GLP-1 Providers That Accept HRA: What Actually Works in 2026

Weight Loss Provider Guide is an independent comparison resource for GLP-1 telehealth providers. Some links on this page are affiliate links — if you enroll through them, we may earn a commission at no extra cost to you. This does not affect our editorial process. For informational purposes only — not medical advice.

Short answer: Most GLP-1 providers don't 'accept HRA' the way they accept HSA/FSA — but the right ones give you paperwork your HRA admin will actually reimburse.

An HRA (Health Reimbursement Arrangement) is an employer-funded account that usually reimburses you after you pay, rather than processing a debit card at checkout. Some specialty GLP-1 HRAs (Benepass, WEX, Sentinel) do issue cards — but the reimbursement model remains the common case.

The real question isn’t which provider accepts HRA. It’s which provider gives you a clean enough receipt and Letter of Medical Necessity that your administrator actually reimburses you — instead of sending a denial letter two weeks later.

As of April 16, 2026, here’s the bottom line from our review of every major online GLP-1 program:

- Clearest exact-match: Sesame is the only provider in our comparison that publicly names HRA as an accepted payment source. Subscription is $59/month on the annual plan or $99/month month-to-month, with medication billed separately.

- Cleanest reimbursement-first option: Hers and Hims publish the clearest pay-first-and-submit workflow — $39 first month, then $149/month, with downloadable receipts inside your account.

- FDA-approved brand-name path: Ro is the right choice if your HRA plan restricts reimbursement to FDA-approved medication — get started for $39, then as low as $74/month with an annual plan paid upfront (or $149/month ongoing), with access to Zepbound® (tirzepatide) and Foundayo™ (orforglipron, FDA-approved April 1, 2026).

The one condition that changes everything

Not sure which path fits your HRA?

Take our free 60-second matching quiz — we’ll ask about your HRA setup and match you to the program with the cleanest reimbursement path for your situation.

What we actually verified

We reviewed the following sources directly to build this page:

- IRS Publication 502 (medical expenses) and Publication 969 (HSAs, HRAs, and other tax-favored plans)

- Public HRA / HSA / FSA payment language on each provider’s own site or help center

- Provider pricing pages, billing terms, and cancellation policies

- FDA approval announcement for Foundayo (April 1, 2026)

- FDA guidance on compounded GLP-1s and national supply

- Healthcare.gov HRA glossary and ICHRA guidance

- Employer-benefits guidance from Ogletree Deakins (November 2025), NFP, and Benepass

- Material FDA warning letters affecting listed providers

- Representative HRA plan notices published in 2026 (e.g., VEHI’s January 29, 2026 HRA/GLP-1 notice)

We did not independently test checkout for every provider. Where we couldn’t confirm a claim from a public source, we flag it as “not publicly documented” or “verify at checkout.”

HRA Compatibility Matrix for online GLP-1 providers

Last verified: . The column that matters most isn’t price — it’s whether the provider gives you the paperwork your HRA administrator needs to pay you back.

| Provider | Public HRA wording? | Best payment path | Receipt / LMN support | Starting price | Best for |

|---|---|---|---|---|---|

| Sesame | Yes — explicit | Pay on annual or month-to-month; reimburse via HRA or card at checkout | Itemized receipts available; LMN via booked provider (not publicly documented as standard) | $59/mo annual or $99/mo month-to-month (med separate) | Exact HRA-language match; FDA-approved options |

| Hers | Not HRA-specific; reimbursement workflow is explicit | Pay first, submit receipt | Downloadable receipts publicly documented | $39 first month, then $149/mo | HRAs that reimburse after payment |

| Hims | Not HRA-specific; reimbursement workflow is explicit | Pay first, submit receipt | Downloadable receipts publicly documented | $39 first month, then $149/mo | Male-coded mainstream brand trust |

| Ro | Cash-pay receipts support reimbursement; accepts some insurance | Insurance first, HRA for copay; or cash receipt | Detailed receipts post-purchase publicly documented | $39 intro, then $149/mo (as low as $74/mo annual) | FDA-approved Zepbound® + Foundayo™; insurance paths |

| Shed | HSA/FSA card explicit; HRA not named | Card at checkout (HSA/FSA card) or receipt | Detailed receipts + LMN support publicly documented | $199/mo starting | Card-friendly with the strongest paperwork trail |

| Embody | HSA/FSA card explicit; HRA not named | Card at checkout (HSA/FSA card) or receipt | Standard receipts (LMN not publicly documented) | From $99 first month (semaglutide injection) | Lowest first-month price; needle-free GLP-1 gum option |

| MEDVi | HSA/FSA advertised; HRA not named | Reimbursement | Receipts issued (LMN not publicly documented) | $179 first month, $299 refills | Lowest guided entry price (read warnings below) |

| Yucca | No public HRA wording | N/A — documentation gaps | No itemized receipts; no LMN support | ~$146/mo | Not recommended for HRA use |

How to read this table

Editorial conclusion for this exact query: Sesame is the strongest literal match because it’s the only provider on our matrix that publicly names HRA on its payment page. After Sesame, your best path depends on whether your HRA works more like a debit card (Shed, Embody) or a reimbursement account (Hers, Hims, Ro). We’ll help you figure out which one you have in the next few sections.

See current Sesame GLP-1 pricingCan you actually use an HRA for a GLP-1 medication?

Answer capsule

There are three layers working at the same time, and missing any one of them gets you denied:

Layer 1: The IRS rule (federal)

Prescription weight-loss medications are eligible for reimbursement through an FSA, HSA, or HRA when they treat a specific diagnosed condition such as obesity, type 2 diabetes, hypertension, or heart disease (HSA Store eligibility list, aligned with IRS Publication 502). General wellness, cosmetic weight loss, or “looking better for a wedding” doesn’t qualify. The dividing line is whether the medication is treating a diagnosed medical condition.

Layer 2: Your prescription and diagnosis

The telehealth provider needs to document your diagnosis — not just write a prescription. A prescription for “semaglutide for weight management” without a diagnosis code like obesity (ICD-10 E66.9) or overweight with a related condition often gets flagged by an HRA administrator. Better providers capture this in the clinical note by default.

Layer 3: Your employer’s HRA plan design

This is the part most ranking pages skip. Even if the IRS says the medication is qualified, your employer’s HRA plan document can specifically exclude weight-loss medications. A clean real-world example: in January 2026, the Vermont Education Health Initiative (VEHI) published a notice telling members their HRA could not be used for GLP-1 weight-loss medications even though HSA, FSA, and cash-pay still could.

That’s the pattern playing out in real forum threads. One Reddit post titled “Any telehealth providers take HRA funds?” captures the same confusion almost verbatim — people who have the money, want the medication, and can’t figure out whether the employer plan will actually let them use it.

So before you pick a provider, answer these three questions:

- Does your HRA plan document list weight-loss medications as excluded? Check your Summary Plan Description (SPD) or ask your benefits administrator directly. If weight-loss meds are excluded, no provider will solve that — only your employer can.

- Does your plan require a Letter of Medical Necessity for GLP-1 reimbursement? Many do, especially when the prescription is coded as weight management rather than diabetes.

- Is your HRA “integrated” with your group health plan, or is it a standalone or specialty HRA? (We cover the five common structures below — each one changes what it can reimburse.)

If those answers come back clean, you’re in the normal lane: pick a provider that issues clean receipts, submit them, and get reimbursed.

Not sure which HRA structure you have or which path fits?

No spam, no sales calls — just a personalized HRA-friendly provider match.

HRA vs HSA vs FSA for GLP-1s: the real differences that change what you do

Answer capsule

| Feature | HSA | FSA | HRA |

|---|---|---|---|

| Who funds it | You (pre-tax from paycheck) | You (pre-tax from paycheck) | Employer only |

| How you typically pay | Debit card at checkout | Debit card at checkout | Pay out of pocket, submit for reimbursement (some HRAs issue cards) |

| Rolls over year to year | Yes, always | No (limited exceptions) | Depends on plan design |

| Travels with you if you change jobs | Yes | No | No (almost always stays with employer) |

| Need an LMN for weight-loss GLP-1? | Often yes | Often yes | Usually yes |

| Card works at any medical merchant? | Usually yes | Usually yes | Depends on plan — often no |

The key insight

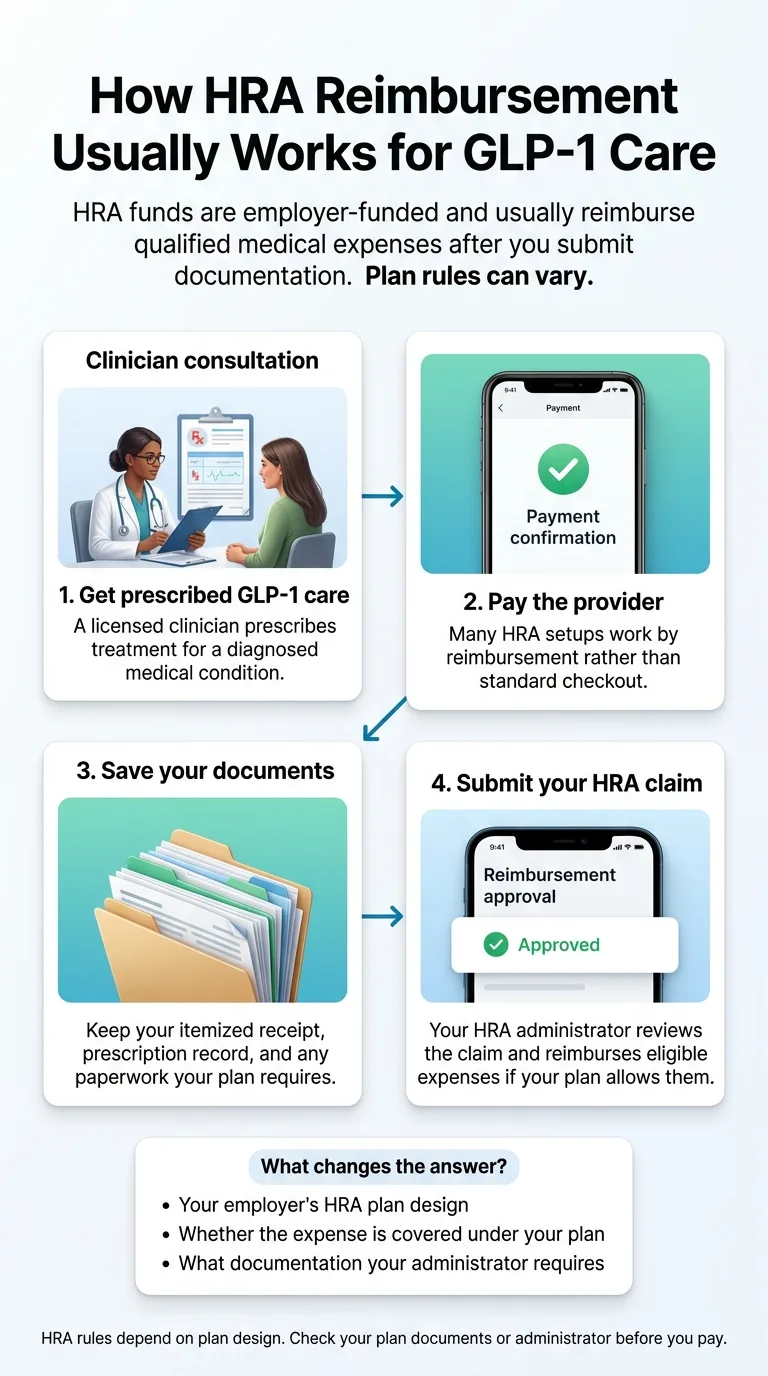

This is why the right workflow for HRA users is almost always:

- Pay the provider with a regular credit or debit card.

- Download an itemized receipt from the provider’s account portal.

- Submit the receipt (with any required documentation) to your HRA administrator.

- Get reimbursed. Timing varies — HealthEquity, for example, publicly states member reimbursements typically process within a few business days once documentation is complete.

If your HRA has a swipable card, lucky you — test it on a smaller purchase first, because card declines at telehealth checkout are common.

If it turns out you actually have an HSA or FSA (not an HRA), read our companion page: GLP-1 Providers That Accept HSA. The mechanics are different.

Which HRA do you actually have? The 5 common structures that change your GLP-1 answer

Answer capsule

Type 1: Integrated HRA (the most common)

If your employer offers group health insurance and the HRA is part of that benefits package, this is almost certainly what you have. An integrated HRA can reimburse virtually any qualified medical expense allowed by the IRS — which includes prescribed GLP-1s. Weight-loss GLP-1s are usually covered unless your plan document specifically excludes them.

Practical implication: your ceiling is whatever the employer funded (often $1,000–$5,000/year), and your biggest risk is a plan-level exclusion. Read your SPD.

Type 2: Excepted Benefit HRA (EBHRA)

The EBHRA is a “standalone” account — your employer can offer it even if you’re not enrolled in their group health plan. The 2026 maximum contribution is $2,200 (Ogletree Deakins, November 2025). EBHRAs can reimburse copays, coinsurance, deductibles, COBRA premiums, and standalone vision/dental premiums — but generally can’t reimburse individual or group health insurance premiums.

Practical implication: $2,200 gets you roughly 11 months of a $199/month compounded semaglutide program, or about 4–5 months of FDA-approved Wegovy® at manufacturer self-pay rates.

Type 3: ICHRA (Individual Coverage HRA)

Your employer doesn’t offer group health insurance; instead they give you money to buy your own Marketplace plan. ICHRA funds can cover both premiums and qualified medical expenses. Per Healthcare.gov, employers can contribute as much or as little as they want to an ICHRA — there is no annual minimum or maximum contribution requirement.

Practical implication: ask HR exactly what’s in your ICHRA, what it covers, and whether weight-loss medications are included.

Type 4: QSEHRA (Qualified Small Employer HRA)

For employers with fewer than 50 full-time employees. QSEHRAs can reimburse qualified medical expenses and individual insurance premiums. Annual contribution caps are set by the IRS and adjust yearly.

Practical implication: smaller ceilings than ICHRA but similar flexibility. If you work at a small business with no group health plan, this is probably what you have.

Type 5: Specialty GLP-1 HRA / Weight Health HRA

This is the newer carve-out category. Vendors like Benepass, WEX, and Sentinel Group now administer HRAs designed specifically for GLP-1 coverage. Employers set a fixed annual budget, restrict reimbursement to specific medications (often brand-name only), and sometimes issue a Visa card that only works for approved merchants.

Practical implication: if your employer launched a “Weight Health HRA” or “GLP-1 HRA” in 2025 or 2026, read the medication list carefully. Many specialty HRAs restrict reimbursement to FDA-approved brand-name drugs like Wegovy®, Zepbound®, and Foundayo™ — meaning a compounded semaglutide program won’t qualify.

One damaging admission, because it matters

Best GLP-1 providers that accept HRA (deep dives)

Answer capsule

#1 — Sesame: the clearest exact-match for “accepts HRA”

Sesame is the only provider on our matrix that explicitly names HRA as an accepted payment source on its own site. That’s the literal answer to the search that brought you here.

Pricing we verified (April 16, 2026):

- Success by Sesame subscription: $59/month on the annual plan, or $99/month month-to-month (medication is billed separately)

- FDA-approved options through Sesame providers include Wegovy®, Zepbound®, Ozempic®, Wegovy® pill, Rybelsus®, and — as of April 1, 2026 — Foundayo™ (orforglipron)

- Self-pay medication pricing varies by provider; Wegovy® injections through Sesame partnership programs have been listed starting at $199/month for the first two months, then $349/month

Why Sesame wins this exact query:

- It publicly names HRA alongside HSA and FSA as accepted payment sources

- It carries FDA-approved GLP-1s (which matters if your employer’s HRA restricts to brand-name)

- You pick the clinician, which often means more flexibility on documentation requests

Damaging admission, followed by the pivot

Real testimonial (service and convenience context, not a medical outcome claim): Sesame’s review page features a patient named Barbara who wrote about saving money compared to a clinic and finding her medication affordable and convenient (source: Sesame site). Customer experiences are individual and not guarantees of reimbursement or treatment outcome.

Best for:

- Anyone whose HRA admin wants a clean itemized receipt

- Anyone whose plan restricts to FDA-approved medications

- Anyone who prefers to pick their own clinician

Skip if:

- Your only goal is the cheapest possible monthly price

- Your HRA plan has excluded weight-loss medications entirely

#2 — Hers and Hims: best for reimbursement-first HRAs

If your HRA works by reimbursing you after you pay (which is most HRAs), Hers and Hims are the cleanest match. Both platforms publish a plain-English reimbursement workflow: pay with any card, download your receipt from the orders tab, and submit it through your HRA administrator.

Pricing we verified:

- Membership: $39 for the first month, then $149/month

- Weight loss medication options include oral kits starting around $69/month and compounded GLP-1 injections starting around $199/month

- Both brands state explicitly on their HSA/FSA pages that the full GLP-1 medication kit is reimbursable via HSA or FSA — the same submission mechanics apply to HRA

- State availability note: GLP-1 weight-loss medications are not yet available in all 50 states. Check availability during intake before paying

Why they work well for HRA users:

- Receipt download is in your account, one click, no waiting

- Clear separation between membership fee and medication cost (HRA admins like clean itemization)

- The “pay first, submit later” workflow is already the Hers/Hims default

Hers vs Hims: Same platform under the hood, different audience positioning. Hers is positioned for women, Hims for men. The payment mechanics, receipt workflow, and HRA compatibility are identical.

One Reddit post titled “Hers is reimbursable through your HRA” describes exactly this workflow — a patient submitted the Hers receipt to their HRA and got reimbursed. Individual plans vary, but the workflow is reliable.

#3 — Ro: best for FDA-approved brand-name GLP-1s

Ro is the right pick when your HRA plan restricts reimbursement to FDA-approved medications — which is increasingly common in the newer specialty GLP-1 HRAs. Ro carries Zepbound® (tirzepatide) and Foundayo™ (orforglipron, FDA-approved April 1, 2026), and publicly documents that patients can submit detailed post-purchase receipts for reimbursement.

Pricing we verified (confirm at checkout):

- Get started for $39, then as low as $74/month with annual plan paid upfront (or $149/month ongoing)

- Membership includes provider oversight, prescription management, insurance navigation, and coaching

- Medication is billed separately

- Ro submits insurance prior authorizations on your behalf, which can stack with HRA reimbursement for copays

Why Ro works for HRA users:

- FDA-approved medication is a safe fit for specialty GLP-1 HRAs

- Insurance concierge means you can stack insurance + HRA (insurance first, HRA covers the copay)

- Clean post-purchase receipts that HRA administrators typically accept

A note on Ro's payment acceptance

#4 — Shed: best paperwork trail among card-friendly providers

Shed is a strong next-tier pick for anyone whose HRA behaves more like an HSA or FSA — meaning it gives you a card you can swipe at qualified medical merchants. Shed explicitly accepts HSA/FSA cards for prescription purchases, issues detailed receipts in the portal, and tells patients on its help page to reach out if a Letter of Medical Necessity or additional documentation is required.

Pricing we verified:

- Compounded semaglutide: starting at $199/month

- Maintenance pricing: published at $249/month

- Oral and injection formats available

Why Shed stands out:

- Only provider in the compounded tier that publicly documents LMN/additional-documentation support

- Clean receipt trail in the portal

- Month-to-month commitment structure (with the standard 2-month minimum)

Honest limitation

#5 — Embody: best low starting price and needle-free options

Embody is a cash-pay telehealth GLP-1 program for people who want a low starting price, fast online intake, weekly semaglutide or tirzepatide injections, or a needle-free GLP-1 gum option.

Pricing we verified:

- From $99 first month (semaglutide injection), then $299/mo ongoing

- Tirzepatide injection: $149 first month, then $399/mo ongoing

- Needle-free GLP-1 gum options available ($149+ first month)

- HSA/FSA cards accepted; no insurance required

Why Embody fits broad HRA scenarios:

- Low entry cost for initial treatment phase

- Broad U.S. availability (confirmed during intake)

- Itemized receipt workflow suitable for reimbursement

Compounded medication note

#6 — MEDVi: lowest guided entry price, with a material caveat you should read

MEDVi offers one of the lowest first-month entry prices in the compounded GLP-1 market: $179 first month, with refills at $299 per month. HSA/FSA eligibility is advertised, and receipts are issued in the patient portal.

The caveat we have to disclose

Who MEDVi still fits:

- Readers who value the lowest possible first-month entry price and understand the regulatory context

Who should skip MEDVi:

- Specialty GLP-1 HRA holders whose plans require FDA-approved medication

- HRA admins strict about regulatory compliance of the dispensing pharmacy

- Anyone uncomfortable with the FDA warning context — route to Sesame or Ro

Not recommended for HRA use: Yucca Health

Yucca Health is a reasonable low-friction cash-pay option for some searchers. For HRA users, it isn’t. Yucca’s FAQ page states that the company does not provide itemized receipts or Letters of Medical Necessity — which are the two documents HRA administrators most often request.

If reimbursement paperwork matters to you (and if you’re on this page, it does), Yucca will make your HRA claim harder, not easier. Route to Shed or Embody for card-friendly self-pay, or to Sesame for the exact-match HRA path.

Compare documentation-friendly GLP-1 providersThe HRA reimbursement packet (step-by-step)

Answer capsule

What to assemble

1. Itemized provider receipt — should show medication name, dosage, quantity, date, amount paid, and the provider business name. Most telehealth providers (Sesame, Hers, Hims, Ro, Shed, Embody, MEDVi) issue this automatically in the patient portal.

2. Prescription record — a screenshot of the prescription label, a pharmacy dispense record, or (in telehealth) the prescription document in your patient portal.

3. Letter of Medical Necessity (LMN) — when required. The LMN is a short signed statement from your prescriber that includes your diagnosis (for example, obesity ICD-10 E66.9), confirms the medication is medically necessary, and states the treatment is not cosmetic.

4. Diagnosis documentation — often included in the LMN itself. Some administrators also want the visit note or a separate diagnosis letter.

5. Proof of payment — credit card statement, bank screenshot, or the provider’s stamped “paid” confirmation on the receipt.

6. HRA claim form — each HRA administrator has their own form (HealthEquity, Lively, WEX, Alegeus, Sentinel Group, Benepass, and others). Usually submitted through their portal or mobile app.

The workflow

- Pay the provider with any card. Screenshot your confirmation.

- Download the itemized receipt from the patient portal the moment the order confirms. Save as PDF.

- Request an LMN from the prescriber through the patient portal if your HRA requires one — turnaround depends on the provider.

- Collect proof of payment (statement screenshot).

- Assemble the packet into a single folder or PDF.

- Submit through your HRA administrator’s portal. Keep a copy for your records.

- Wait for reimbursement. HealthEquity, for example, publishes typical processing windows of a few business days once documentation is complete; mailed reimbursements take longer.

If your card declines at checkout

When you need a Letter of Medical Necessity (and how to get one)

Answer capsule

What an LMN contains

- Your full name and date of birth

- The prescribing clinician’s full name, credentials, and NPI

- Your specific diagnosis (for example, obesity — ICD-10 E66.9)

- The prescribed medication name and dosage

- A plain statement that the treatment is medically necessary for the diagnosed condition

- An explicit statement that the treatment is not cosmetic or for general wellness

- The clinician’s signature and date

- A validity period (most administrators accept 12 months)

How to ask your telehealth provider for an LMN

Message through the patient portal. A simple script works:

“Hi — I’m going to submit a reimbursement claim to my HRA administrator for my GLP-1 prescription. Could you send me a Letter of Medical Necessity that includes my diagnosis, the medication, and a statement that this treatment is medically necessary (not cosmetic)? My HRA administrator requires this documentation. Thank you.”

Provider-by-provider LMN reality check

- Shed publicly documents LMN and additional-documentation support on its help page

- Sesame LMNs are typically handled through the booked provider (responsiveness depends on who you book)

- Hers, Hims, Ro support clinician requests through the patient portal, though LMN issuance is not publicly documented as a standard feature

- MEDVi, Embody — LMN policies are not publicly documented; contact support directly

- Yucca Health publicly states it does not provide LMNs — not recommended for HRA use

If your current provider won’t write an LMN — switch. Most reputable telehealth platforms will issue an LMN for a legitimate weight-loss diagnosis. If yours won’t, that’s a signal about their operational quality.

Find a provider that supports LMN requestsCan your HRA still deny a GLP-1 claim even if the medication is IRS-eligible?

Answer capsule

IRS-qualified vs plan-covered

IRS-qualified means the expense meets Section 213(d) of the tax code — it’s a legitimate medical expense eligible for tax-advantaged reimbursement in general.

Plan-covered means your specific HRA plan document allows that expense to be reimbursed from your specific HRA.

These two things are not the same. Your employer decides which IRS-qualified expenses its HRA will actually reimburse. Many employers narrow the list.

The clearest recent example comes from VEHI’s January 29, 2026 HRA notice: covered members learned that GLP-1 weight-loss medications could still be purchased with HSA or FSA funds or cash-pay, but not with HRA dollars — because the underlying health plan excluded weight-loss GLP-1 coverage. The notice also warned that an HRA card might still process at a pharmacy and then trigger a repayment obligation later. That’s the denial pattern you want to prevent.

Three questions to ask your HRA administrator before you buy

- “Does my HRA plan exclude weight-loss medications or GLP-1 receptor agonists?”

- “Does my plan require a Letter of Medical Necessity for GLP-1 reimbursement, or will a prescription and diagnosis suffice?”

- “Are there specific medications, formulations (FDA-approved vs compounded), or vendors that my plan restricts or excludes?”

Write down the answers. Screenshot the email response if you get one.

What to check in your Summary Plan Description (SPD)

- The words “weight loss,” “weight management,” “obesity,” or “GLP-1”

- Any “excluded drugs” or “non-covered medications” list

- The list of qualified medical expenses the plan will reimburse

- Any requirement for prior authorization or medical necessity documentation

- The claim submission window (some plans require claims within 90 days)

If your claim is denied

Most HRA administrators allow an internal appeal under the standard benefit-claim procedure rules overseen by the U.S. Department of Labor. Common fixes: add the LMN if you didn’t include it, re-submit with stronger diagnosis documentation, or ask your prescriber to add a specific ICD-10 code. If the denial is based on a plan exclusion, paperwork won’t fix it — escalate to HR or accept the exclusion.

Want help checking HRA compatibility before you enroll?

Two minutes, no spam — just your match.

FDA-approved vs compounded GLP-1 for HRA users

Answer capsule

The core distinction

- FDA-approved GLP-1s are manufactured to federal standards, carry full prescribing information, and are sold through licensed retail pharmacies. Examples: Wegovy® and Ozempic® (semaglutide, Novo Nordisk), Zepbound® and Mounjaro® (tirzepatide, Eli Lilly), Foundayo™ (orforglipron, Eli Lilly — approved April 1, 2026 as the first small-molecule oral GLP-1 receptor agonist for chronic weight management).

- Compounded GLP-1s are prepared by state-licensed compounding pharmacies, often at significantly lower prices. Compounded products are not FDA-approved and are not evaluated by the FDA for safety, effectiveness, or quality. Per FDA’s April 1, 2026 compounder policy statement, both the tirzepatide injection shortage and the semaglutide injection shortage (resolved February 21, 2025) are now resolved, which has shifted the regulatory context for routine compounded GLP-1 production.

Why this matters for HRA users

- Integrated HRAs usually don’t care whether the medication is FDA-approved or compounded — they want a valid prescription, receipt, and (usually) an LMN.

- Specialty GLP-1 HRAs frequently restrict reimbursement to FDA-approved medications only.

- EBHRAs and ICHRAs vary by plan design — always check.

The practical decision

- If your HRA plan allows either type: compounded usually wins on price.

- If your HRA plan requires FDA-approved: Ro for Zepbound® or Foundayo™, or Sesame for the full FDA-approved menu.

- If you’re unsure: err toward FDA-approved. A denied $299/month claim is worse than a reimbursed $499/month claim.

Compliance reminders for our readers

- Compounded semaglutide is not the same product as Wegovy® or Ozempic®.

- Compounded tirzepatide is not the same product as Zepbound® or Mounjaro®.

- “Compounded” is not a generic version of an FDA-approved drug.

- Clinical trial outcomes for FDA-approved drugs do not automatically apply to compounded versions.

Real HRA + GLP-1 scenarios with numbers

Answer capsule

| Scenario | HRA type & amount | Plan rules | Best provider fit | Coverage outcome |

|---|---|---|---|---|

| A | $2,200 EBHRA (2026 max) | Allows weight-loss GLP-1s; LMN required | Shed at $199/mo (compounded semaglutide); Eden also fits ($129 first month, 3-mo plan) | HRA covers ~11 months of the starting program |

| B | $5,000 Integrated HRA | Allows GLP-1s with LMN; restricts to FDA-approved | Sesame ($59/mo annual + Wegovy® via Sesame partnership at $199/mo first 2 months, then $349/mo) | ~$4,596 first-year total — HRA covers full year + ~$400 left |

| C | $1,500 Specialty GLP-1 HRA (Benepass / WEX / Sentinel) | Restricts to specific FDA-approved medications | Ro annual plan — $39 first month, then ~$74/mo on annual; Foundayo™ from $149/mo at lowest dose via LillyDirect | Covers meaningful months of brand-name access |

| D | $7,500 ICHRA | Covers qualified medical expenses broadly | Shed at $199–$249/mo (compounded) | HRA covers ~2+ years of a $249/mo program |

Each scenario assumes the HRA reimburses successfully. Real-world reimbursement depends on documentation quality and your specific plan design.

Take the quiz and match to the right provider for your HRA

60 seconds. We ask about HRA type, priorities, and state.

How we ranked HRA-compatible GLP-1 providers

Answer capsule

The criteria, in order

- Does the provider publicly name HRA as an accepted payment source? Only Sesame passes this test cleanly. That’s why Sesame leads.

- Does the provider publicly document itemized receipts and the reimbursement workflow? Hers, Hims, Ro, and Shed pass with publicly documented receipts. Sesame, Eden, and MEDVi issue receipts but the exact format and content aren’t publicly standardized. Yucca fails.

- Does the provider support LMN requests? Shed publicly documents LMN support; Sesame, Hers, Hims, Ro, and Eden support clinician-initiated documentation through the portal; MEDVi is not publicly documented.

- Does the provider carry FDA-approved medication? Ro (Zepbound®, Foundayo™) and Sesame lead here.

- Is pricing transparent and billing predictable? Sesame, Hers, Hims, Ro, Shed, and Eden all publish starting prices. MEDVi publishes first-month and refill pricing separately.

- Are there material regulatory disclosures readers should know about? MEDVi received an FDA warning letter dated February 20, 2026 — we disclose this in the MEDVi section.

What we did not do

- We did not test every provider’s checkout flow with a real HRA card.

- We did not file real claims through each provider’s receipts.

- We did not independently verify Yucca’s policies beyond their public FAQ.

Where we couldn’t confirm a claim, we flagged it. If you see “not publicly documented” on any row of our matrix, contact the provider before you assume anything.

Affiliate disclosure

Frequently asked questions about GLP-1 providers that accept HRA

Still not sure which GLP-1 program fits your HRA?

You don’t have to figure this out alone.

Take our free 60-second matching quiz. We’ll ask about your HRA type, your priorities (price, FDA-approved vs compounded, oral vs injection), and your state. We’ll match you to the GLP-1 program with the cleanest reimbursement path for your specific situation — no sales pressure, no spam, just a personalized action plan.

Find the GLP-1 program with the cleanest HRA reimbursement path

60 seconds. Personalized to your HRA setup and state.

Ready to start?

If you already know what you need:

Medical disclaimer

This page is for informational purposes only and is not medical advice. GLP-1 medications are prescription drugs that may not be appropriate for everyone. Always consult a licensed healthcare provider before starting, changing, or stopping any medication. Compounded medications are not FDA-approved and carry risks that differ from FDA-approved drugs. Tell your healthcare provider about all medications you take and your complete medical history.

Sources and references

- IRS Publication 502 and Publication 969

- IRS FAQ on nutrition, wellness, and general health expenses

- Healthcare.gov: HRA glossary and ICHRA guidance

- FDA: Foundayo approval announcement, April 1, 2026

- FDA: Policy on compounders as GLP-1 supply stabilizes

- FDA: Kin Meds (MEDVi) warning letter, February 20, 2026

- DOL / EBSA: Benefit claims procedure regulation

- HHS: HIPAA and workplace wellness

- Ogletree Deakins: Employers Grapple With GLP-1 Coverage for Weight Loss (November 2025)

- NFP: GLP-1 Discrimination Considerations for Employer Plans

- Benepass: Tame GLP-1 Costs With Specialty HRAs

- Alegeus: GLP-1s + CDH accounts: What benefits admins need to know

- HSA Store: Weight Loss Drugs eligibility

- Sesame Care: Online weight loss program payment info and insured/payment FAQ

- Hers: HSA/FSA reimbursement workflow

- Hims: Weight loss care + HSA/FSA workflow

- Ro: Cost and pricing FAQ and Ro Body pricing

- Shed: HSA/FSA and documentation help

- Embody: About and pricing

- Yucca Health: FAQ

- HealthEquity: Member reimbursement processing times

- WEX: Benefits toolkit — eligible expenses

- VEHI: HRA/FSA/GLP-1 notice, January 29, 2026

Related guides on Weight Loss Provider Guide

- Is GLP-1 HRA Eligible? The 3-Gate Test (With LMN Template & Email Script)

- GLP-1 Providers That Accept HSA

- Best Brand-Name GLP-1 Telehealth Providers

- Best GLP-1 Online Programs

- Best Compounded Semaglutide

- Does Sesame Accept HSA/FSA?

- Does SHED Accept HSA/FSA?

Last verified: . We re-verify provider pricing, HRA/HSA/FSA payment language, FDA regulatory status, and material compliance disclosures on a monthly cadence. If you spot something out of date, let us know.