How Long Does Prior Authorization Take for GLP-1?

Last verified: April 7, 2026 · Written by WPG Research Team

If you're wondering how long does prior authorization take for GLP-1, many complete requests are decided within 2–7 days. Faster electronic reviews can come back within 24–72 hours. But missing documentation, manual review, plan rules, and appeals can push the timeline to 14 days or longer — and if you're denied and need to appeal, the full process can stretch well past a month.

Here's what most pages won't tell you: documentation completeness is one of the biggest drivers of your timeline. Whether your doctor's office submits everything the insurer needs on the first try often matters more than which drug you were prescribed or which insurer you have. That single factor is the difference between a 48-hour approval and a 6-week ordeal.

But it's not the only factor. Your plan's criteria, the drug's indication (weight loss vs. diabetes vs. cardiovascular), whether the request triggers manual clinical review, and your specific PBM's processing speed all play a role. If you're sitting here wondering whether your wait is normal or something went wrong — keep reading.

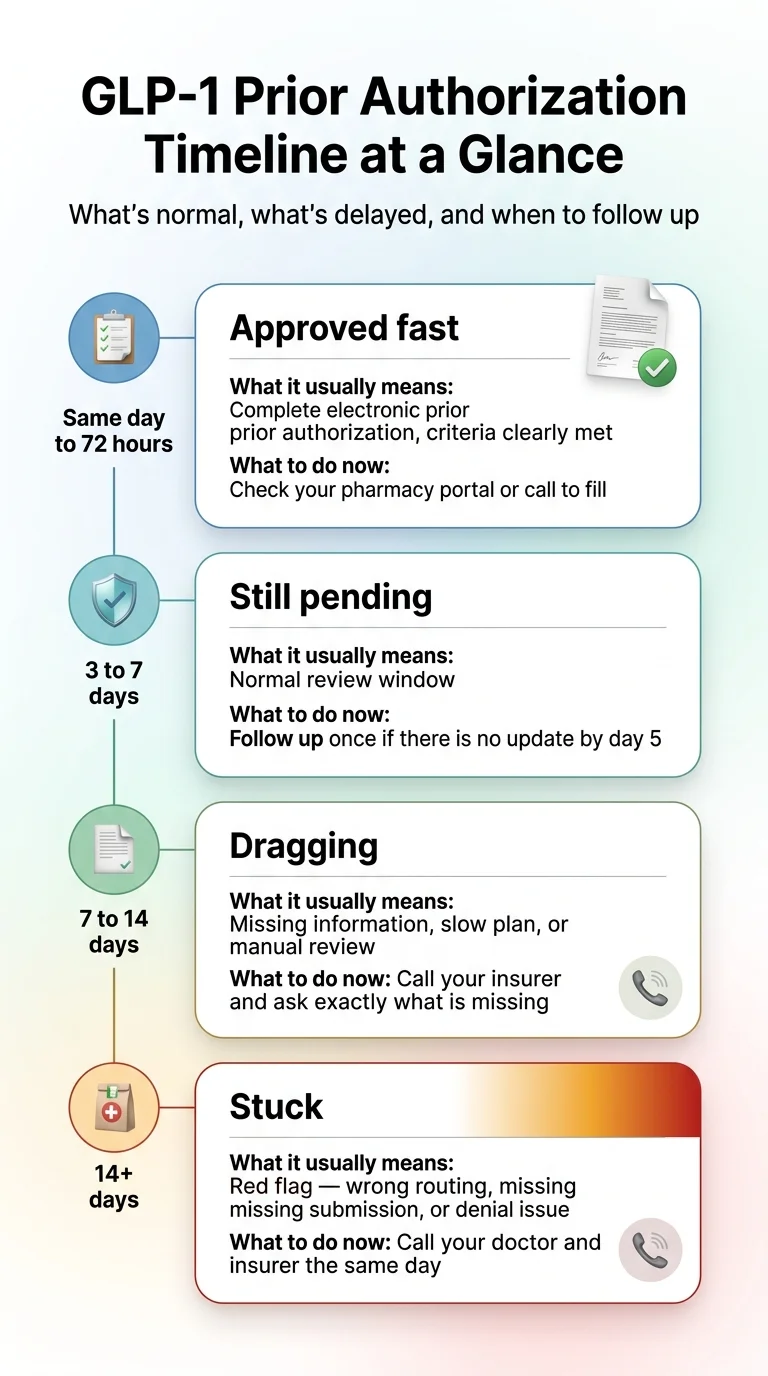

GLP-1 Prior Authorization Wait Times at a Glance

What it means: Complete ePA, criteria clearly met, auto-approval

What to do: Check your pharmacy portal or call to fill

What it means: Normal review window for most plans

What to do: Follow up once if no update by day 5

What it means: Missing info, slow plan, or manual review triggered

What to do: Call insurer — ask exactly what's missing

What it means: Red flag — possible wrong routing, missing submission, or denial already issued

What to do: Call your doctor AND insurer the same day

What it means: You're now in a separate appeal process

What to do: Get the denial reason in writing and start your appeal promptly

Sources: Blue Shield of California, Express Scripts, UnitedHealthcare, Aetna, CMS. Full sourcing in How We Verified This Page.

What Is a "Normal" GLP-1 Prior Authorization Timeline?

Many complete GLP-1 prior authorization requests are decided in 2–7 days. Fast plans and PBMs can approve in under 24 hours, while others may take up to 14 days. If you're past two weeks without a clear answer, that's a signal something needs your attention — not more patience.

Verified Insurer and PBM Timelines

| Organization | Published timeline | Scope | Verified |

|---|---|---|---|

| Blue Shield of California | 24–72 hours | Pharmacy PA requests (plan-specific) | April 2026 |

| Express Scripts | Nearly all within 2 business days with complete info; ePA may return decisions within minutes | PBM-wide FAQ | April 2026 |

| UnitedHealthcare (TX Community Plan) | 3 business days when complete; no later than day 10 from original receipt if incomplete | Specific UHC plan — timelines vary by state and plan type | April 2026 |

| Aetna (Medicare member materials) | Up to 2 weeks | Aetna Medicare plans specifically | April 2026 |

| CMS rule (impacted payers) | 72 hours expedited / 7 calendar days standard | Regulatory requirement for impacted payers — not a universal pharmacy PA promise | April 2026 |

These are specific published examples, not universal guarantees. Your plan's timeline may differ. But they give you a realistic range to measure your own experience against.

A Better Rule of Thumb

- Day 0–3:Don't panic. Check your insurer's portal to confirm the request exists.

- Day 4–7:Follow up once. Call your insurer. Confirm receipt and ask if anything is missing.

- Day 8–14:Something is likely incomplete or in manual review. Get specific: ask what document, code, or form they're waiting on.

- Day 14+:Stop waiting passively. This is a workflow problem, not a patience problem.

What real patients report about their wait times:

"Mine took less than a day." — r/Zepbound

"Mine was approved within 2 days." — r/Zepbound

"I've been waiting 3 weeks and insurance says they've received nothing." — r/Zepbound

"A lot of times it's because the doctor's office didn't complete all the documentation." — r/Zepbound

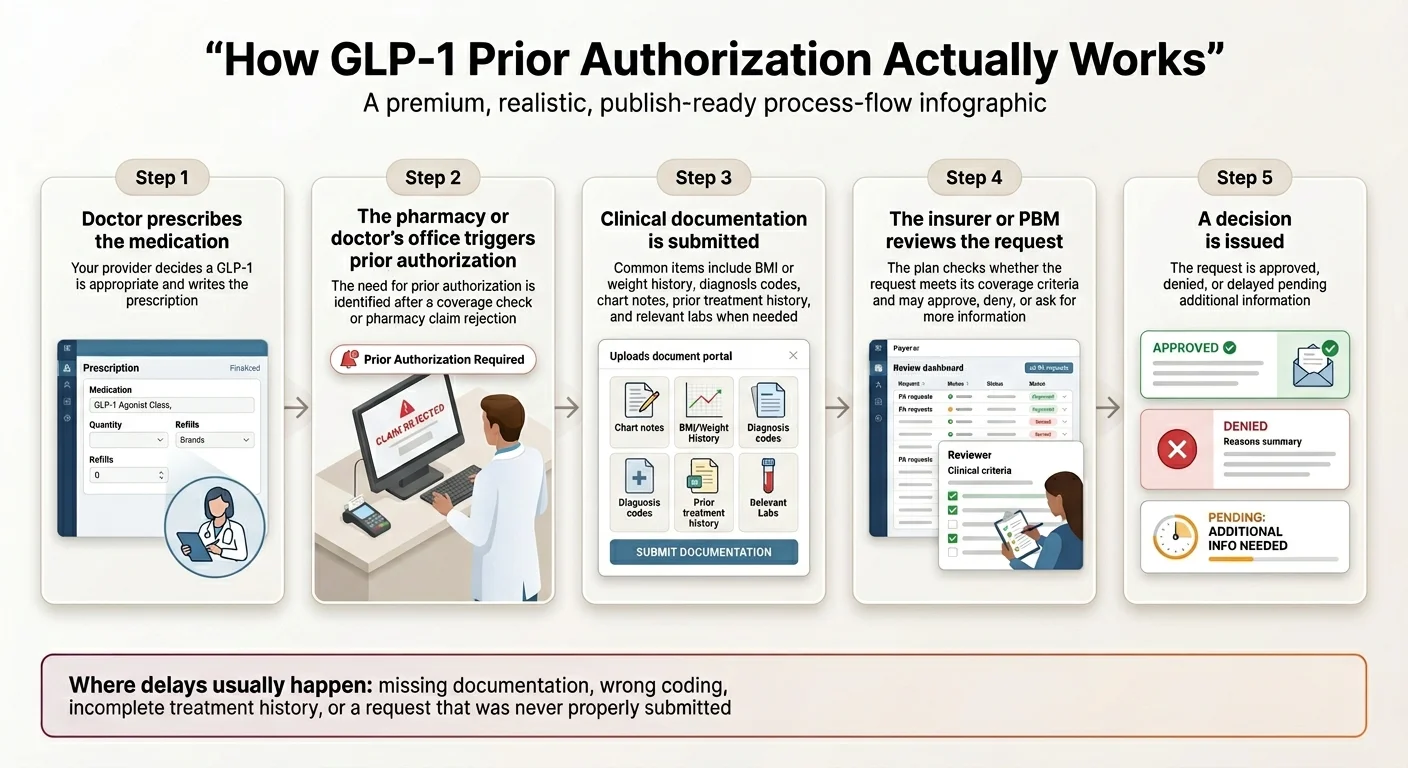

How the GLP-1 Prior Authorization Process Actually Works

If you've never been through a prior authorization, the process can feel like a black box. Here's what happens step by step — so you know where things break and where you can step in.

Your doctor prescribes a GLP-1

They determine a GLP-1 medication is right for your condition — weight management, Type 2 diabetes, cardiovascular risk reduction, or another indication.

The pharmacy or doctor's office triggers the PA

When the prescription hits the pharmacy, the system checks your insurance. If PA is required, the claim is flagged. Either the pharmacy notifies your doctor's office, or the doctor's office submits the PA proactively. This handoff is where requests sometimes fall into a gap — the pharmacy assumes the doctor knows, the doctor assumes the pharmacy is handling it, and nobody has actually submitted anything. If you're past day 3 and haven't heard anything, check this first.

Your doctor submits clinical documentation

BMI, diagnosis codes, chart notes, treatment history — all compiled and sent to your insurer or PBM. This can happen electronically (ePA through platforms like CoverMyMeds), by fax, or through an insurer portal. Electronic submissions are dramatically faster.

The insurer reviews

Their utilization management team checks your submission against plan-specific criteria. Straightforward cases may be automated. Complex cases — off-label use, borderline BMI, incomplete step therapy — get flagged for manual review. That's where multi-week timelines come from.

Decision is issued

The insurer approves, denies, or requests additional information. If approved, your pharmacy can fill your prescription. If denied, you receive a denial letter with the specific reason and have the right to appeal.

Where things go wrong most often:

- 1. The handoff (Step 2): Nobody submits the PA because each party thinks the other is handling it.

- 2. The documentation (Step 3): The submission is missing a required element and gets sent back.

- 3. The indication mismatch (Step 4): The drug was submitted for weight loss but the plan only covers it for diabetes (or vice versa).

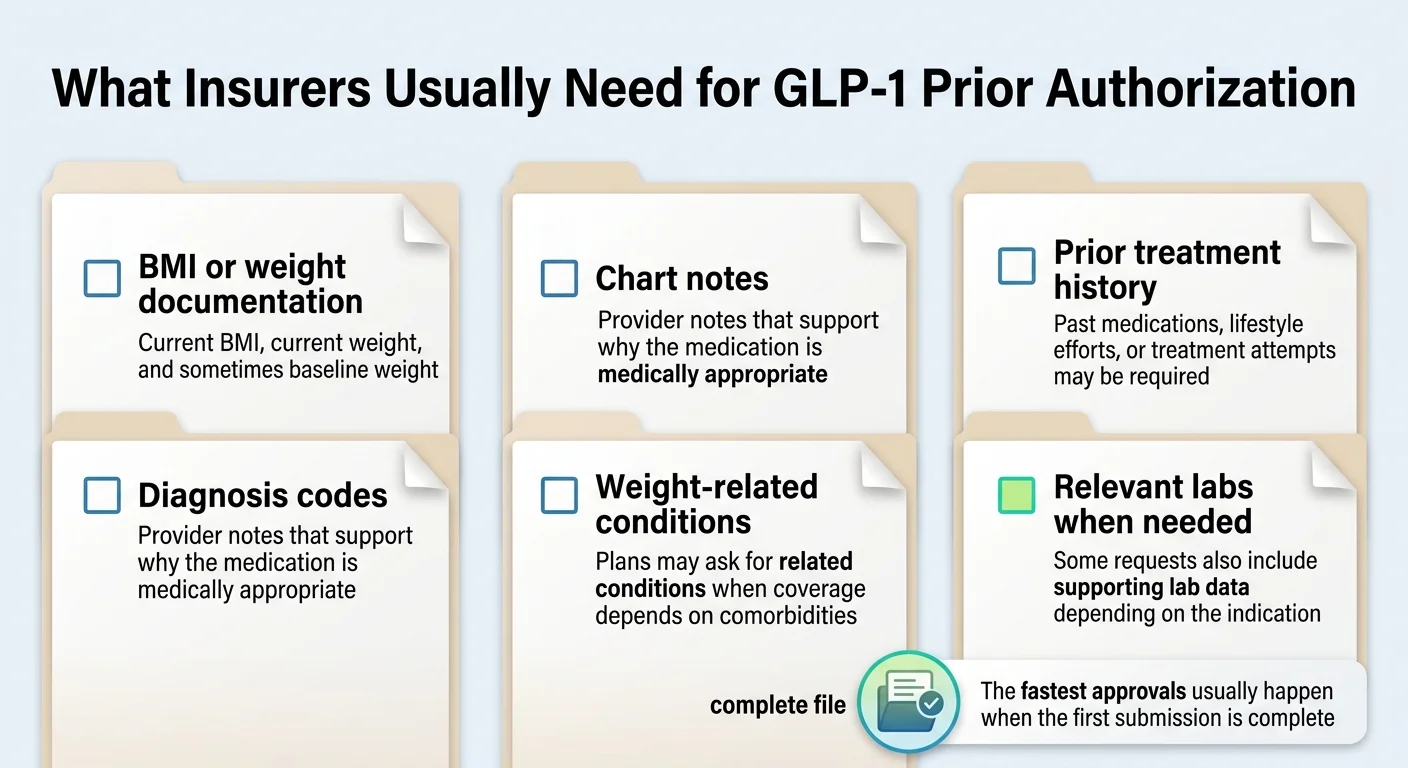

What Insurers Usually Need for GLP-1 Prior Authorization

The fastest approvals happen when the first submission is complete. Here's what most plans need:

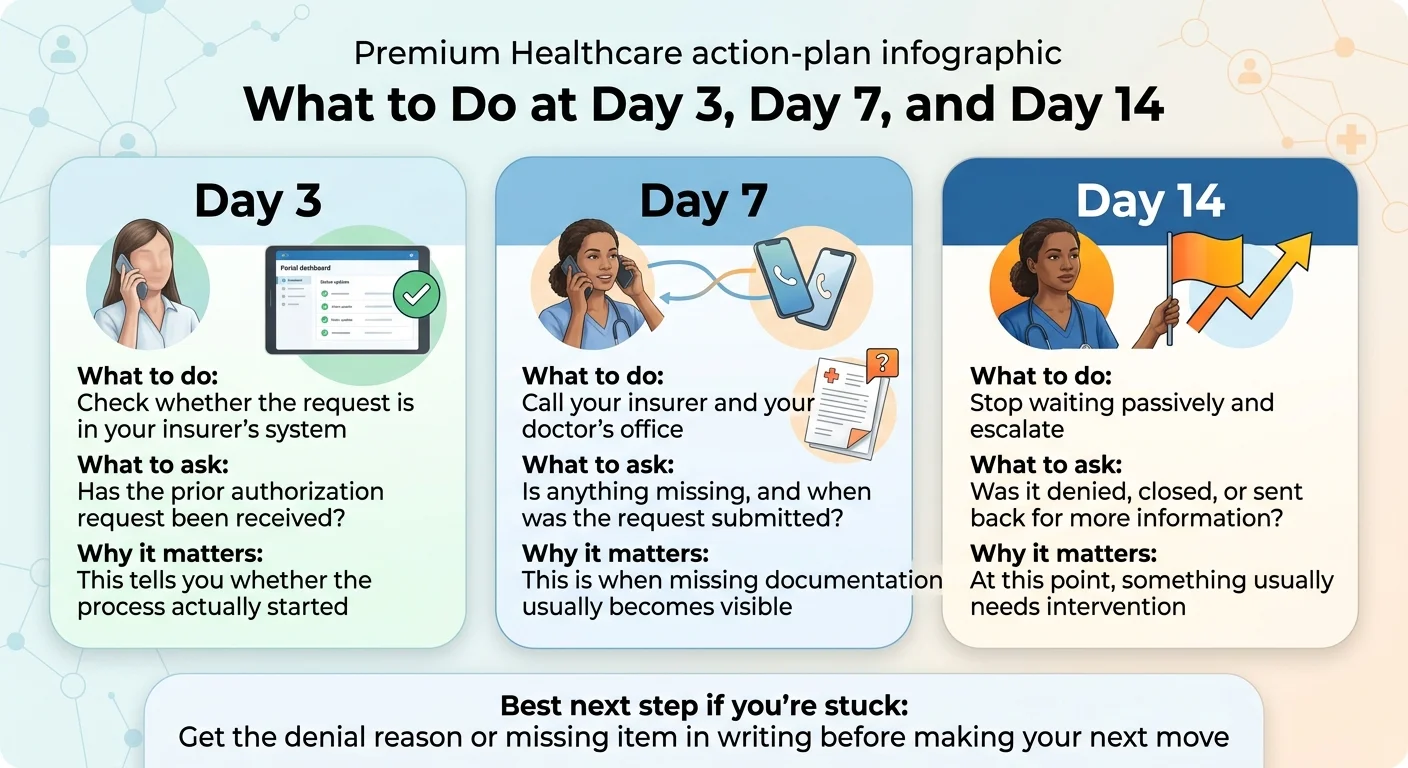

What Should You Do at Day 3, Day 7, and Day 14?

The right action depends entirely on how long you've been waiting. Here's your exact playbook.

If It's Been 0–3 Days

Do: Wait. This is within the normal window for nearly every plan.

Also do: Log into your insurer's member portal and confirm a PA request appears for your medication. Some insurers update status in real time.

If It's Been 4–7 Days

Now it's time to check. Make two calls:

Call your insurer (number on the back of your card)

- 1."Do you have a prior authorization request on file for [drug name]?"

- 2."What date did you receive it?"

- 3."Is it under standard or expedited review?"

- 4."Is anything missing or pending from your end?"

- 5."When should I expect a decision?"

Call your doctor's office

- 1."Was the PA submitted electronically, by fax, or through a portal?"

- 2."What date was it sent?"

- 3."Do you have a confirmation number or fax receipt?"

- 4."Has the insurer contacted you for additional information?"

Write down the reference number, representative's name, and date/time of your call. If your doctor says it was sent and your insurer says they never received it — that's your answer. Ask the office to resubmit and confirm receipt.

If It's Been 8–14 Days

Something is likely incomplete or in manual review. Don't accept "still processing" as a final answer. Get specific:

- Ask your insurer: "What specific document, code, or form is needed to complete this review?"

- Ask your doctor's office to send whatever is missing the same day.

- Confirm the drug was submitted under the correct indication — a Wegovy request coded as a diabetes medication can trigger a denial or extended review.

If It's Been 14+ Days — Escalate

- Ask your insurer whether the request was denied, closed as incomplete, or still in active review.

- If denied, request the denial letter in writing — you need the specific reason.

- Ask whether a peer-to-peer review is available (a direct call between your doctor and the insurer's medical director).

- If your doctor's office has been unresponsive, call them and make clear that you need the PA resolved this week.

At this point you have a decision. If the delay is fixable — missing documentation, a coding error, an appeal likely to succeed — keep working the insurance path. But if your plan excludes weight-loss medications entirely, or you've been in an administrative loop for weeks with no resolution, you may want to start treatment while insurance sorts itself out.

Start treatment now — no PA required

Embody is a cash-pay telehealth GLP-1 program with no prior authorization and no insurance required (HSA/FSA accepted). It offers weekly semaglutide or tirzepatide injections plus a needle-free GLP-1 gum option, from $99 for the first month of semaglutide injection (then $299/mo ongoing). If a licensed provider approves treatment, medication ships to your door. Embody's shipped options are compounded GLP-1 medications, not FDA-approved finished drugs.

Check Embody Eligibility

How to Check Your PA Status Without Getting Bounced Around

The key is to confirm three separate things: whether the doctor submitted it, whether the insurer received it, and whether the pharmacy rejection is truly a PA rejection. Many "waiting" stories turn out to be a request that was never sent, never received, or never formally started.

Call script: Your insurer

- 1."I'm calling to check the status of a prior authorization for [drug name]. My member ID is [number]. Can you confirm whether you have a PA request on file, what date it was received, and whether there are any outstanding items needed to complete the review?"

Call script: Your doctor's office

- 1."I'm checking on the prior authorization submitted for [drug name]. Can you confirm it was sent, the submission date, and whether the insurer has contacted you for additional information?"

Call script: Your pharmacy

- 1."My prescription for [drug name] was rejected at the pharmacy. Can you tell me whether the rejection was due to a prior authorization requirement, a formulary issue, or something else? Was a PA initiated from your end?"

Before you hang up, confirm:

- PA reference or tracking number

- Date the request was received by the insurer

- Standard or expedited review status

- Any specific missing items

- Estimated decision date

- Representative's name

- If denied: the denial reason and instructions for obtaining the written denial letter

Why Do Some GLP-1 Prior Authorizations Get Approved in Hours While Others Take Weeks?

The biggest difference isn't the drug. It's the workflow. Electronic prior authorization with complete documentation can return a decision in minutes. Missing codes, blank fields, or incomplete chart notes can stall the same request for weeks.

What makes a PA go fast

- ✓ Electronic submission (ePA) instead of phone or fax

- ✓ Complete documentation on first submission

- ✓ Drug and indication match formulary criteria cleanly

- ✓ Diabetes diagnosis already on file (for Ozempic/Mounjaro)

What makes a PA drag

- ✗ Fax or phone submissions

- ✗ Missing BMI, codes, or chart notes

- ✗ Off-label use or manual review triggered

- ✗ PA that was never actually submitted

| Delay cause | What you'll hear | Who fixes it | Fastest fix |

|---|---|---|---|

| Missing BMI or baseline weight | "We need additional clinical information" | Doctor's office | Resend with documented BMI same day |

| Wrong or missing ICD-10 code | "The diagnosis doesn't match criteria" | Doctor's office | Correct the code and resubmit |

| Incomplete chart notes | "We need supporting documentation" | Doctor's office | Upload notes with PA reference number |

| No prior treatment history documented | "Step therapy not documented" | Doctor's office | Add records of previous weight-loss attempts |

| PA never actually submitted | "We don't have a request on file" | Doctor's office or pharmacy | Confirm submission method and resend |

| Pharmacy triggered coverage check, not a PA | "That was a benefits check, not a prior authorization" | Pharmacy + doctor's office | Clarify and formally initiate PA |

| Plan exclusion | "This medication class is excluded" | Nobody — the plan doesn't cover it | Explore formulary exception, appeal, or alternatives |

Does the Timeline Differ by Drug — Wegovy vs. Ozempic vs. Zepbound vs. Mounjaro?

There's no reliable universal timeline that differs by drug. What changes is the indication and the criteria — and that can significantly affect how smoothly your PA goes.

Wegovy (semaglutide)

- FDA-approved indications

- Chronic weight management in qualifying adults and adolescents; reduction of major adverse cardiovascular events in adults with established CVD and obesity/overweight; treatment of MASH with moderate-to-advanced liver fibrosis

- PA criteria focus

- BMI thresholds, prior weight-management history, comorbidity documentation

- What helps

- If you have documented cardiovascular disease, the CV indication may open an easier approval pathway — even on plans that restrict weight-loss drugs

- Renewal note

- One UHC commercial criteria document shows an initial authorization period of 5 months, with reauthorization requiring weight-loss evidence from baseline

Ozempic (semaglutide)

- FDA-approved indications

- Type 2 diabetes; cardiovascular risk reduction in adults with Type 2 diabetes and established cardiovascular disease

- PA criteria focus

- Diabetes diagnosis, A1C, prior diabetes medication history

- What helps

- Some plans auto-approve when a T2D diagnosis is already on file — potentially no formal PA needed

- Watch out

- If your doctor prescribes Ozempic off-label for weight loss without a diabetes diagnosis, expect a more complex PA process

Mounjaro (tirzepatide)

- FDA-approved indications

- Type 2 diabetes

- PA criteria focus

- Diabetes diagnosis and treatment history

- What helps

- Watch out

- If the PA codes Mounjaro as weight management, the criteria won't match — even though many patients use it with weight loss in mind

Zepbound (tirzepatide)

- FDA-approved indications

- Chronic weight management; moderate-to-severe obstructive sleep apnea in adults with obesity

- PA criteria focus

- BMI thresholds, comorbidity documentation, potentially sleep study results for OSA

- What helps

- If you have diagnosed sleep apnea, the OSA indication may open a different coverage pathway

- Renewal note

- One UHC criteria document shows an initial authorization period of 6 months for Zepbound

The takeaway: the drug matters less than the indication and the completeness of your documentation. A clean submission with the right diagnosis codes and supporting evidence can move quickly regardless of which GLP-1 you're prescribed.

Do Dose Increases or Renewals Need a New Prior Authorization?

This depends on your specific plan, and it catches people off guard. GLP-1 medications follow a dose-escalation schedule, and some plans require separate authorization at certain dose thresholds or when the original approval period expires.

Dose Increases

- • Some plans review dose changes separately; others approve a full titration schedule upfront.

- • When required, dose-increase authorization needs less documentation — usually a provider statement confirming adherence.

- • Tip: Submit dose-increase requests up to 30 days before you need the next dose to avoid treatment gaps.

Renewals

- • Proof of continued clinical response — many plans require at least 5% weight loss from baseline.

- • Updated provider notes documenting adherence and tolerability.

- • Continued lifestyle modification documentation.

- • Updated labs if applicable.

The Renewal Trap — Don't Let This Happen to You

A common and completely preventable problem: your medical record has your current weight but not your baseline weight from when you started the medication. Insurers compare renewal weight against your original starting weight. If that baseline isn't documented, the renewal can fail even if you've lost significant weight.

Ask your doctor to document your baseline weight and BMI at the start of treatment and keep it in your chart permanently. It takes 30 seconds and prevents the most frustrating kind of renewal denial.

What Changes If You're on Medicare, Medicaid, or an Employer Plan?

The same drug can follow a completely different approval path depending on your plan type.

Medicare in 2026

Current: Medicare Part D covers GLP-1s for Type 2 diabetes. Wegovy is covered for cardiovascular risk reduction in patients with documented heart disease and obesity/overweight. Medicare does NOT cover GLP-1s prescribed solely for weight loss.

Starting July 1, 2026: The Medicare GLP-1 Bridge demonstration will allow eligible beneficiaries to access GLP-1 obesity medications, running through December 31, 2026. It still requires a provider-submitted prior authorization.

Important: If your use is already covered through regular Part D — Zepbound for obstructive sleep apnea or Wegovy for cardiovascular risk reduction — that goes through the regular Part D pathway, not the Bridge.

Employer / Commercial Plans

• Approval depends on your employer's formulary and utilization management rules.

• A 2025 Health Affairs/KFF survey found that 43% of large employers (5,000+ employees) now cover GLP-1s for weight loss, up from 28% in 2024.

• If your plan categorically excludes weight-loss medications, a clean PA won't overcome that.

• Check during open enrollment whether alternative plan options cover weight-loss medications.

Medicaid

• As of January 2026, 13 state Medicaid fee-for-service programs covered GLP-1 drugs for obesity.

• When covered, PA timelines are typically 7–14 days.

• If your state doesn't cover GLP-1s for weight loss through Medicaid, your options are limited to diabetes or CV indications, or alternatives outside insurance.

What If You Don't Want to Wait?

Going outside insurance means paying out of pocket — typically $149–$349/month depending on the medication and provider. That's real money. If your insurance covers GLP-1s and you can get a $30–$75 copay through PA, keep working that path.

But if your plan excludes weight-loss medications — and the majority of ACA marketplace plans and current Medicare don't cover GLP-1s for weight loss — the PA process was never going to end in an approval. Many patients in that situation choose to start treatment through a cash-pay provider while their insurance sorts itself out.

Two Paths Worth Knowing About

FDA-approved brand-name — no PA

Novo Nordisk offers oral Wegovy starting at $149/month for the 1.5mg starting dose through NovoCare for self-pay patients. FDA-approved product — no insurance required, no PA. Some telehealth programs also offer brand-name GLP-1s with insurance concierge support.

Visit NovoCare →Compounded GLP-1 — fastest start

Embody prescribes compounded GLP-1 medications with no prior authorization and no insurance required (HSA/FSA accepted). Complete a fast online intake; if a licensed provider approves treatment, medication ships to your door — often within the same week. Choose weekly semaglutide or tirzepatide injections or a needle-free GLP-1 gum, starting at $99 for the first month of semaglutide injection (then $299/mo ongoing).

Note: Compounded GLP-1 drugs are not FDA-approved and are not the same as brand-name products. They are legal when prescribed by a licensed provider and dispensed by a licensed pharmacy.

Check Embody EligibilityDoes This Sound Like Your Situation?

Keep working insurance if:

- ✓ Your plan covers weight-loss or diabetes meds

- ✓ Your delay looks fixable

- ✓ You haven't been denied yet

- ✓ Your copay will be lower than cash-pay

Consider starting now if:

- → Your plan excludes weight-loss coverage

- → You've been denied and appeal adds weeks

- → You've been waiting 14+ days with no resolution

- → You're on Medicare pre-Bridge

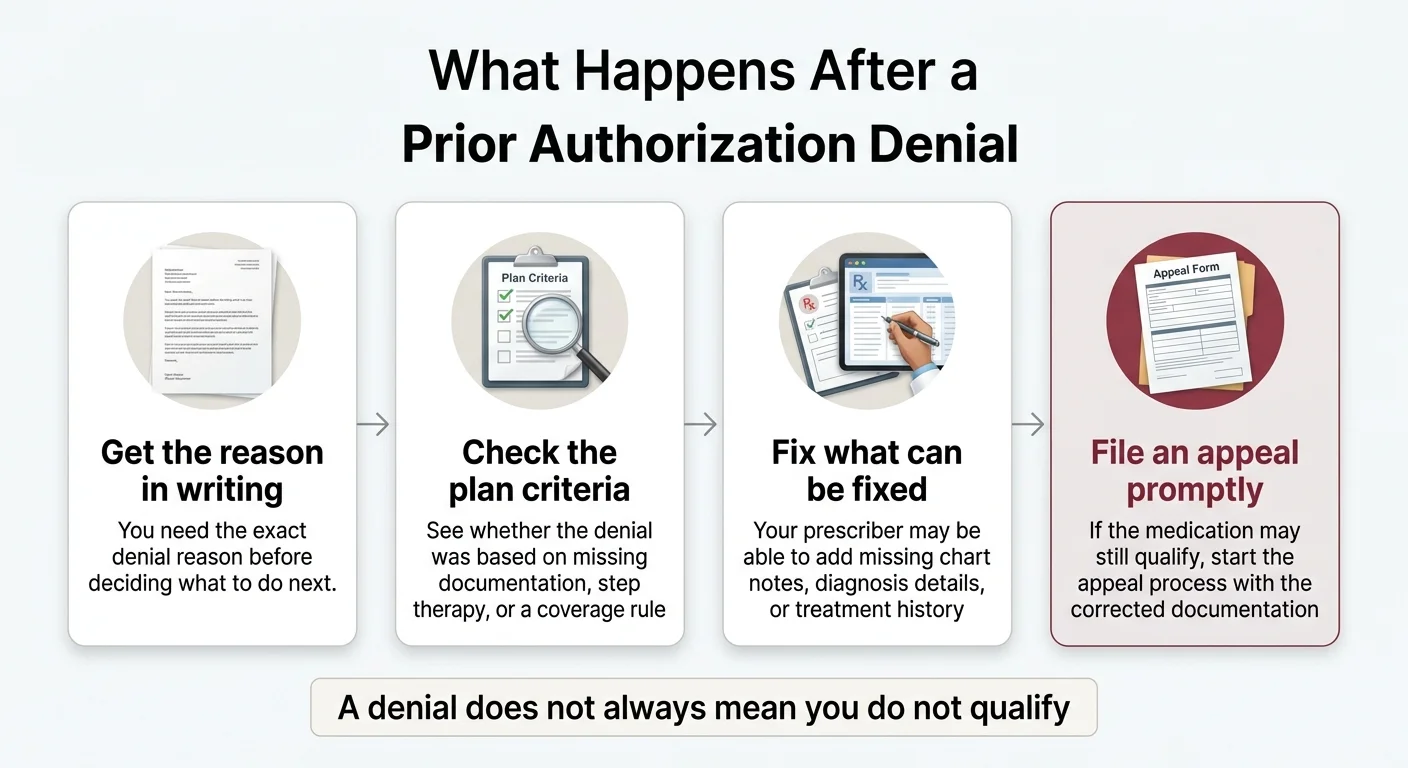

What Happens After a Prior Authorization Denial?

A denial does not always mean you don't qualify. In Medicare Advantage, 80.7% of appealed PA denials are partially or fully overturned.

Get the reason in writing

You need the exact denial reason before deciding what to do next.

Check the plan criteria

See whether the denial was based on missing documentation, step therapy, or a coverage rule.

Fix what can be fixed

Your prescriber may be able to add missing chart notes, diagnosis details, or treatment history.

File an appeal promptly

If the medication may still qualify, start the appeal process with the corrected documentation.

Need help with a denial or appeal?

See our detailed step-by-step guide on appealing a Wegovy or Zepbound denial — including word-for-word scripts, denial type decoder, and real case studies.

How to Appeal a Wegovy or Zepbound Denial →How We Verified This Page

We don't publish timelines based on what "sounds right." Here's what we checked:

- •Official payer turnaround commitments from Blue Shield of California, Express Scripts, UnitedHealthcare, and Aetna published PA guidelines

- •PBM criteria documents from CVS Caremark (Wegovy criteria) and OptumRx

- •Manufacturer PA guides from Novo Nordisk (Wegovy) and Eli Lilly (Mounjaro)

- •Patient-reported timing from Reddit threads (r/Zepbound, r/Ozempic) — used for real-world context, not medical guidance

- •KFF Medicare Advantage PA data on denial rates and appeal outcomes

- •AMA physician survey data on PA processing burdens

- •Surescripts ePA research on electronic PA time savings

- •CMS Medicare GLP-1 Bridge documentation

Every claim is linked to a verifiable source or identified as a range based on patient reports. We review and update this page regularly.

How We Make Money: This page includes links to providers we may earn a commission from if you sign up. This doesn't affect our editorial process or what we tell you about insurance timelines. We recommend providers we've vetted and would suggest to people we know.

Not Medical or Insurance Advice: This page is for informational purposes. We are not doctors, pharmacists, or insurance agents. Consult your prescribing healthcare provider and your insurance company for decisions about your specific treatment and coverage.

Frequently Asked Questions

Ready to explore cash-pay options?

Whether you're still waiting on insurance or ready to start now — compare GLP-1 programs with no PA requirement, no insurance needed, and same-week shipping.