Does Hims Accept HSA/FSA for Weight Loss? What Qualifies, What Doesn’t, and How It Really Works

Weight Loss Provider Guide is an independent comparison resource for GLP-1 telehealth providers. Some links on this page are affiliate links — if you enroll through them, we may earn a commission at no extra cost to you. This does not affect our editorial process. For informational purposes only — not medical, tax, or legal advice.

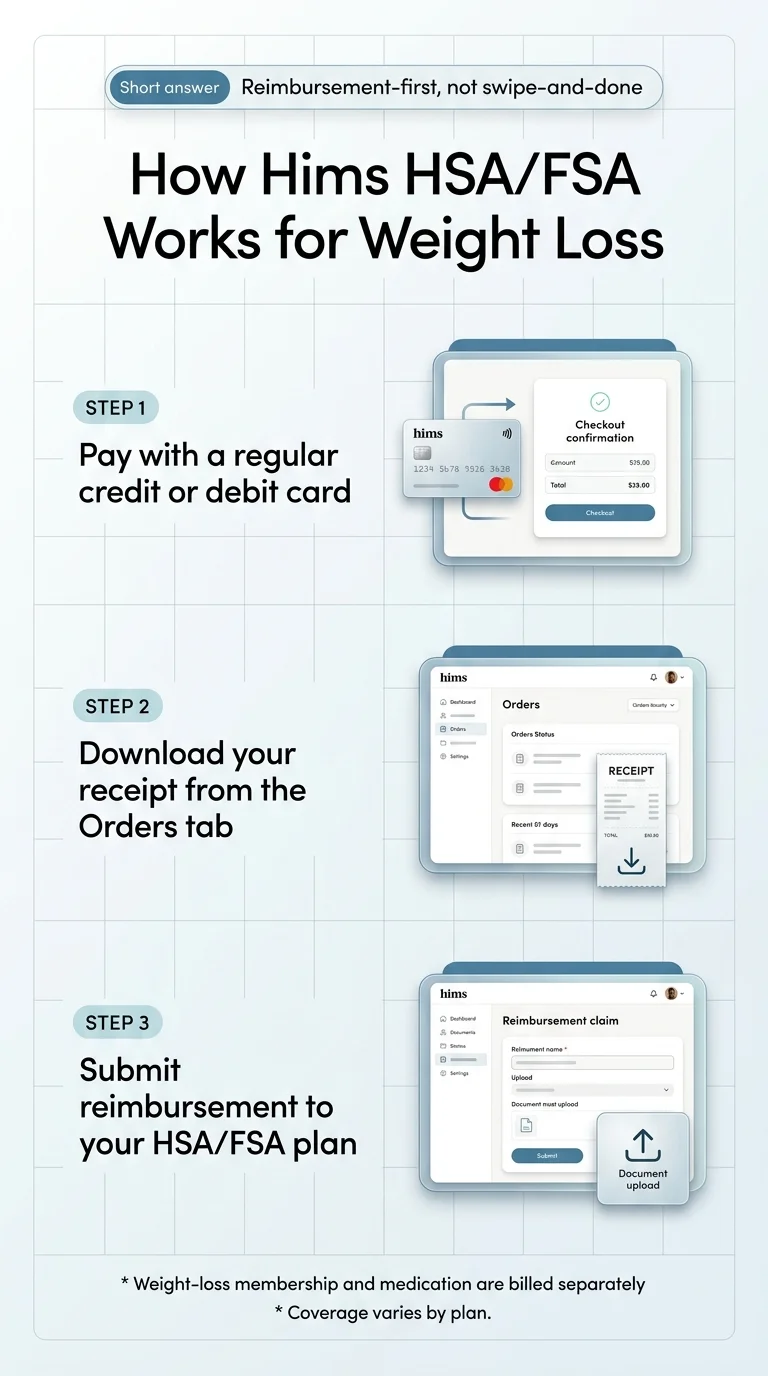

Short answer: Yes — Weight Loss by Hims is HSA/FSA eligible, but Hims doesn't accept HSA/FSA cards the way a pharmacy counter does.

Hims explicitly recommends paying with a regular credit or debit card and then submitting the receipt to your plan for reimbursement (source: hims.com/weight-loss/fsa-hsa). That one distinction is where most shoppers get tripped up — and it’s why this question keeps coming back.

Other Hims categories aren’t universally covered either — Hims Labs and the Hims enclomiphene program both publicly state HSA/FSA isn’t currently accepted for those products.

Quick verdict (what we found)

| Your situation | What actually happens | Next step |

|---|---|---|

| Want Weight Loss by Hims and fine with reimbursement | Pay with a regular card, pull the receipt from the Orders tab, submit to your plan. Hims confirms the weight-loss medication kit is eligible for HSA/FSA reimbursement. | See current Hims weight-loss plans → |

| Want to swipe your HSA/FSA card directly at checkout | Hims doesn’t treat HSA/FSA cards as a frictionless payment method — the card may flag for extra steps or decline. | See providers that accept HSA/FSA cards directly → |

| Looking at Hims Labs or enclomiphene | Not currently HSA/FSA eligible at Hims (both confirmed by Hims’s own pages). | Out of scope here. |

| Looking at Hims ED, hair, mental health | Mixed — Hims’s own ED content says HSA/FSA funds may apply when eligible. Confirm with your plan. | Not the focus of this page. |

What we actually verified (April 16, 2026)

We read Hims’s own HSA/FSA page, support article, weight-loss FAQ, weight-loss main page, drug-pricing page, Wegovy Pen page, dedicated Wegovy page, Hims Terms, the Hims Labs FAQ, and the Hims enclomiphene content. We cross-checked against IRS Publication 502, IRS Publication 969, and IRS Notice 2026-05 for 2026 HSA limits, plus FSAFEDS documentation for reimbursement procedures. We used Reddit and Trustpilot only to understand how real shoppers describe the reimbursement process — never as primary evidence.

Does Hims accept HSA/FSA for weight loss?

Yes — Weight Loss by Hims is eligible for HSA and FSA reimbursement, and Hims markets the program that way openly.

Here’s the literal instruction from Hims: they recommend using a valid credit or debit card and submitting reimbursement. They note that if you try paying with an FSA/HSA card, your provider may reach out to request a receipt before processing the payment (source: support.hims.com). Translation: it’s a reimbursement workflow, not a swipe-and-done workflow.

That distinction matters because people often see the word “eligible” and expect their FSA debit card to work like it does at CVS. It often doesn’t — and it has nothing to do with Hims being shady and everything to do with how FSA/HSA cards authorize online transactions. We’ll explain the workaround next, then show you exactly how to run the reimbursement without surprises.

Two conditions that change this answer

- Your plan’s specific documentation rules. HSA/FSA coverage varies by plan administrator. Most plans approve Hims weight-loss reimbursement when you submit a detailed receipt plus (when they ask) a Letter of Medical Necessity. A few will want more.

- Whether the prescription is written to treat a diagnosed condition. Under IRS Publication 502, weight-loss expenses qualify only when prescribed to treat a specific disease diagnosed by a physician — examples listed by the IRS include obesity, hypertension, and heart disease. The specific BMI thresholds you see cited online (BMI ≥ 30 alone, or ≥ 27 with a weight-related comorbidity) aren’t from Pub 502 — those are the FDA-approved clinical eligibility criteria for medications like Wegovy and Zepbound. Both layers matter, and they’re different.

If you’re fine handling a reimbursement claim in exchange for pre-tax savings, Hims’s weight-loss medication pricing starts at $149/month for the Wegovy® Pill — with the Weight Loss Membership billed separately at $39 for the first month, then $149/month ongoing.

Check Hims weight-loss eligibility and current pricingDirect card vs. reimbursement — what actually happens at checkout

Hims is a reimbursement-first experience.

This is why Hims tells you to pay with a regular card and file for reimbursement. You use a personal credit or debit card, download your receipt from the Orders tab, and submit it through your HSA or FSA plan’s portal. The tax savings are identical either way. The paperwork is the cost of buying online from a telehealth platform instead of at a retail pharmacy.

Here’s what that looks like in practice:

- Best case at checkout: FSA card processes. Hims may still email asking for a receipt. You pull it from Orders, send it over, done.

- Middle case: Card is held pending documentation. You send the receipt; it releases.

- Worst case: Card declines. You switch to a regular card, complete the purchase, and file reimbursement the standard way.

A declined HSA/FSA card at Hims is not a sign the expense is ineligible or that something is wrong with you. It’s a merchant-system quirk of online medical commerce. The fix is two extra minutes of paperwork.

Start Hims with a personal credit or debit card, then file reimbursement from day one.

Begin your Hims weight-loss eligibility checkYour Hims product-line HSA/FSA matrix

Hims HSA/FSA Verification Matrix

| Hims product | HSA/FSA status (per Hims) | How it works | What to know |

|---|---|---|---|

| Weight Loss by Hims — GLP-1 kit | Eligible for reimbursement | Pay with a regular card, download receipt from Orders tab, submit to your plan | Coverage varies by plan; GLP-1s aren’t yet available in all 50 states |

| Weight Loss Membership fee | Billed separately from medication; plan-dependent for reimbursement | Administrators treat this differently — some approve it as part of the medical program, some don’t | The medication line is the cleanest reimbursement claim; confirm the membership fee with your administrator before assuming it’s covered |

| Wegovy® Pen through Hims | Labeled “FSA & HSA eligible” on the product page | Same reimbursement flow | Listed from $199/month billed monthly; Weight Loss Membership required |

| Dedicated Wegovy® page | Reimbursable through HSA/FSA per Hims | 6-month prepay model | Pricing currently inconsistent across Hims’s own pages — see note below |

| Hims Labs | Not accepted | Hims Labs FAQ explicitly states HSA and FSA plans aren’t accepted as payment for Labs at this time | Pay with a regular card; no reimbursement pathway advertised |

| Enclomiphene (men’s hormone health) | Not currently accepted | Hims’s own enclomiphene content | Different category, different rule |

| Hims ED | Mixed — Hims’s own ED content notes HSA/FSA funds may apply to eligible ED treatments | Confirm with your plan administrator | ED treatment can qualify under Pub 502 as treatment of a diagnosed condition; confirm before assuming |

| Hair loss, skin, mental health | Category-dependent; not actively marketed as HSA/FSA-eligible like weight loss | Check with your administrator for anything tied to a diagnosed condition | Not the primary lane Hims markets around HSA/FSA |

A real pricing inconsistency worth flagging

Why this matters for shoppers. If you’re coming to Hims for weight loss, you’re in the covered lane. If you were hoping to bundle other Hims subscriptions into the same HSA/FSA claim, check your specific product — some qualify when prescribed for a diagnosed condition and some don’t. HSA/FSA dollars are for treating diagnosed medical conditions, not for elective or cosmetic care. The weight-loss program is the category Hims has specifically built around HSA/FSA reimbursement.

What does Hims weight loss actually cost before any HSA/FSA savings?

Hims separates the Weight Loss Membership fee from the medication price.

Here’s what the real published monthly outlay looks like on the main weight-loss pages — before any HSA/FSA reimbursement, just the sticker price shoppers actually see.

Real published Hims cost math (editorial calculations based on Hims’s stated prices, verified April 16, 2026)

| Medication option | Medication (per Hims) | + Weight Loss Membership | First month total | Ongoing monthly total |

|---|---|---|---|---|

| Wegovy® Pill | from $149/mo | $39 first / $149 ongoing | $188 | $298 |

| Wegovy® Pen | from $199/mo | $39 / $149 | $238 | $348 |

| Ozempic® | from $199/mo | $39 / $149 | $238 | $348 |

| Generic liraglutide | from $299/mo | $39 / $149 | $338 | $448 |

| Mounjaro® / Zepbound® | $1,899/mo | $39 / $149 | $1,938 | $2,048 |

A few things to read between these lines:

The prepay bundles may look different. Hims also publishes prepay structures — oral medication kits starting at $69/month with a 10-month plan paid up front, and GLP-1 injectable plans starting at $199/month with a 6-month plan paid in full up front. In prepay bundles, the membership-vs-medication structure can be bundled differently. Verify the exact line items on your checkout screen, because what’s billed as a single prepay sum is easier to reimburse cleanly than two recurring charges.

Brand-name tirzepatide has cheaper cash-pay alternatives elsewhere. Hims currently lists Mounjaro and Zepbound at $1,899/month. If that number makes you wince, Eli Lilly’s direct cash-pay program (LillyDirect) offers Zepbound self-pay vials at lower price points than many telehealth markups. Check Lilly’s direct pricing if a brand-name tirzepatide is what you specifically want — Hims isn’t where you’ll get the cheapest Zepbound.

The membership fee is the thing people miss. Most shoppers underestimate their monthly Hims outlay by exactly $149. Now you won’t.

Budget checked. If $298/month (Wegovy Pill + Membership) works with your HSA/FSA balance, you’re ready to move.

See if Hims is a match for your budget and stateThe Hims HSA/FSA reimbursement playbook

Before you sign up

- Check your HSA or FSA balance through your administrator’s app or portal. Know what’s available.

- Ask your administrator two questions:

- Do you require a Letter of Medical Necessity for weight-loss prescriptions?

- What format do you want receipts in — PDF, itemized, with prescribing provider name?

- Decide who will write your LMN if one is required. Options include your Hims prescribing provider or your regular primary care doctor if you’ve discussed weight with them before.

At checkout

- Use your regular credit or debit card. This is what Hims recommends.

- Save the order confirmation email. It’s not enough by itself for reimbursement, but you’ll want it as a reference.

Within 24 hours of your first order

- Download your itemized receipt. Log into your Hims account → Orders tab → find the most recent order → download the receipt. Hims directs customers to this exact path (source: hims.com/weight-loss/fsa-hsa).

- If your plan requires an LMN, message your prescribing provider through the Hims secure portal and ask. Hims doesn’t publicly commit to an LMN turnaround in its support documentation, so ask early rather than late. A suggested script:

“My HSA/FSA plan administrator requires a Letter of Medical Necessity for my prescribed GLP-1 weight-loss treatment. Could you provide one that includes my diagnosis code, the medication and dosage, and the expected treatment duration? Thank you.”

Submit your claim

- Log into your HSA or FSA plan’s portal (HealthEquity, Fidelity, Optum, WageWorks, Navia — whoever administers yours).

- Upload your documentation: the itemized Hims receipt, plus the LMN if your plan asked for one.

- Submit. FSAFEDS (the federal employee FSA program) states that most of its claims are processed within 1–2 business days after they’re received and verified. Private-sector administrators vary — ask yours for their standard turnaround.

If your first claim is denied

Don’t panic. Most denials are procedural and fixable with one resubmit. We cover the three most common failure reasons in What can kill your claim below.

The HSA-specific shortcut almost nobody uses

HSAs have no deadline for reimbursement. If you pay for Hims out of pocket now and keep the receipts, you can reimburse yourself from your HSA years later — this is legitimate IRS-blessed behavior per IRS Publication 969. Some people treat their HSA as a long-term investment vehicle and only reimburse past medical expenses when they need the cash.

FSAs don’t work this way. FSA claims generally need to be submitted within your plan year (or a brief grace period or carryover window). If you’re on an FSA, don’t wait.

Letter of Medical Necessity for Hims — when you need one

What a strong LMN typically contains

Based on FSAFEDS documentation and common administrator requirements, an LMN for weight-loss treatment generally includes:

- Patient name and date of birth

- The diagnosed medical condition being treated — commonly obesity, or type 2 diabetes, or a hypertension-related indication

- A statement that the prescribed treatment is medically necessary to treat that condition, not cosmetic or general wellness

- The specific medication or program prescribed

- The expected duration of treatment

- Signature and date from the prescribing provider

LMNs generally need to be renewed when the prior treatment period expires (FSAFEDS requires a new LMN after the expiration of the previous one). Set a calendar reminder for the renewal point.

If your plan asks for an LMN and you don’t have one yet

Your options:

- Message your Hims prescribing provider through the secure portal and ask. Hims doesn’t publicly guarantee LMN issuance in its support documentation, so if the first response misses the request, follow up.

- Get the LMN from your primary care doctor or an in-person provider you’ve seen for weight concerns. A PCP can write an LMN for a diagnosis they’ve already documented, even if Hims is the one writing the prescription.

- Escalate through Hims support by explicitly citing the HSA/FSA requirement.

What you’ll actually save — HSA/FSA tax math by bracket

Estimated annual savings on Hims Wegovy Pill ($298/month = $3,576/year)

| Your federal tax bracket | Estimated federal tax savings | + Payroll FICA savings (7.65%) | Total annual savings |

|---|---|---|---|

| 12% | ~$429 | ~$274 | ~$703 |

| 22% | ~$787 | ~$274 | ~$1,061 |

| 24% | ~$858 | ~$274 | ~$1,132 |

| 32% | ~$1,144 | ~$274 | ~$1,418 |

| 37% | ~$1,323 | ~$274 | ~$1,597 |

State tax savings stack on top of this if your state also exempts HSA/FSA contributions (most do). California and New Jersey are the notable exceptions for HSAs — they tax HSA contributions at the state level even though the federal code doesn’t.

This is general information, not tax advice. Your actual savings depend on your specific tax situation — confirm with your tax advisor.

HSA vs FSA — which one actually fits ongoing GLP-1 use?

This is a real decision for anyone planning to stay on a GLP-1 long term.

HSA works better if you:

- Are enrolled in a high-deductible health plan (HDHP)

- Want the money to roll over indefinitely

- Like the idea of investing contributions long-term (triple tax-advantaged)

- May switch jobs (HSAs are portable; FSAs generally aren’t)

- Want the “reimburse yourself years later” flexibility

- 2026 contribution limits per IRS Notice 2026-05: $4,400 self-only / $8,750 family, plus a $1,000 catch-up if you’re 55+

FSA works better if you:

- Already have a balance from your employer

- Are close to the plan-year deadline

- Don’t qualify for an HDHP/HSA

- Want to contribute without changing your health insurance

- 2026 FSA carryover maximum: up to $680 for plans that allow carryover (per IRS inflation adjustments for 2026)

For ongoing GLP-1 use: HSA.

What can kill your HSA/FSA claim — and how to rescue it

Failure #1 — Receipt shows “wellness program” instead of the medication

This is a common denial reason for telehealth weight-loss claims. Your plan sees a vague line item and flags it. The fix: contact Hims support and request an itemized receipt that breaks out the medication name, dosage, prescribing provider, and date of service as a separate line.

Rescue script for Hims support:

“My HSA/FSA plan administrator declined my reimbursement claim because the receipt doesn’t itemize the medication separately from other program fees. Please send me an itemized receipt showing the medication name, dosage, prescribing provider, date of service, and amount as separate line items.”

FSAFEDS specifies that acceptable claim receipts should show the patient name, provider name, dates of service, type of service or product, and cost — a good standard to request regardless of which plan you’re with.

Failure #2 — Missing Letter of Medical Necessity

Your plan wrote back asking for an LMN and you don’t have one. Request one through Hims (see the LMN script above), wait for it, and resubmit. If Hims doesn’t respond, work with your primary care provider.

Failure #3 — You tried the HSA/FSA card, got a decline, and assumed you can’t use those funds

This mistake shows up in Reddit threads often. A card decline at online checkout is a merchant-system issue, not an IRS issue. Pay with a regular card, then file reimbursement the normal way. You’re not shut out.

Failure #4 — FSA plan year ended before you submitted

FSAs are use-it-or-lose-it. Most plans close December 31 with a limited carryover (up to $680 for 2026) or a short grace period into March 15, depending on how your employer set it up. If you have an expiring FSA balance and you’ve been thinking about GLP-1 treatment, the decision makes itself: start now, use the dollars, submit before the deadline.

FSAFEDS specifically notes that fees paid in advance of services being rendered aren’t eligible — so if you’re tempted to prepay six months of Hims in December purely to burn the balance, read your administrator’s fine print first. The service generally has to occur within the plan year.

The rescue table

| If your claim was denied for… | Likely fix | Resubmit timeline |

|---|---|---|

| Insufficient receipt detail | Request itemized receipt from Hims support | 1–3 days |

| No LMN on file | Request LMN from your Hims provider or PCP | Varies |

| Line items bundled as “wellness” | Ask Hims support to break out medication separately | 1–3 days |

| Card decline at checkout | Switch to regular card, pay, then file reimbursement | Immediate |

| FSA plan year closed | Check grace period; expired claims generally can’t be reopened | Not fixable |

The catches most pages bury

Hims doesn’t bill insurance for weight loss

Hims does not accept insurance for its weight-loss program (source: support.hims.com). You’re paying cash (or HSA/FSA reimbursement). If you have commercial insurance that actually covers Wegovy or Zepbound — a small but real percentage of plans do — and you want to use it, you need a provider that bills insurance directly. Hims isn’t that. Ro is a more natural fit for brand-name insurance-backed scripts if that’s your situation.

GLP-1s aren’t available in every state

Hims explicitly states GLP-1s aren’t yet available in all 50 states (source: hims.com/weight-loss/faq). Availability gets confirmed during intake — if you’re in an unsupported state, you’ll know before paying.

The membership and the medication renew on separate cycles

This is the sneakiest one. Hims’s terms make clear the Weight Loss Membership and the medication plan are separate billings. Canceling your medication plan does not automatically cancel your Weight Loss Membership (source: hims.com/terms-and-conditions). If you stop treatment but forget to cancel the membership, you can keep getting billed $149/month for a membership you’re not using. Cancel both, and cancel at least two days before the next renewal date per Hims’s terms.

Refund rules

Hims doesn’t generally refund shipped medication. Partially used periods typically aren’t prorated. Once it ships, it’s yours. Plan your timing accordingly — if you’re on the fence about a dose increase or want to wait a month, pause before the next order processes, not after.

Who should use Hims for HSA/FSA — and who shouldn’t

You’re a good fit for Hims if…

- You already trust the Hims brand and want that specific experience

- You want access to branded medications (Wegovy®, Zepbound®, Ozempic®, Mounjaro®, generic liraglutide)

- You’re willing to spend ~20 minutes a month on reimbursement paperwork in exchange for pre-tax savings

- You value the app, check-ins, and ongoing support

- You live in a state where Hims offers GLP-1 treatment

You’re not a good fit for Hims if…

- You want to swipe your HSA/FSA card at checkout and be done. Hims steers you to reimbursement.

- You specifically need insurance billing. Hims doesn’t accept insurance for weight loss.

- You live in a state where Hims doesn’t offer GLP-1s.

- You hate subscription billing and will resent the $149/month membership fee on top of medication.

The honest tradeoff — and what to do if it doesn’t work for you

You deserve an honest read before you click anything, so here’s the one flaw worth saying out loud. Hims is NOT the cleanest HSA/FSA checkout in the GLP-1 space. If direct card acceptance with no reimbursement paperwork is your top priority, a provider like MEDVi is a better fit — MEDVi’s own support page states HSA and FSA cards are accepted at checkout like a debit card, and MEDVi is listed on both the HSA Store and FSA Store through Health-E Commerce.

But because Hims does not offer direct-card HSA/FSA checkout, they can do something MEDVi can’t — offer you one of the broadest branded medication menus in telehealth, including Wegovy, Zepbound, Ozempic, Mounjaro, Wegovy Pen, Wegovy Pill, and generic liraglutide, all under one platform with a polished app and strong provider network. That’s the tradeoff: more paperwork for more medication choice.

If paperwork friction is the dealbreaker, route yourself to MEDVi or SkinnyRx below. If medication choice and brand trust matter more, Hims’s reimbursement flow is genuinely workable once you know the moves.

Ready to start? Hims weight-loss plans are live now.

Check Hims eligibility and state availabilityIf you’d rather skip the paperwork — providers to consider

| Provider | HSA/FSA at checkout | Starting price | Best for |

|---|---|---|---|

| MEDVi | ✅ Yes — MEDVi’s support page confirms HSA and FSA cards accepted at checkout like a debit card | $179/mo intro, $299/mo ongoing (compounded semaglutide) | Unused HSA/FSA balance, broad compounded menu, no paperwork |

| SkinnyRx | ✅ Published HSA/FSA eligibility guidance; FSA Store listed | From ~$199/mo | Oral GLP-1 or microdose intent, lower-friction checkout |

| Shed (LifeMD) | Listed on HSA Store and FSA Store; marketed as FSA-eligible on their site | Varies | Polished app experience; confirm direct-card behavior at checkout with their support before relying on it |

| Ro | ⚠️ Reimbursement-style model similar to Hims | $39 first month, then $149/mo (as low as $74/mo on annual plan paid upfront) | FDA-approved branded medications (Zepbound®, Foundayo™) |

Regulatory note on compounded medications

What real users say about the Hims HSA/FSA process

We’re including customer quotes for process and support expectations only — not for medical efficacy or safety claims. Results vary and individual experiences aren’t predictive.

On Hims support and consultation process (from Hims’s own published reviews):

“The consultation, ordering, check-ins, and customer service through the Hims app have all been very positive!” — Roland, 43, via Hims’s own published reviews. Hims notes customers may have been compensated and results are not independently verified.

On responsiveness (third-party Trustpilot review):

“Quick response times from actual people.”

On the reimbursement experience (third-party Trustpilot review):

“I wish it was easier to navigate the process for HSA reimbursement.”

That third quote captures the honest consumer read of Hims’s HSA/FSA workflow. It’s doable, it’s legitimate, it just takes a few extra minutes each month. If you go in expecting that, nothing about the process will feel like a surprise.

What we actually verified

This is our trust package. If you want to audit our work, here’s every source we pulled from on April 16, 2026.

Hims’s own pages

- HSA/FSA Weight Loss Medication page (hims.com/weight-loss/fsa-hsa)

- “Do you accept insurance?” support article (support.hims.com)

- Weight Loss FAQ (hims.com/weight-loss/faq)

- Weight Loss main page and drug-pricing page (hims.com/weight-loss, hims.com/weight-loss/drug-pricing)

- Wegovy Pen page (hims.com/weight-loss/wegovy-pen)

- Dedicated Wegovy page (hims.com/weight-loss/wegovy)

- Hims Terms (hims.com/terms-and-conditions)

- Hims Labs Frequently Asked Questions

- Hims enclomiphene content

- Hims ED content (for the ED reimbursement note)

IRS and HSA/FSA authority sources

- IRS Publication 502 (Medical and Dental Expenses)

- IRS Publication 969 (Health Savings Accounts and Other Tax-Favored Health Plans)

- IRS Notice 2026-05 for 2026 HSA contribution limits

- IRS tax inflation adjustments for 2026 (FSA carryover)

- FSAFEDS documentation on weight-loss program eligibility, LMN requirements, and claim procedures

- HSA Store and FSA Store eligibility listings (weight-loss programs)

FDA sources for compounded medication context

Competitor verification

- MEDVi official support page on HSA card acceptance

- MEDVi listings on HSA Store and FSA Store via Health-E Commerce

- Shed / LifeMD public pages and HSA/FSA Store listings

- SkinnyRx published HSA/FSA eligibility guide

- Ro published pricing page

What we used only for voice and friction signal (not as evidence)

- Reddit r/HIMS and r/HimsWeightloss threads on HSA/FSA experiences

- Trustpilot reviews of Hims

What we marked as needing plan-specific verification

- Whether the separately billed Weight Loss Membership fee is reimbursable as a medical expense at your administrator — plan-dependent

- The live pricing on Hims’s dedicated Wegovy page, which showed multiple conflicting dollar figures on the same page during our verification

If anything in this article is out of date when you read it, email us and we’ll re-verify and update with a new “Last verified” stamp.

Frequently asked questions

Still deciding?

HSA/FSA mechanics are one piece of this decision. Your budget, medication preference, insurance situation, state availability, and whether you prefer branded or compounded GLP-1s all shape the right answer. We built a short questionnaire that factors all of these into a specific recommendation.

Still not sure which GLP-1 program is right for you? Take our free 60-second matching quiz.

60 seconds. No spam, no sales calls — just a personalized match.

About Weight Loss Provider Guide

Weight Loss Provider Guide is an independent comparison resource for GLP-1 telehealth providers. We research pricing, policies, and patient experience across the major cash-pay and insurance-backed providers in the U.S. market and publish verified comparisons.

Affiliate disclosure: We earn commission on some provider links at no cost to you. Editorial judgments are based on independent verification of provider policies, public documentation, and IRS/FDA sources — not on commission rate. We disclose this on every commercial page.

Editorial standards: Every price and policy claim on this page was verified against each provider’s own public pages on April 16, 2026. Medical, regulatory, and tax claims are cited to primary sources (IRS, FDA, provider pages, FSAFEDS). We do not fabricate author credentials, medical review attestations, or testimonials. This article is general information, not medical, tax, or legal advice — confirm with a qualified professional before making decisions based on it.

Last verified:

Next scheduled re-verification: July 16, 2026