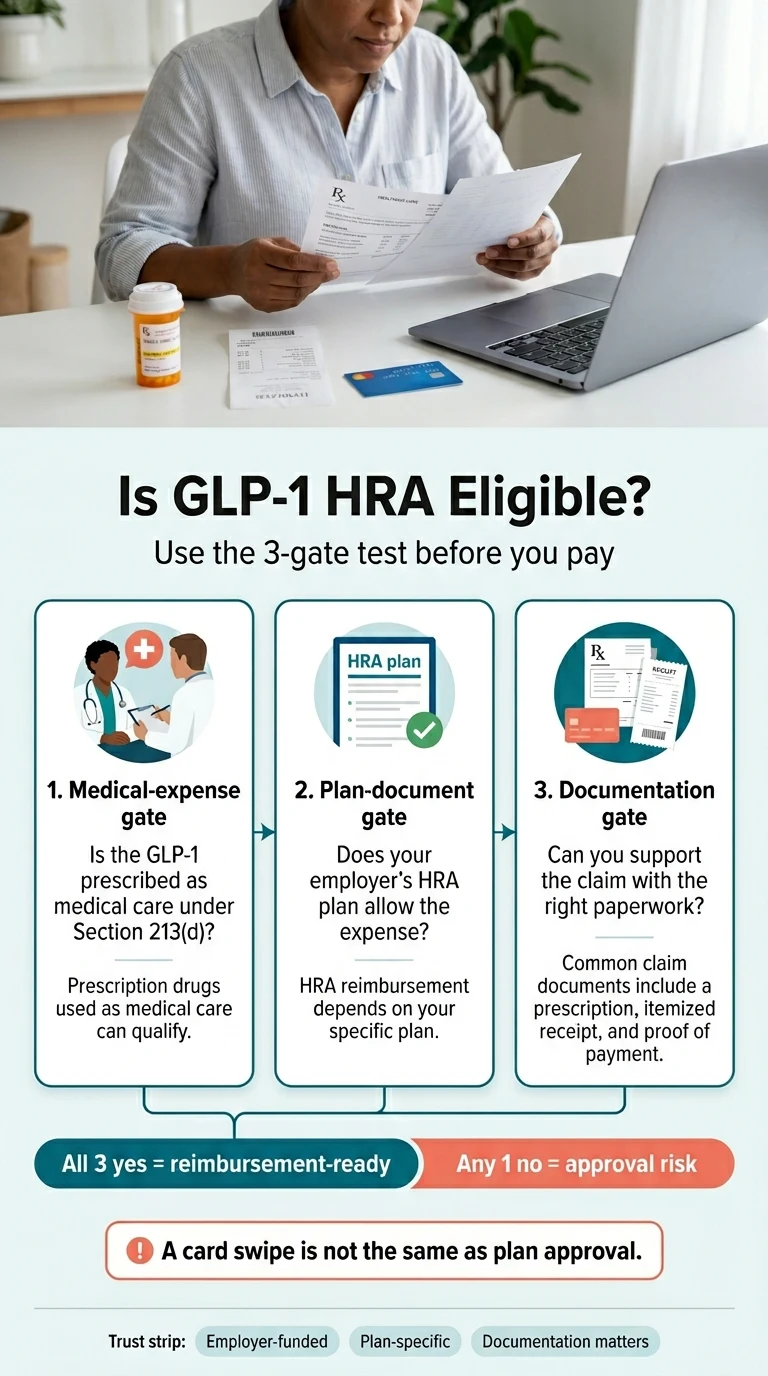

Is GLP-1 HRA Eligible? The 3-Gate Answer Before You Swipe

Short answer: Yes — with conditions.

GLP-1 medications can be HRA eligible when your prescription clears three gates: it's prescribed for a diagnosed medical condition, your employer's HRA plan allows it, and you can substantiate the claim with the right paperwork. The IRS treats prescribed drugs for diagnosed disease as qualified medical expenses under Section 213(d), so GLP-1s like Wegovy, Zepbound, Ozempic, Mounjaro, and Foundayo can qualify on paper. But here's what most pages skip: a swipe that goes through is not the same as a claim that gets approved. Your HRA plan can be narrower than the IRS rulebook — and if it is, you can owe the money back.

| Gate | Question to answer | If "no" |

|---|---|---|

| 1. Medical-expense gate | Is the GLP-1 prescribed to diagnose, treat, mitigate, or prevent a disease? | IRS eligibility is weak. |

| 2. Plan-document gate | Does your employer's HRA actually allow this medication? | Card may swipe; claim may still be denied. |

| 3. Documentation gate | Can you produce a prescription, itemized receipt, and (sometimes) a Letter of Medical Necessity? | Reimbursement gets delayed or rejected. |

| Pass all three: reimbursement-ready. Miss one: at risk. | ||

Not sure which gate trips you up?

Take our free 60-second match quiz and get a personalized payment-path checklist — which providers support HRA, HSA, or FSA checkout, which provide detailed receipts, and what to ask your administrator before paying.

Is GLP-1 HRA eligible? What "HRA eligible" actually means

Last verified:Answer: "HRA eligible" means your employer-funded reimbursement account may cover the expense if it qualifies as medical care under IRS rules and your specific HRA plan permits it. HRAs are funded entirely by your employer and governed by your employer's plan document, which makes HRAs more plan-specific than HSAs or FSAs — a provider page that says "HSA/FSA eligible" tells you very little about whether your HRA will reimburse the same charge.

Three phrases get used as if they're identical. They aren't:

| Phrase | What it actually means | Why it matters |

|---|---|---|

| HRA eligible | The expense fits IRS medical-expense rules under Section 213(d). | A starting point. Not enough to guarantee payment. |

| HRA reimbursable | Your specific employer plan allows this expense. | This is the line that matters for getting paid. |

| HRA card accepted | The merchant's payment processor allowed the swipe. | Approval at checkout is not a guarantee from your plan. |

The IRS describes a Health Reimbursement Arrangement as an employer-funded plan that reimburses qualified medical expenses up to a maximum dollar amount, where the reimbursements aren't taxable income to you (Source: IRS Publication 969). The phrase "qualified medical expenses" sounds standardized — but plan documents can, and routinely do, narrow what's reimbursable. Your employer can exclude weight-loss medications. Your plan can require prior authorization. Your administrator can demand a Letter of Medical Necessity for any prescription that isn't obviously tied to a covered diagnosis. None of that violates IRS rules. All of it changes whether your GLP-1 claim gets paid.

Most "is GLP-1 HSA/FSA eligible" guides treat the IRS rule as the final answer. For HRAs, the IRS rule is just the floor. For a full comparison of GLP-1 providers that work with HSA and FSA, see our GLP-1 Providers That Accept HSA/FSA guide.

The card-approval trap: why "it went through" doesn't mean "you're safe"

Answer: A successful HRA card transaction at a pharmacy or telehealth checkout doesn't prove your plan will accept the expense. Payment processors approve cards based on whether the merchant category looks medical — they don't check your specific employer's plan document. If your plan later determines the expense wasn't reimbursable, you can be required to repay the HRA. This is the most expensive mistake we see GLP-1 shoppers make, and it's avoidable.

Real example from a real employer plan document

The Vermont Education Health Initiative — a major school-employee benefits administrator — told its members in early 2026 that GLP-1 medications used exclusively for weight loss are not eligible for coverage under any of its health plans. The notice went further: it warned that pharmacy debit transactions might still process at checkout because the medication appears to qualify under broad IRS rules, but if the plan excludes weight-loss GLP-1s, members whose HRA dollars were inappropriately used would need to repay those funds. The same plan still allowed HRA dollars for GLP-1s prescribed for diabetes and cardiovascular conditions, with prior approval.

Read that twice. The card worked. The plan still said no.

This is the trap. And it's exactly what makes so many GLP-1 HRA stories on Reddit end with "now they're saying I owe the money back." It's not the IRS coming after you — it's your own plan administrator, weeks or months after you swiped.

The fix is boring and effective

Confirm before you pay. Don't trust the merchant. Don't trust the card. Confirm the expense with your administrator in writing, in plain language, before the transaction happens. Later in this guide we give you the exact email to send.

Don't get stuck repaying your HRA.

The 60-second quiz routes you to the lowest-risk payment path for your plan type — direct card, reimbursement, insurance-first, or cash-pay — and tells you exactly what to confirm with your administrator first.

Does your HRA type change the answer? (ICHRA vs GCHRA vs QSEHRA vs EBHRA)

Last verified:Answer: Yes — materially. There are five common HRA structures, each with different rules about what they can reimburse, how much, and how they interact with other benefits like HSAs. Knowing your HRA type narrows the question from "does the IRS allow this?" to "does my HRA allow this?" — which is the question that actually controls whether you get reimbursed.

Integrated HRA / Group Coverage HRA (GCHRA)

The most common employer setup. The HRA is paired with your employer's group health plan, and only employees enrolled in that plan can use it. Some plans apply clinical criteria, prior authorization rules, formulary limits, or exclusions for weight-loss drugs — check your plan document before assuming GLP-1 reimbursement.

ICHRA (Individual Coverage HRA)

ICHRAs let employers of any size reimburse you for individual-market premiums plus medical expenses, with no IRS-mandated cap on contributions. An ICHRA can reimburse Section 213(d) medical expenses if designed that way, but the employer's ICHRA plan document still controls whether GLP-1 expenses are reimbursable.

QSEHRA (Qualified Small Employer HRA)

QSEHRAs are limited to employers with fewer than 50 full-time-equivalent employees that don't offer group health coverage. The 2026 IRS limits cap reimbursement at $6,450 for self-only and $13,100 for family coverage (Source: IRS Publication 15-B, 2026). At those caps, a QSEHRA may cover only 3–6 months of a typical GLP-1 program before you've hit the limit — plan accordingly.

EBHRA (Excepted Benefit HRA)

EBHRAs stand alone from your employer's group plan and are capped at $2,200 for 2026. They were designed for vision, dental, and supplemental costs — but technically they can reimburse §213(d) medical expenses, including prescriptions.

Critical HSA warning

HHS guidance has indicated that an EBHRA reimbursing prescription drugs on a first-dollar basis can be treated as not "excepted," which can disqualify you from contributing to an HSA if you're enrolled in a high-deductible health plan. If you're on an HDHP with an HSA, using your EBHRA for a GLP-1 prescription before meeting your deductible can quietly eliminate your HSA contribution eligibility for that year.

Specialty / Carve-out GLP-1 HRA

A growing number of employers are using purpose-built GLP-1 HRAs administered by platforms like Sentinel Group and Benepass. These are designed specifically for GLP-1 reimbursement and sit outside the medical plan, with their own eligibility criteria — typically BMI thresholds, participation in a coaching or clinical-monitoring program, and sometimes restrictions on which pharmacies or medications qualify.

A note on Lifestyle Spending Accounts (LSAs)

LSAs get confused with HRAs constantly because both are employer-funded — but an LSA is not an HRA. LSA reimbursements are taxable income to you, not tax-free like HRA dollars. Check the employer's specific LSA rules if you have one.

The HRA × GLP-1 reimbursement-likelihood matrix

| HRA type | GLP-1 for diabetes (Ozempic, Mounjaro) | FDA-approved weight-loss GLP-1 (Wegovy, Zepbound, Foundayo) | Compounded semaglutide / tirzepatide |

|---|---|---|---|

| Integrated / GCHRA | Often reimbursable; check plan | Conditional — LMN often required; check plan | Often excluded |

| ICHRA | Often reimbursable; check plan | Conditional — LMN often required; check plan | Employer discretion |

| QSEHRA | Reimbursable within 2026 cap if plan allows | Reimbursable within cap if plan allows; LMN common | Employer discretion |

| EBHRA | Reimbursable within $2,200 cap; HDHP+HSA caveat | Reimbursable within cap; HDHP+HSA caveat | Same + HDHP+HSA caveat |

| Specialty GLP-1 HRA | Varies by program | Typically yes — that's the point | Often excluded |

Last verified: April 24, 2026, against IRS Publication 502 (2025), IRS Publication 969 (2025), IRS Publication 15-B (2026), IRS Rev. Proc. 2025-32 (FSA limits), HHS guidance on excepted-benefit status, and current employer-benefit analyses from Alliant, NFP, Akerman, and Mercer.

Brand-by-brand: Wegovy, Zepbound, Ozempic, Mounjaro, Foundayo

Answer: FDA-approved GLP-1 brands can be HRA eligible when prescribed for medical care, allowed by the HRA plan, and properly documented. The practical difference is which plans cover which brand for which use — most plans cover GLP-1s prescribed for diabetes more readily than the same molecule prescribed for weight loss. The indication on your prescription matters more than the brand name.

Wegovy (semaglutide)

FDA-approved for chronic weight management in adults with obesity or overweight with at least one weight-related comorbidity, and in adolescents 12+ with obesity. Also approved to reduce risk of major adverse cardiovascular events in adults with established cardiovascular disease and overweight or obesity. Wegovy pill is FDA-approved for chronic weight management in adults.

Zepbound (tirzepatide)

FDA-approved for chronic weight management in adults with obesity or overweight with comorbidity, and for moderate-to-severe obstructive sleep apnea in adults with obesity. Available as Zepbound pen, KwikPen, and single-dose vial.

Ozempic (semaglutide, T2D-labeled)

FDA-approved for type 2 diabetes, plus reducing risk of major adverse cardiovascular events in T2D adults with established cardiovascular disease, and slowing chronic kidney disease progression in T2D.

Mounjaro (tirzepatide, T2D-labeled)

FDA-approved for type 2 diabetes.

Foundayo (orforglipron) — new in 2026

NEWFoundayo was FDA-approved on April 1, 2026 for chronic weight management in adults with obesity or adults with overweight plus at least one weight-related comorbid condition. Treat the same as Wegovy and Zepbound for HRA purposes — reimbursable when documentation matches the medical record, with LMN commonly required for weight-loss use. Because Foundayo was approved recently, confirm whether your HRA plan lists it before assuming reimbursement.

Ro Body

Ro carries Foundayo, Wegovy pill, Wegovy pen, Zepbound pen, and Zepbound KwikPen. They run a free GLP-1 Insurance Coverage Checker and include an insurance concierge that handles prior authorization for you. Ro provides detailed itemized receipts you can submit to your HRA after purchase — the cleaner path for most insurance-coordinated HRAs.

$39 first month · as low as $74/month with annual plan

See FDA-approved GLP-1 options on RoCompounded vs FDA-approved GLP-1: what changes for HRA reimbursement

Answer: IRS medical-expense rules don't create a GLP-1-specific brand-versus-compounded reimbursement answer. A prescribed compounded medication may be submitted only if it's medical care, lawful, plan-permitted, and substantiated — and the HRA plan may still exclude it. After the FDA's April 1, 2026 clarification on compounding policies and the resolution of the semaglutide and tirzepatide shortage designations in 2025, more plan administrators have added explicit carve-outs for compounded GLP-1s.

If your HRA permits compounded products and you want a needle-averse or oral compounded path, there are providers built around exactly that lane. If your HRA excludes compounded products, the safer route is an FDA-approved brand or paying cash and skipping HRA reimbursement on that purchase. For more on provider options, see our GLP-1 Providers That Accept HRA guide.

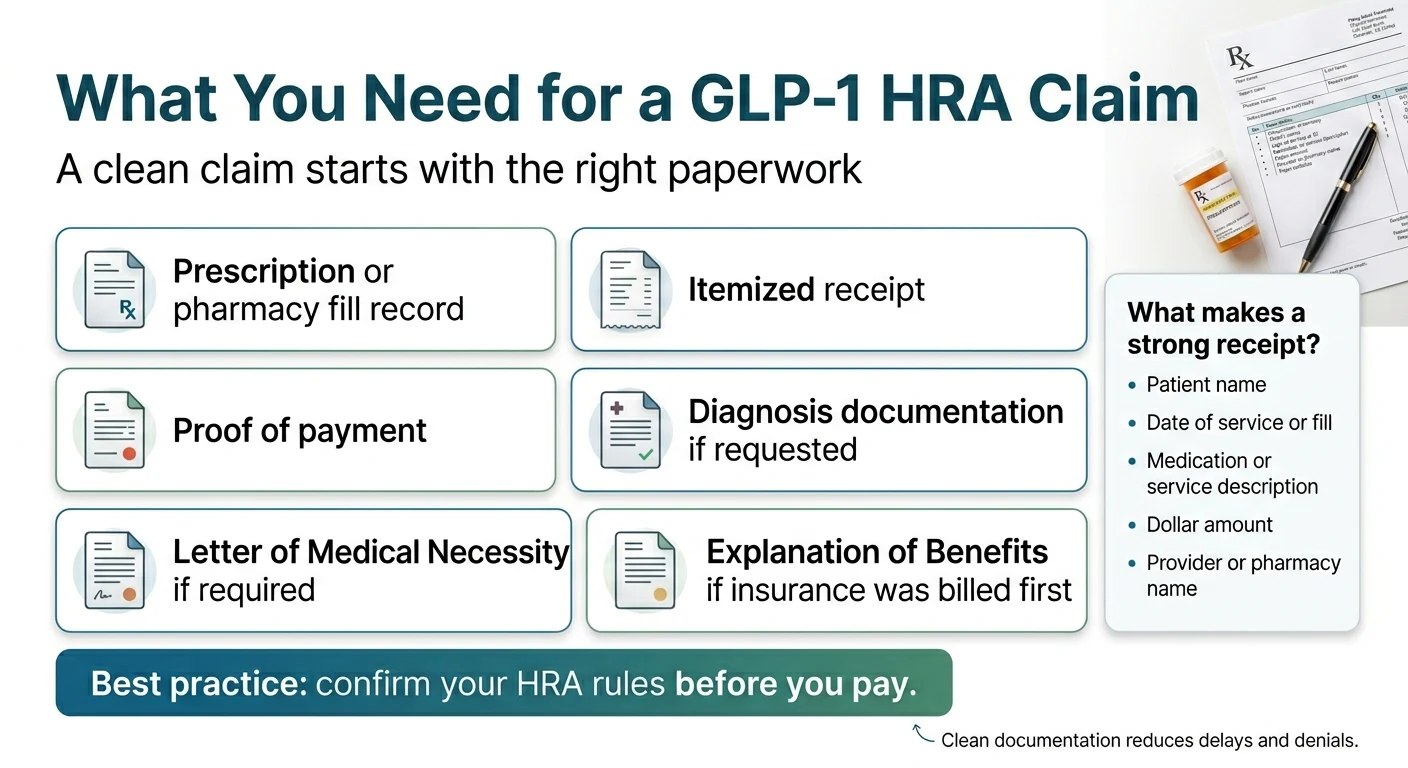

What documentation do you actually need for GLP-1 HRA reimbursement?

Answer: Most GLP-1 HRA claims should be prepared with a prescription, an itemized receipt, proof of payment, and any plan-required medical-necessity documentation. Weight-loss prescriptions commonly face more documentation requests, often including a Letter of Medical Necessity.

The core documentation checklist

- The prescription or pharmacy fill record showing the medication name and prescribing provider.

- An itemized receipt showing patient name, date of service, medication or service description, dollar amount, and provider or pharmacy name.

- Proof of payment (card statement, receipt, or paid invoice).

- Diagnosis documentation in your medical record — including the ICD-10 code for the prescribing condition.

- Letter of Medical Necessity (LMN) if requested — typical for weight-loss indication.

- Explanation of Benefits (EOB) if insurance was billed before the HRA claim.

- Prior authorization decision if your plan required one.

What a "clean" itemized receipt looks like

This is where most denials happen. Telehealth providers commonly bundle the medication, visit, and membership into a single line item like "weight management program — $299." That language can get flagged because it reads as general wellness rather than medical care.

A clean receipt has:

- Patient name that matches the HRA holder (or covered spouse/dependent).

- Date of service or fill.

- Medication name (and NDC for FDA-approved drugs when possible) on its own line — separate from any program or subscription fee.

- Provider or pharmacy name with credentials.

- Itemized dollar amount for the medication specifically.

- Total paid and payment method.

Ask any provider for a "split invoice" or "itemized medical receipt" if their default checkout summary doesn't break it out.

Letter of Medical Necessity — Copy-Paste Template

LETTER OF MEDICAL NECESSITY — GLP-1 Therapy

Date: [Date]

To: [HRA Administrator Name / Attn: Reimbursement Review]

Re: Patient [Full Name], DOB [Date of Birth]

I am the prescribing provider for the above patient and am submitting this letter in support of their reimbursement claim for [Medication Name and Strength — e.g., Wegovy 2.4 mg weekly subcutaneous injection].

Diagnosis: [Primary diagnosis with ICD-10 code — e.g., Obesity, E66.9]

Additional relevant diagnoses: [List with ICD-10 codes]

BMI (if relevant): [Number]

Treatment plan: The patient has been prescribed [Medication] as a medically necessary treatment for the above diagnosis.

Clinical rationale: [Reference the FDA-approved indication and the patient's documented diagnosis. Do not include language implying FDA review, generic equivalence, or "same active ingredient" for compounded products.]

Duration: This medication is expected to be medically necessary for at least [duration], with ongoing clinical reassessment.

This expense qualifies as a medical care expense under IRC Section 213(d) as a prescribed medicine for the treatment of a diagnosed disease.

Signed,

[Provider Name, Credentials]

[NPI Number]

[Clinic / Practice Name]

[Phone] | [Email]

Want this LMN as a downloadable PDF and editable .docx?

The 60-second match quiz delivers both, along with a personalized HRA receipt checklist for your situation.

Direct HRA card vs reimbursement vs insurance-first: which payment path fits you?

Answer: There are four real ways to pay for GLP-1 treatment when an HRA is in the picture. The right path depends on your HRA plan, your provider, and how much administrative tolerance you have.

| Payment path | Pros | Cons | Best for |

|---|---|---|---|

| Direct HRA card at checkout | No upfront cash if approved; fastest workflow. | Card can process even when plan later denies; substantiation may still be required after the fact. | Plans with clearly defined direct-card rules + providers that accept HRA cards. |

| Pay and submit | Full control over documentation; cleanest paper trail. | Requires upfront cash. | Anyone unsure whether the card will be accepted, or whose admin requires manual review. |

| Insurance first, HRA for cost-share | Lowest total cost when insurance covers the medication. | Prior authorization required; denials common; slower. | FDA-approved branded GLP-1s when your insurance has GLP-1 coverage. |

| Cash-pay, no HRA | Fastest if you don't qualify; no admin friction. | Highest out-of-pocket cost; loses the HRA tax advantage. | When your plan excludes GLP-1s entirely. |

Which GLP-1 providers make HRA reimbursement easiest?

Last verified:Answer: The right provider depends on whether you want to swipe an HRA card directly, pay and submit for reimbursement, or use insurance first. We compare each below by what their public pages actually deliver — including the limitations. We checked each provider's public payment, FAQ, and pricing pages on April 24, 2026.

Sesame

Best for direct HRA card payment

A telehealth marketplace where you can choose your own provider for a GLP-1 evaluation and pay directly with HRA, FSA, or HSA funds at checkout. Sesame's public payment page states users can pay with HSA, FSA, HRA, or other health-account funds at checkout, and that itemized bills are available for reimbursement (Source: Sesame Care payment page, verified April 24, 2026).

Why this matters: Sesame is the only major GLP-1 telehealth path we verified with explicit HRA card language at checkout. If your plan permits direct-card medical purchases, Sesame is the lowest-friction way to use HRA dollars without the pay-and-submit step.

Honest tradeoff: Sesame doesn't accept health insurance. If you were hoping insurance would cover most of the medication cost, Sesame is not your fit. But because Sesame skips insurance, they offer transparent self-pay pricing and let you use your HRA card directly at checkout. Confirm with your HRA administrator that direct-card medical purchases are allowed under your plan before relying on this path.

Check Sesame's HRA-friendly checkoutRo

Best for FDA-approved brands and insurance-coordinated HRAs

Ro Body — built around FDA-approved GLP-1 medications including Foundayo, Wegovy pill, Wegovy pen, Zepbound pen, and Zepbound KwikPen. They run a free GLP-1 Insurance Coverage Checker and include an insurance concierge that handles prior authorization. Ro Body pricing: $39 for the first month, then as low as $74/month with the annual plan paid upfront ($149/month otherwise).

Why this matters: Ro publicly states it does not accept HSA/FSA cards directly at checkout, but users may submit a detailed receipt after purchase for reimbursement (Source: Ro pricing FAQ, verified April 24, 2026). For HRAs that reimburse after purchase — which is most of them — that's the workflow that actually applies anyway.

Honest tradeoff: Ro doesn't accept HSA/FSA cards directly at checkout, which can feel like a hassle if you wanted to swipe and go. But they provide detailed receipts for HRA reimbursement and offer the free Insurance Coverage Checker plus prior-auth handling — meaning more people get insurance coverage and lower long-term costs through Ro than through providers that skip insurance entirely.

See FDA-approved GLP-1 options on RoEmbody

Best for cash-pay and needle-free gum options

Embody offers cash-pay compounded semaglutide and tirzepatide with a starting price of $99 for the first month of injections. They are a standout choice for patients seeking a needle-free GLP-1 gum option. If your HRA reimburses for compounded medications and you pay out of pocket, Embody provides itemized receipts for your reimbursement claim.

Honest caveat: Embody does not accept insurance and their shipped medications are compounded, not FDA-approved finished drugs. While they advertise HSA/FSA acceptance, you should treat them as a "pay first, submit to HRA later" option and confirm with your administrator that compounded GLP-1s are covered under your specific plan.

Check Embody EligibilityMEDVi — regulatory disclosure required

MEDVi offers one of the deepest GLP-1 menus in telehealth, including injectable and oral compounded options, with HSA/FSA-approved language and starting prices among the lowest in the market.

Required disclosure

On February 20, 2026, the FDA issued warning letter #721455 to MEDVi, citing false or misleading marketing claims regarding compounded semaglutide and tirzepatide. The FDA found that website language falsely suggested MEDVi was the compounder, and that claims like "Same active ingredient as Wegovy® and Ozempic®" implied FDA approval of compounded products. Important context: the FDA issued similar warning letters to more than 30 telehealth companies in early 2026 — this was an industry-wide enforcement action. The warning letter addressed MEDVi's marketing language, not the safety of the medications themselves. Until corrective status is publicly verified, we do not feature MEDVi as a top recommendation.

If you want to evaluate MEDVi yourself, verify their current website language, pricing, and pharmacy partners directly before purchasing. Embody (low-cost compounded starter options) and Ro (FDA-approved brands with insurance support) are cleaner paths for HRA reimbursement.

Hims and Hers

For mainstream brand-name HRA reimbursement

Following the March 2026 Novo Nordisk partnership, Hims and Hers offer broad access to FDA-approved Wegovy pill, Wegovy pen, and Ozempic. They're a reasonable fit if you want a familiar mainstream telehealth brand and your HRA reimburses FDA-approved medications. Confirm direct-card acceptance with your administrator before relying on it.

Provider summary

| Provider | Verified payment language | Direct HRA card at checkout | Best for |

|---|---|---|---|

| Sesame | HRA, HSA, FSA at checkout (verified) | Yes — strongest verified evidence | Direct-card HRA users with no insurance |

| Ro | No HSA/FSA cards; itemized receipts available (verified) | No — pay and submit | FDA-approved brands + insurance-coordinated HRAs |

| Embody | Low-cost compounded GLP-1 (injections/gum) | Confirm with admin | Patients seeking low starting price or GLP-1 gum |

| MEDVi | HSA/FSA approved (verified); current FDA warning letter disclosed above | Confirm with admin | Self-evaluate after reading the disclosure |

| Hims / Hers | Mainstream FDA-approved brand access | Confirm with admin | Mainstream brand-name reimbursement |

| All payment policies verified on April 24, 2026 against publicly available provider pages. Provider terms can change — verify on each provider's site before purchasing. | |||

HSA vs FSA vs HRA for GLP-1s — what's actually different

Answer: All three accounts follow IRS Section 213(d) for medical-expense rules, so the medication-level eligibility is similar across the three. The differences are in funding, ownership, contribution limits, carryover rules, and how much control your employer has over what's reimbursed. HRAs are the most plan-specific because the employer funds them and writes the rules; HSAs are the most portable because they're yours; FSAs are the most "use it or lose it."

| Feature | HSA | FSA | HRA |

|---|---|---|---|

| Funded by | Employee + optional employer | Employee pre-tax payroll | Employer only |

| Portable when you leave | Yes — it's yours | No | No (employer keeps it) |

| 2026 contribution cap | $4,400 self / $8,750 family | $3,400 | No federal cap (QSEHRA: $6,450 / $13,100; EBHRA: $2,200) |

| Carryover | Unlimited rollover | Up to $680 for 2026 if plan allows | Employer's discretion |

| Plan-document restrictions | Minimal | Administrator-set | Full employer control |

| Typical GLP-1 posture | Eligible with prescription | Eligible with prescription, often LMN | Eligible with prescription — but employer can exclude |

| 2026 limits sourced from IRS Rev. Proc. 2025-32, IRS Publication 15-B 2026, IRS HSA inflation guidance, and IRS guidance on EBHRAs. | |||

HRA can affect HSA eligibility

This is the most-missed gotcha. If you're enrolled in a high-deductible health plan and contributing to an HSA, certain HRA designs can disqualify you from making HSA contributions unless the HRA is structured as limited-purpose, post-deductible, suspended, or otherwise HSA-compatible (Source: IRS Publication 969). Talk to your benefits team before stacking accounts.

You can't double-dip

If your HRA reimburses an expense, you can't also deduct that same expense as a medical expense on your tax return (Source: IRS FAQ on medical expenses, nutrition, wellness, and general health). Most employees use the HRA first because it's the employer's money, then HSA/FSA for what the HRA didn't cover.

For a deeper comparison of GLP-1 providers that accept HSA/FSA cards specifically, see our GLP-1 Providers That Accept HSA/FSA Cards guide.

The exact email to send your HRA administrator

Answer: The single most effective thing you can do before paying for a GLP-1 is send your HRA administrator a short, specific email. Don't ask "are GLP-1s eligible?" — that gets you a generic answer. Ask whether your specific medication, prescribed for your specific indication, will be reimbursed under your specific plan if you provide specific documentation. Get the answer in writing.

Copy this email before you spend a dollar

Subject: HRA reimbursement question — prescribed GLP-1 medication

Hi [Administrator name or team],

I'm considering a prescribed GLP-1 medication ([Medication name — e.g., Wegovy 2.4 mg]) through [provider or pharmacy]. Before paying, I want to confirm whether my HRA will reimburse this expense under my plan.

Could you confirm in writing:

- Whether prescription GLP-1 medications are reimbursable under my HRA.

- Whether prescriptions for weight management or obesity treatment are excluded.

- Whether I need a Letter of Medical Necessity, diagnosis code, or other documentation submitted with the claim.

- Whether I can use my HRA debit card directly at checkout, or whether I should pay out of pocket and submit a reimbursement claim.

- What an itemized receipt must include for substantiation.

- Whether telehealth visit fees, lab work, and program subscription costs are treated separately from the medication itself.

Thank you — I'd appreciate the written response so I can keep it on file.

Best,

[Your name]

[Plan ID or member number]

If they call you back instead of replying in writing, ask them to follow up by email summarizing what they said. If they refuse to confirm in writing, that's information too — default to pay-and-submit and keep every receipt.

What to do if your HRA GLP-1 claim gets denied

Answer: A denied HRA claim isn't always final. Many denials are either documentation problems or plan-exclusion problems, and documentation problems are usually fixable. Get the denial reason in writing, compare it to your plan document, identify whether the issue is documentation or exclusion, and then either resubmit with additional paperwork, file an internal appeal, or switch to a different payment path.

The 5-step denial workflow

- 1Get the specific denial reason in writing. "Denied" is not enough. You need the code or explanation: missing receipt, missing LMN, plan exclusion, non-covered category, etc.

- 2Compare it to your plan document. Pull the SPD or HRA plan document and find the section that matches the denial reason.

- 3Identify whether it's documentation or exclusion. Documentation problem: missing or insufficient paperwork → fixable. Plan exclusion: the plan genuinely doesn't cover this → not fixable through this account, but you may have alternative paths.

- 4Resubmit or appeal. For documentation problems, gather the missing items and resubmit. For exclusions you believe are wrong, most plans have an internal appeal process spelled out in the plan document.

- 5Switch payment paths if needed. If the exclusion is real, route to FSA/HSA, insurance, or cash-pay rather than fighting a losing battle.

The 8 most common GLP-1 HRA denial reasons and the fix

| Denial reason | Why it happens | Fix |

|---|---|---|

| 1. No diagnosis on record | Prescription written without a documented medical condition in the chart | Ask your provider to update the chart with the appropriate ICD-10 (E66 for obesity, E11 for T2D, etc.) and resubmit. |

| 2. Plan excludes weight-loss drugs | Employer carved out GLP-1s for weight loss | If the medication was prescribed for diabetes or another covered diagnosis, ask the clinician how to submit documentation that accurately matches your medical record. If not, route to cash-pay or alternative account. |

| 3. Missing Letter of Medical Necessity | Admin's GLP-1 policy requires LMN for weight-loss use | Use the template above, get it signed, resubmit. |

| 4. Itemized receipt lacks medication line | Telehealth invoice bundled "program fee" with medication | Request an accurate itemized receipt that names the medication and matches the medical record. |

| 5. Receipt shows "wellness" or "weight management program" only | Admin reads this as non-qualifying general health | Ask the provider for a corrected receipt that names the medication or service accurately. |

| 6. HRA blocks first-dollar drug reimbursement under HDHP | You're enrolled in HDHP+HSA, and the HRA isn't post-deductible structured | Pay out of pocket until deductible met; reimburse afterward; or restructure HRA at next open enrollment. |

| 7. Compounded product not recognized | Some administrators flag compounded GLP-1s after FDA April 2026 guidance | Provide the 503A pharmacy's dispensing documentation and prescriber's medical justification — or switch to FDA-approved brand. |

| 8. Submission outside plan deadline | HRA claim deadlines vary by plan | Submit within your plan's deadline; a 30-day internal target is a practical habit. |

If your employer excludes weight-loss GLP-1s, see our GLP-1 Providers That Accept HSA/FSA Cards guide for cash-pay options that don't require HRA approval.

What if your employer just removed GLP-1 coverage or created a separate GLP-1 HRA?

Answer: A growing number of employers are restructuring how they cover GLP-1s — narrowing existing coverage, capping reimbursement, requiring participation in a coaching program, or carving GLP-1 spending out of the medical plan entirely into a specialty HRA. GLP-1 spending is one of the largest line items in employer health budgets right now. According to the Peterson-KFF Health System Tracker, in 2025, 19% of large firms (200+ workers) and 43% of firms with 5,000+ workers covered GLP-1s for weight loss in their largest health plan.

Employers are responding three ways:

- Narrowing the medical plan — adding BMI thresholds, requiring participation in a weight-management program, putting GLP-1s in a higher pharmacy tier, or excluding weight-loss use entirely.

- Carving GLP-1 spending into a specialty HRA — separating the medication from the medical plan with its own monthly cap and program requirements.

- Eliminating coverage with no replacement — and pointing employees toward direct-to-consumer pricing (NovoCare, LillyDirect, Ro, etc.).

If your coverage was eliminated entirely

Don't fight the plan you can't win. Pivot.

How much can an HRA actually save you on GLP-1 treatment?

Answer: An HRA doesn't lower the sticker price of GLP-1 treatment — it reimburses eligible expenses up to your available HRA balance or your plan's reimbursement cap. The HRA's value is the tax advantage and the offset to out-of-pocket cost, not a discount at checkout.

Realistic math (illustrative only)

| Monthly GLP-1 cost | Monthly HRA reimbursement | Remaining out-of-pocket |

|---|---|---|

| $299 (typical compounded refill) | $299 (full coverage) | $0 |

| $499 (FDA-approved program with concierge) | $300 (capped) | $199 |

| $1,089 (Zepbound list price reference) | $500 (capped) | $589 |

| $1,349 (Wegovy list price reference) | $200 (specialty HRA cap) | $1,149 |

| Illustrative only. Verify your plan's actual reimbursement cap, your provider's actual current price, and the specific eligible-expense definition before relying on these numbers. | ||

Don't think of an HRA as a coupon. Think of it as an offset against what you'd otherwise pay in after-tax dollars. A $200/month HRA reimbursement on a $499 GLP-1 program is roughly equivalent to a $260–$280 pretax raise depending on your tax bracket — meaningful, but not the whole cost.

Your action plan: what to do this week

Answer: Don't pay for a GLP-1 with HRA dollars until you've confirmed the expense is reimbursable, gathered the documentation you'll need, and chosen the right payment path for your plan. The full sequence takes about 30 minutes of work upfront and saves you from the much more painful process of fighting a denial later.

Identify your HRA type

Check your benefits portal or ask HR: integrated/GCHRA, ICHRA, QSEHRA, EBHRA, or specialty GLP-1 HRA?

Send the email above to your HRA administrator

Get written confirmation about your specific medication, indication, and documentation requirements.

Get your prescription with the diagnosis on record

Ask your provider explicitly: "Please document the diagnosis and medical necessity in my chart with the appropriate ICD-10 code."

Choose your payment path

Direct HRA card at checkout → Sesame (verified HRA acceptance). FDA-approved brand + insurance support → Ro. Cash-pay reimbursement → Embody (low-cost starter pricing). Compounded path → only if your plan covers compounded; verify provider regulatory standing first.

Submit promptly with full documentation

Submit within your plan's deadline. Keep digital copies for at least 3 years.

Final decision table

| Your situation | Best next step |

|---|---|

| "My HRA card can be used at checkout" | Verify plan rules in writing, then Sesame. |

| "I want FDA-approved branded medication and insurance help" | Ro. |

| "I'm paying cash and reimbursing through my HRA later" | Embody. |

| "My employer excludes weight-loss GLP-1s" | Don't force the card. Use FSA/HSA, cash-pay, or direct-from-manufacturer instead. |

| "I have no idea which applies to me" | Take the matching quiz. |

Still figuring out which provider, payment path, and documentation fits your specific HRA?

Our free 60-second matching quiz asks about your plan type, your medication, your prescribing reason, and your provider preferences, then routes you to the lowest-friction GLP-1 path with a personalized documentation checklist.

What we actually verified for this guide

Verified directly from primary sources — April 24, 2026

- IRS Publication 502 (2025) — medical expense definitions

- IRS Publication 969 (2025) — HRA structure, HSA interactions

- IRS Publication 15-B (2026) — QSEHRA limits

- IRS Rev. Proc. 2025-32 — 2026 FSA limit ($3,400) and carryover ($680)

- 2026 HSA limits ($4,400 self / $8,750 family) and EBHRA limit ($2,200)

- FDA April 1, 2026 compounding policy clarification

- FDA shortage status — semaglutide (Feb 2025), tirzepatide (Dec 2024)

- FDA approval of Foundayo (orforglipron), April 1, 2026

- FDA Warning Letter #721455 to MEDVi, February 20, 2026

- VEHI member notice on HRA and GLP-1 weight-loss medications (January 2026)

- Sesame Care payment page — verified HRA, HSA, FSA at checkout language

- Ro pricing FAQ — verified receipt-submission policy

What still needs your individual confirmation

- Whether your specific employer's HRA plan excludes weight-loss medications

- Whether your HRA administrator requires a Letter of Medical Necessity for your prescription

- Whether your plan allows direct HRA card payment, pay-and-submit, or both

- Current pricing on Ro, Embody, Sesame, MEDVi, Hims, and Hers — verify on each provider's site before purchasing

- Your specific provider's current HRA, HSA, and FSA acceptance — these can change

Industry analyses from Alliant Compliance Insights, NFP, Akerman LLP, Ogletree Deakins, Mercer, Foley & Lardner, Benepass, Peterson-KFF Health System Tracker, SHRM, and International Foundation of Employee Benefit Plans. If you spot something we got wrong, email us. We update this page when source documents change.

Frequently asked questions

Sources cited in this guide

- IRS Publication 502 (2025), Medical and Dental Expenses — irs.gov/publications/p502

- IRS Publication 969 (2025), Health Savings Accounts and Other Tax-Favored Health Plans — irs.gov/publications/p969

- IRS Publication 15-B (2026), Employer's Tax Guide to Fringe Benefits — irs.gov/publications/p15b

- IRS Topic No. 502, Medical and Dental Expenses — irs.gov/taxtopics/tc502

- IRS, Frequently asked questions about medical expenses related to nutrition, wellness and general health

- IRS Rev. Proc. 2025-32 (2026 FSA limits and carryover)

- IRS, 2026 inflation adjustments announcement (FSA carryover $680, FSA limit $3,400)

- FDA, FDA clarifies policies for compounders as national GLP-1 supply begins to stabilize

- FDA, April 1, 2026 clarification on 503A and 503B compounding policies

- FDA Warning Letter #721455 to MEDVi, LLC, dated February 20, 2026

- FDA approval announcement for Foundayo (orforglipron), April 1, 2026

- Vermont Education Health Initiative member notice on HRA and GLP-1 weight-loss medications, January 2026

- Alliant Compliance Insights, GLP-1 Cost Containment Strategies

- NFP, GLP-1 Discrimination Considerations for Employer Plans

- Akerman LLP, GLP-1s and Employer Health Plans (February 2026)

- Ogletree Deakins, Employers Grapple With GLP-1 Coverage for Weight Loss

- Mercer, GLP-1 considerations for 2026

- Foley & Lardner, FDA Clarifies Policies for Pharmacy Compounders of GLP-1 Products (April 2026)

- Peterson-KFF Health System Tracker, employer GLP-1 coverage data

- Benepass, Tame GLP-1 Costs With Specialty HRAs

- International Foundation of Employee Benefit Plans, GLP-1 coverage trend data

- Sesame Care payment page (verified April 24, 2026)

- Ro pricing FAQ (verified April 24, 2026)

Still not sure which GLP-1 program is right for you?

Take our free 60-second matching quiz and we'll route you to the right provider, the right payment path, and the right documentation for your specific HRA setup.

Start the free 60-second quizWeight Loss Provider Guide is an independent comparison resource for GLP-1 telehealth providers. This page contains affiliate links — if you purchase through them, we may earn a commission at no cost to you. We recommend providers based on verified payment policies, documentation quality, and fit for the reader, not commission rates. Affiliate disclosure: Sesame, Ro, Embody, Hims, and Hers are partners. This guide is informational and does not replace advice from your clinician, tax advisor, or HRA plan administrator. Last verified: .