Does Sesame Accept HSA/FSA? Yes — Here’s What’s Actually Covered in 2026

Weight Loss Provider Guide is an independent comparison resource for GLP-1 telehealth providers.

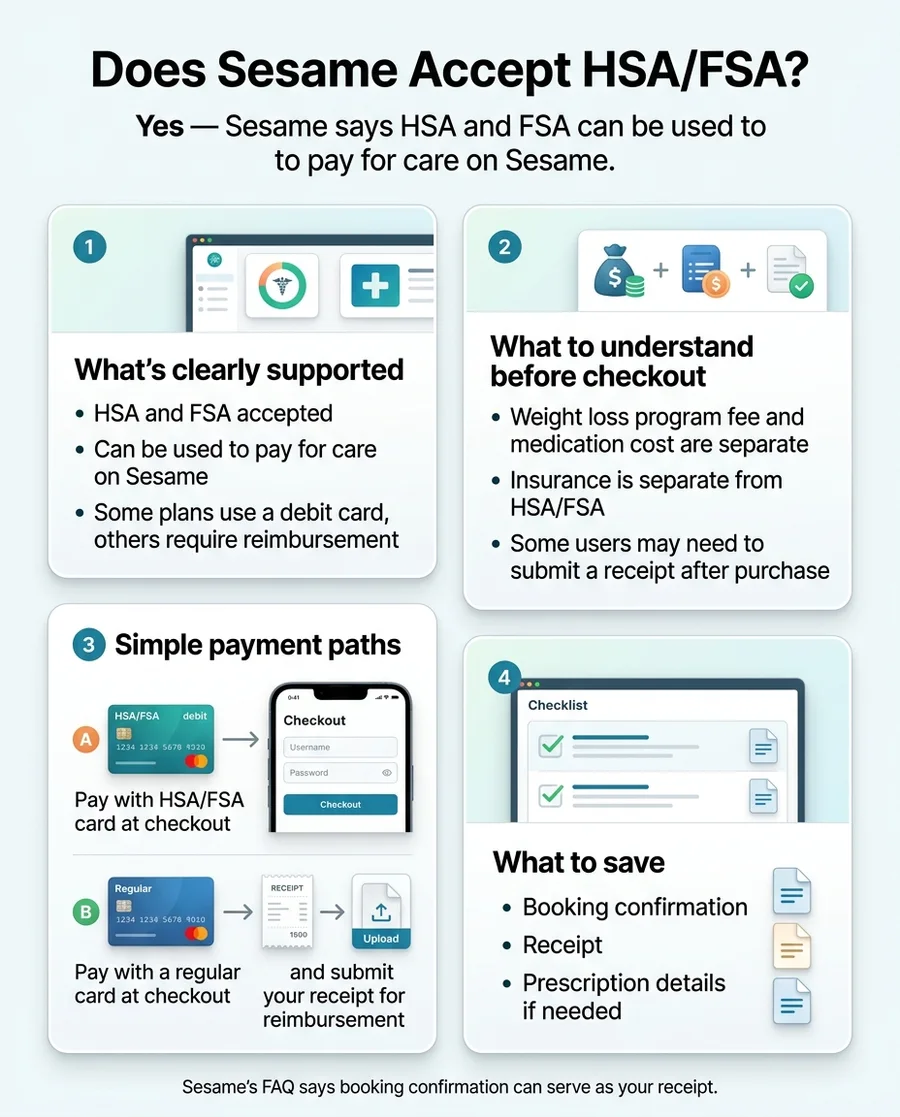

Yes — Sesame accepts HSA, FSA, and HRA funds across its services.

That includes Success by Sesame — the GLP-1 weight loss program — and the prescriptions that come with it: Wegovy, Zepbound, Ozempic, Mounjaro, and Foundayo. Swipe your HSA/FSA debit card at checkout the same way you’d swipe a Visa, or pay with a regular card and submit your receipt for reimbursement.

Two wrinkles most pages skip: Sesame’s weight-loss team will generate an itemized bill for HSA/FSA submission on request (the general site only provides a booking confirmation), and weight-loss prescriptions sometimes need extra documentation depending on your specific plan administrator. We cover both below.

| Question | Sesame’s Answer |

|---|---|

| Accepts HSA/FSA funds? | Yes — HSA/FSA directly, plus HRA per Sesame’s insured page |

| Program fee (Success by Sesame) | $59/mo on the annual plan (saves $480/year vs monthly); $99/mo monthly |

| Medication included in the fee? | No — priced separately starting at $149/month |

| Insurance help for medication? | Yes — providers assist with prior authorization for GLP-1s |

| Bills traditional insurance for the program? | No — direct-pay model |

| Cancellation window | Up to 48 hours before your renewal date |

| Costco member perk? | Yes — $349/mo Wegovy/Ozempic at Costco Pharmacy + 10% off Sesame services |

HSA/FSA accepted • From $59/mo on the annual plan • Same-day video visits

Does Sesame Accept HSA/FSA?

Yes. Sesame’s own homepage, FAQ, and insured page all confirm HSA and FSA funds are accepted for care on the platform, with the insured page adding HRA and other health-account funds. That applies to one-off telehealth visits, labs, the Success by Sesame weight loss subscription, and prescription medications — including GLP-1s like Wegovy and Zepbound.

If you have an HSA or FSA debit card, it processes at Sesame checkout exactly like a Visa, Mastercard, Amex, or Discover card. No special form, no insurance claim, no waiting. If your HSA card isn’t handy or you pay with a regular card by habit, you can still submit your Sesame receipt to your plan administrator’s portal for reimbursement.

That’s the 10-second answer. The reason this page keeps going is that “Sesame accepts HSA/FSA” is the easy part. What most readers actually want to know is which parts are covered, what kind of receipt Sesame hands you, and what could go wrong at your plan administrator — because weight-loss prescriptions follow slightly stricter rules than, say, an antibiotic.

What Can You Actually Pay for With HSA/FSA on Sesame? (The 3-Tier Breakdown)

Not every dollar you spend on Sesame is treated the same by the IRS or your plan administrator. We group Sesame’s charges into three tiers: Tier 1 is general medical care, Tier 2 is the Success by Sesame subscription, and Tier 3 is FDA-approved GLP-1 medications.

Visits and labs — the cleanest HSA/FSA case

A one-off telehealth visit on Sesame runs roughly $29 to $79 depending on specialty and provider. Urgent care, primary care, prescription refills, labs — these are standard medical care, eligible under IRS Publication 502 with a booking confirmation as your receipt.

Success by Sesame subscription — eligible, and Sesame will give you the paperwork

Success by Sesame, the weight loss program, is priced on a tiered subscription model:

| Plan | Price | Savings vs Monthly |

|---|---|---|

| Annual | $59/mo (billed annually) | $480/year |

| 6-Month | Billed every 6 months | $180 every 6 months |

| 3-Month | Billed every 3 months | $60 every 3 months |

| Monthly | $99/mo | — |

Here’s the part nobody else surfaces: Sesame’s general FAQ says your booking confirmation serves as your receipt and Sesame doesn’t issue additional paperwork for insurance claims. But Sesame’s weight-loss program page says something different — if you email [email protected], the Success by Sesame team will provide an itemized bill you can submit to your HSA or FSA.

FDA-approved GLP-1 medications — eligible, with documentation rules

FDA-approved GLP-1 medications prescribed through Sesame are HSA/FSA-eligible when they treat a diagnosed condition. Type 2 diabetes prescriptions (Ozempic, Mounjaro, Rybelsus) typically go through without extra paperwork. Weight-loss-indication prescriptions (Wegovy, Zepbound, Foundayo — or off-label weight-loss use of Ozempic/Mounjaro) can trigger a documentation request from your plan, especially on the FSA side.

| Medication | Pricing | HSA/FSA | Extra Docs? |

|---|---|---|---|

| Wegovy injection | $199/mo intro (first 2 fills), $349/mo ongoing — Novo promo through 6/30/26 | Yes | May be requested for weight-loss |

| Wegovy pill (oral semaglutide) | From $149/mo — Novo promo through 6/30/26 | Yes | May be requested for weight-loss |

| Ozempic | $199/mo intro, $349/mo ongoing — Novo promo | Yes | Rarely if for type 2 diabetes |

| Zepbound KwikPen (LillyDirect) | $299 (2.5mg), $399 (5mg), $499 (7.5mg), $699 (10/12.5/15mg); Self Pay Journey drops 7.5–15mg to $449 with 45-day refill timing | Yes | May be requested for weight-loss |

| Zepbound vial (LillyDirect) | $299 (2.5mg) up to $699 at higher doses | Yes | May be requested for weight-loss |

| Zepbound with insurance + prior auth | As low as $25/month | Yes | Usually not needed with coverage |

| Mounjaro | ~$1,080–$1,300/mo without insurance; Sesame providers assist with prior auth | Yes | Rarely if for type 2 diabetes |

| Foundayo (orforglipron, oral) | $149 (0.8mg), $199 (2.5mg), $299 (5.5/9mg), $349 (14.5/17.2mg) | Yes | May be requested for weight-loss |

| Contrave, metformin, topiramate | Varies; often under $50/mo | Yes | Usually not needed |

Costco member perk

A note on Sesame Plus ($10.99/mo or $99/year)

Booking Confirmation vs. Itemized Bill — The Paperwork Nobody Explains

Sesame issues two different kinds of receipts depending on what you’re paying for, and your plan administrator may care which one you submit. Here’s the side-by-side most pages don’t bother with:

| What You Paid For | What Sesame Provides | If Your Plan Wants More |

|---|---|---|

| One-off telehealth visit | Booking confirmation email (your receipt) | Forward the email to your administrator’s reimbursement portal |

| Success by Sesame subscription | Booking confirmation by default; itemized bill available on request from [email protected] | Email Sesame support and ask for the itemized bill specifically |

| Prescription filled at a pharmacy | Pharmacy receipt (not from Sesame) | Your pharmacy provides HSA/FSA-ready receipts separately |

| Letter of Medical Necessity | Not automatically issued — ask your provider if your plan requires one | Message your provider through the app |

The practical path

HSA/FSA vs. Insurance — Three Things Readers Keep Confusing

Many readers fuse “Sesame accepts HSA/FSA” with “Sesame takes my insurance.” They’re not the same. Sesame is a direct-pay marketplace — it does not bill traditional health insurance for the program fee or for visits. HSA/FSA is a payment method funded through pre-tax contributions; it’s not insurance.

| Concept | How It Works on Sesame |

|---|---|

| HSA/FSA acceptance | ✓ Yes — you can pay with HSA/FSA funds at checkout |

| Insurance billing for the program fee or visits | ✗ No — Sesame does not bill traditional insurance |

| Insurance help for medication cost | ✓ Yes — Sesame providers assist with prior authorization for GLP-1 medications |

That middle row is where most readers trip. If your top priority is paying a telehealth copay through insurance, Sesame isn’t the right platform. But if you’re in a high-deductible plan or uninsured, Sesame’s transparent cash prices plus HSA/FSA tax savings plus prior-authorization support on the medication often beat going through insurance entirely — especially once the medication cost drops toward $25/month with prior auth approved.

What Sesame Actually Costs Before and After HSA/FSA Tax Savings

Paying with HSA or FSA funds reduces your Sesame spend by roughly 12% to 37% depending on your federal marginal tax bracket, because those dollars skipped income tax on the way in. For someone in the 22% bracket, the $99/month Success by Sesame subscription has an effective cost of about $77. On a $349/month Wegovy ongoing prescription, the real cost after tax savings is roughly $272 — about $924 a year kept in your pocket on that medication alone.

Monthly effective cost by tax bracket

| Your Plan | Sticker | 12% | 22% | 24% | 32% | 37% |

|---|---|---|---|---|---|---|

| Success by Sesame only (annual) | $59/mo | $52 | $46 | $45 | $40 | $37 |

| Success by Sesame only (monthly) | $99/mo | $87 | $77 | $75 | $67 | $62 |

| Subscription + Wegovy intro (first 2 mo) | $298/mo | $262 | $232 | $226 | $203 | $188 |

| Subscription + Wegovy ongoing | $448/mo | $394 | $349 | $341 | $305 | $282 |

| Subscription + Wegovy pill (promo) | $248/mo | $218 | $193 | $188 | $169 | $156 |

| Subscription + Zepbound 2.5mg (LillyDirect) | $398/mo | $350 | $310 | $302 | $271 | $251 |

| Subscription + Zepbound 5mg (LillyDirect) | $498/mo | $438 | $388 | $378 | $339 | $314 |

| Subscription + Zepbound 7.5mg via Self Pay Journey | $548/mo | $482 | $427 | $417 | $373 | $345 |

| Subscription + insurance-covered GLP-1 | $124/mo | $109 | $97 | $94 | $84 | $78 |

Annual savings on common plans

| Plan | Sticker Annual Cost | Annual Savings (22%) | Annual Savings (32%) |

|---|---|---|---|

| Subscription + Wegovy ongoing (12 months) | $5,376 | $1,183 | $1,720 |

| Subscription + Wegovy pill (12 months) | $2,976 | $655 | $952 |

| Subscription + Zepbound 2.5mg (12 months) | $4,776 | $1,051 | $1,528 |

| Subscription only (annual plan, 12 months) | $708 | $156 | $227 |

Estimates based on federal marginal tax brackets. Actual savings often come out higher once FICA (for FSA contributions) and state income tax are factored in. Consult a tax professional for your specific situation.

2026 HSA contribution limits

Are GLP-1 Weight Loss Meds HSA/FSA Eligible? (IRS Rules, Plainly)

Yes — FDA-approved GLP-1 medications are HSA/FSA-eligible when prescribed to treat a diagnosed medical condition. That covers type 2 diabetes (always qualified under IRS rules) and obesity (which the IRS treats as a disease for medical-expense purposes). The medication has to treat a specific disease diagnosed by a physician — not be used for general weight loss, aesthetics, or wellness.

The IRS rule is simpler than most HSA/FSA blogs make it sound. Publication 502 says medical expenses are costs paid for the diagnosis, cure, mitigation, treatment, or prevention of disease. Weight-loss programs and drugs qualify when they’re prescribed to treat a specific disease diagnosed by a physician. They don’t qualify when they’re for “improvement of appearance, general health, or sense of well-being.”

You generally qualify if you have:

- BMI of 30 or higher (clinical threshold for obesity) plus a weight-loss prescription

- BMI of 27 or higher plus a weight-related condition — type 2 diabetes, hypertension, dyslipidemia, obstructive sleep apnea, cardiovascular disease, or non-alcoholic fatty liver disease

- Diagnosis of type 2 diabetes at any BMI, for a medication with a T2D indication

You probably won’t qualify if:

- BMI is under 27 with no comorbidities and the goal is general weight loss or appearance

- Prescription is written for aesthetic or wellness goals without a coded diagnosis

- You’re using a GLP-1 preventively with no active diagnosed condition

A practical note: Sesame’s weight-loss intake screens for these clinical criteria before prescribing. Providers on the platform prescribe GLP-1 treatment when it’s clinically appropriate for your profile — so if Sesame issues you a prescription for weight management, the medical basis is already documented in your chart. That documentation is what your plan administrator will actually want to see if they audit.

GLP-1 medications available through Sesame

Do You Need a Letter of Medical Necessity (LMN) for Sesame’s GLP-1 Program?

It depends on your plan. Sesame doesn’t automatically issue a Letter of Medical Necessity with every prescription. If your plan administrator specifically asks for an LMN, request one directly from your Sesame provider via the app or during your video visit. Type 2 diabetes prescriptions typically don’t need one. Weight-loss-indication prescriptions may, depending on how strictly your administrator verifies claims.

A Letter of Medical Necessity is a short written note from a licensed provider confirming that a treatment is medically necessary to treat a diagnosed condition. It usually includes the diagnosis (ideally with an ICD-10 code), a statement of medical necessity, the specific medication or service prescribed, and the provider’s signature and credentials.

FSA users

FSA administrators tend to verify each weight-loss-related charge at reimbursement time, which is where documentation requests most often appear.

HSA users

HSAs are usually more self-directed at the point of purchase, but the IRS can audit up to three years back. Keeping an LMN on file (if one is written) is cheap insurance.

Limited-purpose FSA

Limited-purpose FSAs (dental and vision only) won’t cover GLP-1 at all — this is a separate account type you may have alongside an HSA.

How to ask Sesame for documentation

For the itemized bill, email [email protected] with your subscription order number.

For a Letter of Medical Necessity, message your provider directly through the Sesame app after your first visit. A one-sentence request is enough: “Can you provide a letter of medical necessity documenting my diagnosis and why this GLP-1 medication is medically necessary, for my HSA/FSA administrator?”

Save any documentation provided to your email and a secure folder — the IRS audit window is three years, and seven years is a safer cushion.

How to Actually Use Your HSA/FSA at Sesame — Step by Step

Two paths work. Path A: use your HSA/FSA debit card directly at Sesame checkout — it processes like any Visa. Path B: pay with a regular card and submit your receipt (or the itemized bill from Success by Sesame support) for reimbursement. Path A is faster; Path B earns you credit-card points plus the reimbursement. Both are legitimate under IRS rules.

1Before booking

Log into your HSA or FSA portal. Confirm balance, make sure your debit card is active and not expired, and note your administrator’s reimbursement portal URL in case Path B becomes relevant.

2Pick your plan

Success by Sesame at $59/mo (annual, saves $480/year) or $99/mo (monthly). The 6-month and 3-month options sit in between.

3Book your first video visit

During the visit, share your medical history, goals, and any existing diagnoses. If your plan administrator is strict about weight-loss prescriptions, ask your provider for a Letter of Medical Necessity then.

4Pay at checkout

Enter your HSA/FSA debit card in the payment field. Sesame accepts Visa, Mastercard, Amex, and Discover — your HSA/FSA card runs on whichever network issued it.

5Save your receipt

Sesame emails a booking confirmation. For the Success by Sesame subscription specifically, email [email protected] to request the itemized bill for your records.

6If you paid with a regular card (Path B)

Log into your plan administrator’s portal, find "Request Reimbursement," upload the Sesame booking confirmation or itemized bill (plus LMN if requested), and submit. Most plans process reimbursement within 5–10 business days.

7For medication

When you fill your prescription at CVS, Walgreens, Costco Pharmacy, Walmart, or via mail-order (Sesame lets you choose), pay with the same HSA/FSA card or save the pharmacy receipt for reimbursement. Pharmacy-side HSA/FSA acceptance is separate from Sesame-side acceptance.

Choose your provider • Same-day appointments available

If Your HSA/FSA Card Is Declined at Sesame: 4-Step Fix

A declined HSA/FSA card at Sesame is almost always a documentation or classification issue — not a fundamental eligibility issue. The four most common causes, in frequency order: (1) zero balance or expired card, (2) administrator flagged the charge for review, (3) limited-purpose FSA that only covers dental and vision, or (4) merchant category code mismatch. All four are fixable.

Step 1 — Check the basics

Log into your HSA/FSA portal. Confirm: balance above zero, card not expired, and you haven’t accidentally selected a Dependent Care FSA (a separate account that only covers childcare, not medical expenses).

Step 2 — Pay with a regular card, save the receipt, and submit for reimbursement

This is almost always the cleanest fix. Sesame’s booking confirmation is a valid receipt. For Success by Sesame specifically, email [email protected] to request the itemized bill first — it’s often what trips a stubborn administrator into approving the claim. Most administrators process reimbursement in 5–10 business days.

Step 3 — If reimbursement is denied, add documentation

The most common denial reason for weight-loss-indication prescriptions is missing proof of medical necessity. Request a Letter of Medical Necessity from your Sesame provider, upload it with your resubmission, and reference IRS Publication 502 in the notes — specifically the section stating that weight-loss drugs prescribed to treat a specific disease diagnosed by a physician qualify as medical expenses.

Step 4 — If the denial persists, appeal

Every administrator has a formal appeals process. Your appeal should include the prescription, the LMN, your diagnosis on record, and a citation to IRS Publication 502. Denials at this stage are unusual once the full documentation package is on file.

Sesame vs. Ro vs. Hims/Hers vs. Eden — HSA/FSA Friction Compared

All four platforms support HSA/FSA funds for weight-loss care, but the workflow differs. Sesame and Eden are the cleanest for card-at-checkout simplicity; Ro wins if insurance support on the medication is the priority.

| Provider | HSA/FSA Card at Checkout? | Reimbursement | Program Fee | Insurance Help | Best For |

|---|---|---|---|---|---|

| Sesame | ✓ Yes | ✓ Yes — itemized bill on request | $59–$99/mo | Prior auth help for GLP-1 medications | Provider choice, Costco members, cash-pay clarity |

| Ro | ⚠ Reimbursement flow | ✓ Yes | $39 intro, then $149/mo (as low as $74/mo with annual paid upfront) | Strong insurance concierge for Zepbound, Foundayo | Insurance-first shoppers wanting FDA-brand GLP-1s |

| Hims / Hers | ⚠ Mostly reimbursement | ✓ Yes | Varies | Limited | Readers comfortable with reimbursement workflows |

| Eden | ✓ Yes | ✓ Yes | No membership fee | Cash-pay only | Broad self-pay, Wegovy/Zepbound flagged HSA/FSA-eligible at checkout |

Sesame lets you choose your own provider — you browse profiles, read reviews, pick your doctor. That’s the platform’s signature feature.

Ro’s insurance support is strong. If you have coverage and want Ro’s team to run prior authorization and get you to a $25/month copay on branded Zepbound or Foundayo, Ro is the better fit. The trade-off: Ro’s HSA/FSA flow is reimbursement-based, not direct-card.

Eden is the cleanest zero-membership cash-pay alternative. If Sesame’s program fee is a dealbreaker and you want branded Wegovy or Zepbound flagged HSA/FSA-eligible at checkout without a subscription, Eden is worth checking.

Still comparing? See our full HSA/FSA GLP-1 provider comparison or take our 60-second matching quiz and we’ll route you based on your insurance, budget, BMI, and medication preference.

Not sure if Sesame fits? We'll match you with the best HSA/FSA-friendly GLP-1 provider in 60 seconds.

The One Thing Sesame Doesn’t Do (Honest Admission)

Sesame does not bill traditional health insurance for the program fee or for visits. If having your provider visit billed through insurance is your top priority, Sesame isn’t your fit, and Ro or your in-network PCP is a better path.

But because Sesame skips the program-side insurance billing, it can publish transparent cash prices up front, let you choose your own provider, accept HSA/FSA directly at checkout, and still help with prior authorization on your GLP-1 so the medication itself can drop to around $25/month when covered by your plan. For most readers who want the tax benefits of HSA/FSA plus the simplicity of cash pricing, that’s a trade worth making.

Who Sesame Is Best For (and Who Should Look Elsewhere)

Sesame is a strong HSA/FSA fit if you:

- Want to choose your own provider — browse profiles, read reviews, pick your doctor

- Are a Costco member — $349/mo Wegovy/Ozempic + 10% off Sesame services

- Prefer local pharmacy pickup over mail-order shipments

- Have HSA/FSA dollars ready plus insurance that may cover the GLP-1 medication

- Want transparent cash pricing on the program fee and prior-authorization help on the medication

Sesame is probably not the best fit if you:

- Need your program visit billed through traditional insurance

- Want a zero-membership cash-pay model without any subscription fee

- Require CPT-coded insurance superbills on every submission

- Have had prior issues with refill timing or customer service on similar marketplaces

Honest limitations

What patients say

“I love this service. It was extremely convenient.”

— Patient testimonial, sesamecare.com homepage

“Very happy it was so convenient and fast.”

— Patient testimonial, sesamecare.com homepage

“I’ve used an HSA debit card at Sesame.”

— Reddit user, r/SemaglutideFreeSpeech thread on online providers accepting HSA

These quotes illustrate payment-experience and service-experience signals, not typical clinical outcomes. Individual results vary.

What We Actually Verified (and What We Didn’t)

Every commercial page in a YMYL category should be transparent about what’s verified versus what’s editorial. Here’s our split for this page as of .

What we verified from primary sources

- ✓Sesame’s HSA/FSA acceptance language across the homepage, FAQ, insured page, and Terms of Service

- ✓Success by Sesame subscription tiers: $59/mo annual (saves $480/year), 6-month, 3-month, and $99/mo monthly

- ✓Success by Sesame itemized bill availability on request from [email protected]

- ✓General Sesame FAQ language: booking confirmation serves as the receipt for most visits

- ✓Sesame cancellation policy: cancel up to 48 hours before renewal

- ✓Wegovy pricing on Sesame: $199/mo intro (first 2 fills), $349/mo ongoing via Novo Nordisk promo through 6/30/26; Wegovy pill from $149/mo

- ✓Zepbound self-pay pricing (LillyDirect): $299 (2.5mg), $399 (5mg), $499 (7.5mg), $699 (10/12.5/15mg); Self Pay Journey drops 7.5–15mg to $449 with 45-day refill timing

- ✓Zepbound with insurance + prior auth: as low as $25/month

- ✓Foundayo pricing: $149 (0.8mg), $199 (2.5mg), $299 (5.5/9mg), $349 (14.5/17.2mg)

- ✓Costco partnership pricing: $349/mo Wegovy/Ozempic at Costco Pharmacy, Wegovy pill as low as $149/mo, 10% off Sesame services

- ✓Costco membership fees: Gold Star $65/year, Executive $130/year total

- ✓IRS Publication 502 rule on weight-loss programs qualifying when prescribed for a specific disease

- ✓2026 HSA contribution limits: $4,400 self-only / $8,750 family / $1,000 catch-up at 55+ (IRS Revenue Procedure 2025-19)

What is editorial judgment, not verified policy

- ⚠Sesame Plus membership ($10.99/mo or $99/yr) HSA/FSA eligibility — we classify it as likely not eligible based on IRS rules distinguishing medical care from discount memberships. Sesame has not published an official position. Confirm with your plan administrator.

- ⚠Tax savings calculator outputs are estimates based on federal marginal tax brackets. Actual savings are typically higher once FICA (for FSA) and state income tax are included.

- ⚠Our provider-fit recommendations are editorial conclusions based on the verified facts above, not paid rankings.

What we did NOT verify

- ✗We did not live-test an HSA debit card at Sesame checkout ourselves. Our confidence comes from Sesame’s stated policy and the absence of contrary evidence in reported user experience.

- ✗We did not independently verify every pharmacy-network HSA/FSA acceptance flow — pharmacy-side acceptance is a separate rail from Sesame-side acceptance.

- ✗We did not contact every HSA/FSA administrator to confirm their individual documentation requirements. Administrator nuance varies plan to plan.

Frequently Asked Questions

Still not sure which GLP-1 program is right for you? We'll ask a few quick questions about your situation — insurance status, budget, BMI, medication preference, state — and match you with the providers most likely to fit.

Methodology

We wrote this page by cross-referencing Sesame Care’s public FAQ, Terms of Service, weight loss program page, individual medication pages (Wegovy, Zepbound, Ozempic, Foundayo, Mounjaro), Costco partnership announcement, and Success by Sesame launch blog — then checking every commercial claim against IRS Publication 502, IRS Revenue Procedure 2025-19 (2026 HSA limits), IRS FAQs on medical expenses, Eli Lilly’s Zepbound savings pages, and administrator guidance from HSA Store, FSA Store, Fidelity, and Empower. Real-world user experience data came from Reddit threads on r/Semaglutide, r/Zepbound, r/HSA, plus ConsumerAffairs and Trustpilot reviews. Pricing was verified from primary sources on April 16, 2026. We re-verify every 60 days while Novo Nordisk promotional pricing is active (through December 31, 2026), then quarterly.

Related guides

- GLP-1 Providers That Accept HSA/FSA — Full 2026 Comparison

- Does Eden Take HSA or FSA? Verified 2026 Answer

- Semaglutide Providers That Accept HSA — Wegovy & Compounded Options

- Tirzepatide Providers That Take FSA & HSA

- Best Brand-Name GLP-1 Telehealth Providers (2026)

- Best GLP-1 Telehealth Providers (April 2026)

Last verified: • Next scheduled review: • Author: Weight Loss Provider Guide Editorial Team

Editorial Disclosure: Weight Loss Provider Guide is an independent comparison resource for GLP-1 telehealth providers. We earn affiliate commissions when readers sign up for providers through our links, including Sesame. Those commissions do not change the IRS rules cited on this page, Sesame’s published policies, or the honest limitations we’ve flagged. Sesame is the primary recommendation on this page because you searched for Sesame specifically — not because it’s our top-paying affiliate.

Medical & Tax Disclaimer: This page is informational and does not constitute medical, tax, or legal advice. Consult a licensed healthcare provider about GLP-1 therapy and a tax professional about HSA/FSA rules specific to your situation. Full medical disclaimer →