the no-paperwork path, and the no-paperwork path is not Medicare-covered. Once you see that clearly, the decision gets easy: if you can get Medicare to help pay — through the $50 Bridge or a covered indication — do it, paperwork and all. If you can’t, or you won’t wait, FDA-approved cash-pay through Ro (or Sesame) is the clean, no-prior-authorization way to start now.

You’ve been thinking about this for a while. You’re allowed to do this. The only thing left is picking the path that actually fits your situation.

Still not sure which GLP-1 program is right for you?

Take the free 60-second matching quiz. Find My GLP-1 Path →Medical and coverage information on this page is for general education and reflects what we verified as of May 28, 2026. It is not medical advice. Talk to your doctor about whether a GLP-1 is right for you, and confirm current coverage with your Medicare Part D plan or 1-800-MEDICARE. Weight Loss Provider Guide is an independent comparison resource for GLP-1 telehealth providers; we may earn a commission from some links, which never affects our rankings.

Sources

- ·CMS — Medicare GLP-1 Bridge program page (cms.gov)

- ·CMS — Press release on $50 monthly access

- ·KFF — What to Know About the BALANCE Model and the Medicare GLP-1 Bridge

- ·Medicare.gov — Part D coverage rules (PA, step therapy, quantity limits)

- ·Humana — Does Medicare Cover GLP-1 Weight Loss Drugs?

- ·Wellcare — Understanding GLP-1 Coverage in 2026

- ·NPR — New Medicare option for weight-loss drugs ($50 copay)

- ·Healthline — GLP-1 Insurance Coverage for Weight Loss: 2026 Guide

- ·U.S. News — Navigating Insurance Coverage for GLP-1 Medications

- ·Ro — Weight Loss Pricing, Insurance, and GLP-1 Insurance Coverage Checker pages (ro.co)

- ·Sesame Care — Online Weight Loss Program page (sesamecare.com)

- ·Costco — Member Prescription Program terms (costco.com)

- ·Novo Nordisk and Eli Lilly — published copay/savings program terms

- ·U.S. Food and Drug Administration — Concerns with Unapproved GLP-1 Drugs Used for Weight Loss (fda.gov)

Related Articles

Best Foundayo Providers That Accept Insurance

Verified comparison of Foundayo telehealth providers that accept insurance — coverage checker tools, prior authorization support, cost by insurance lane, Medicare GLP-1 Bridge details, and…

Best GLP-1 Provider for Medicare Bridge PA

The $50 Medicare GLP-1 Bridge starts July 2026. See exactly who can submit your prior authorization, who qualifies, and what to verify before you pay.

Best GLP-1 Provider With Patient Assistance 2026

Best GLP-1 provider with patient assistance in 2026: the free PAPs skip Wegovy and Zepbound. See the $25, $50, and $149–$699 paths that actually work.

Best GLP-1 Providers After Insurance Denial (2026 Guide)

GLP-1 denied by insurance? Appeal it, get FDA-approved Wegovy or Zepbound from $149–$449/mo, or use the new $50 Medicare Bridge — your 2026 options.

Best GLP-1 Providers If Insurance Denies Wegovy

Denied Wegovy? Compare the 3 real paths — appeal help, cash-pay direct, FDA-approved switch — with verified May 2026 prices and the best provider for each.

Best GLP-1 Providers If Insurance Denies Zepbound 2026

Denied for Zepbound? Your 4 paths — appeal, switch to Wegovy, $299/mo LillyDirect cash, or alternatives. Real 2026 prices verified.