Can You Use Your HSA or FSA to Pay for GLP-1 Medication?

Short answer: yes. If a licensed provider prescribes a GLP-1 medication — Wegovy, Ozempic, Mounjaro, Zepbound, Rybelsus, or a compounded version of semaglutide or tirzepatide — to treat a diagnosed medical condition, it counts as a qualified medical expense under IRS rules. That means you can pay for it with your HSA or FSA and potentially save 20–40% of the cost (depending on your tax bracket and contribution method) by using pre-tax dollars.

Last Updated: February 27, 2026 | Last Verified: February 27, 2026

Written by: Weight Loss Provider Guide Research Team

Fact-checked against: IRS Publication 502, IRS Publication 969, IRS Notice 2004-50, IRS Notice 2026-05

Disclosure: We may earn a commission when you sign up through links on this page. This doesn't influence our recommendations or the IRS rules we cite — those are what they are.

That's the headline. But the details are where most people either save hundreds of dollars a year or accidentally trigger a 20% tax penalty — and the difference comes down to a few specific things your plan administrator won't tell you.

Here's what we mean: there are expenses most people assume are covered that aren't (like shipping fees and wellness coaching). There are documentation shortcuts that can get your claim denied months after you thought everything was fine. And there's a little-known IRS rule called the “shoebox rule” that lets you reimburse yourself from your HSA for GLP-1 expenses years after you paid — most people have no idea this exists.

We spent weeks digging into IRS Publication 502, Section 213(d), Revenue Procedure 2025-19, the new 2026 OBBBA HSA expansion rules, and the actual payment policies of every major GLP-1 telehealth provider to build the most complete guide on this topic. Below you'll find the exact IRS rules in plain English, a complete eligibility table, step-by-step payment instructions, which providers accept HSA/FSA cards at checkout, a tax savings breakdown, and an audit-proof documentation checklist you can copy.

Everything you need to confidently use your pre-tax dollars for GLP-1 — without a second search.

GLP-1 HSA/FSA Eligibility at a Glance

Before we get into the “why,” here's the quick reference. If you're in a rush, this table tells you what you need to know.

| Medication | Type | HSA Eligible? | FSA Eligible? | LMN Usually Required? | Key Detail |

|---|---|---|---|---|---|

| Ozempic (semaglutide) | Brand-name injection | ✅ Yes | ✅ Yes | Rarely | FDA-approved for type 2 diabetes |

| Rybelsus (semaglutide) | Brand-name oral tablet | ✅ Yes | ✅ Yes | Rarely | FDA-approved for type 2 diabetes |

| Wegovy (semaglutide) | Brand-name injection | ✅ Yes | ✅ Yes | Often | FDA-approved for weight management |

| Mounjaro (tirzepatide) | Brand-name injection | ✅ Yes | ✅ Yes | Depends on indication | FDA-approved for type 2 diabetes |

| Zepbound (tirzepatide) | Brand-name injection | ✅ Yes | ✅ Yes | Often | FDA-approved for weight management |

| Compounded semaglutide | Compounded injection | ✅ Yes | ✅ Yes | Recommended | Must have valid Rx for diagnosed condition |

| Compounded tirzepatide | Compounded injection | ✅ Yes | ✅ Yes | Recommended | Must have valid Rx for diagnosed condition |

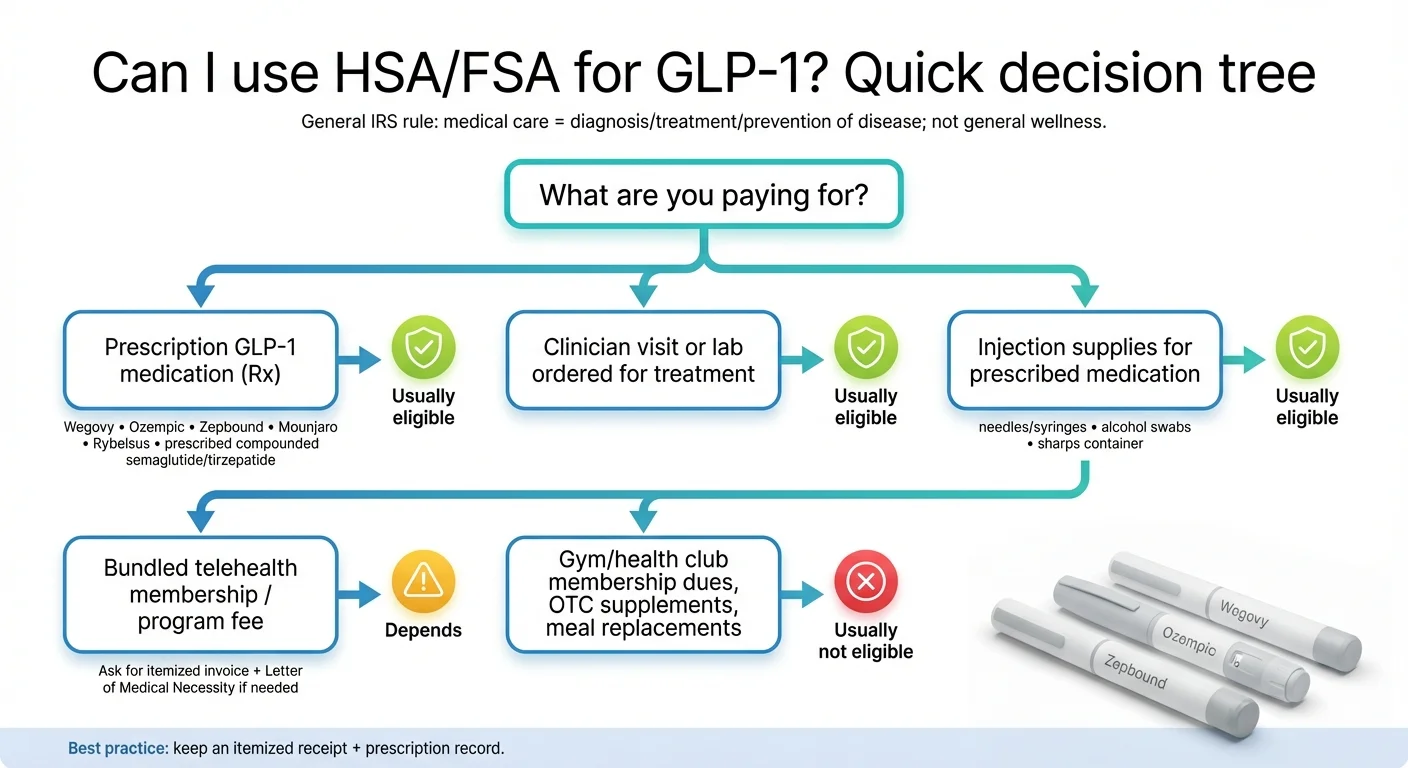

The pattern: The IRS doesn't play favorites between medications. Brand-name, compounded, injection, oral — doesn't matter. What matters is that a licensed provider prescribed it to treat a real medical condition documented in your chart.

If your GLP-1 is prescribed for diabetes, the prescription alone is usually enough. If it's prescribed for weight management, keep a Letter of Medical Necessity on file. We'll explain exactly how to get one below.

The Rule That Decides Everything

Every HSA/FSA eligibility question about GLP-1 comes down to one IRS rule. Once you understand it, the rest of this page is just details.

Under IRS Code Section 213(d), a qualified medical expense is any cost for “the diagnosis, cure, mitigation, treatment, or prevention of disease.” IRS Publication 502 spells it out further: prescription medications are eligible expenses when they treat a medical condition — not when they're merely “beneficial to general health.”

That's the line. Medical treatment of a diagnosed condition = eligible. General wellness = not eligible.

The 3-Question Test

For any GLP-1 expense, ask yourself three questions:

Is it prescribed for a diagnosed medical condition?

Type 2 diabetes, obesity (BMI ≥30), overweight with a comorbidity (BMI ≥27 plus hypertension, high cholesterol, sleep apnea, PCOS, cardiovascular disease, prediabetes) — these all count. “I want to lose 15 pounds for summer” without a documented diagnosis does not.

Is the expense for medical care?

The medication itself, doctor visits, lab work, injection supplies — yes. A gym membership, meal delivery kit, or wellness coaching app — generally no, unless your provider prescribes it specifically to treat a diagnosed condition and you have documentation.

Can you prove it?

You need a paper trail: prescription, receipts, and potentially a Letter of Medical Necessity. The IRS may not ask for years — or ever — but if they do, you need to have it.

Pass all three? You're good. Fail one? That's where problems start.

What the IRS does NOT care about

- • Brand-name vs. compounded

- • Semaglutide vs. tirzepatide

- • Injection vs. oral tablet

- • Which pharmacy fills it

- • Whether insurance covers it or not

- • Whether you use a telehealth provider or see a doctor in person

What the IRS DOES care about

- • Valid prescription from a licensed provider

- • Documented diagnosis in your medical records

- • Medical necessity (not cosmetic, not general wellness)

Sources: IRS Publication 502, IRS Code §213(d), IRS FAQ on Medical Expenses Related to Nutrition, Wellness and General Health

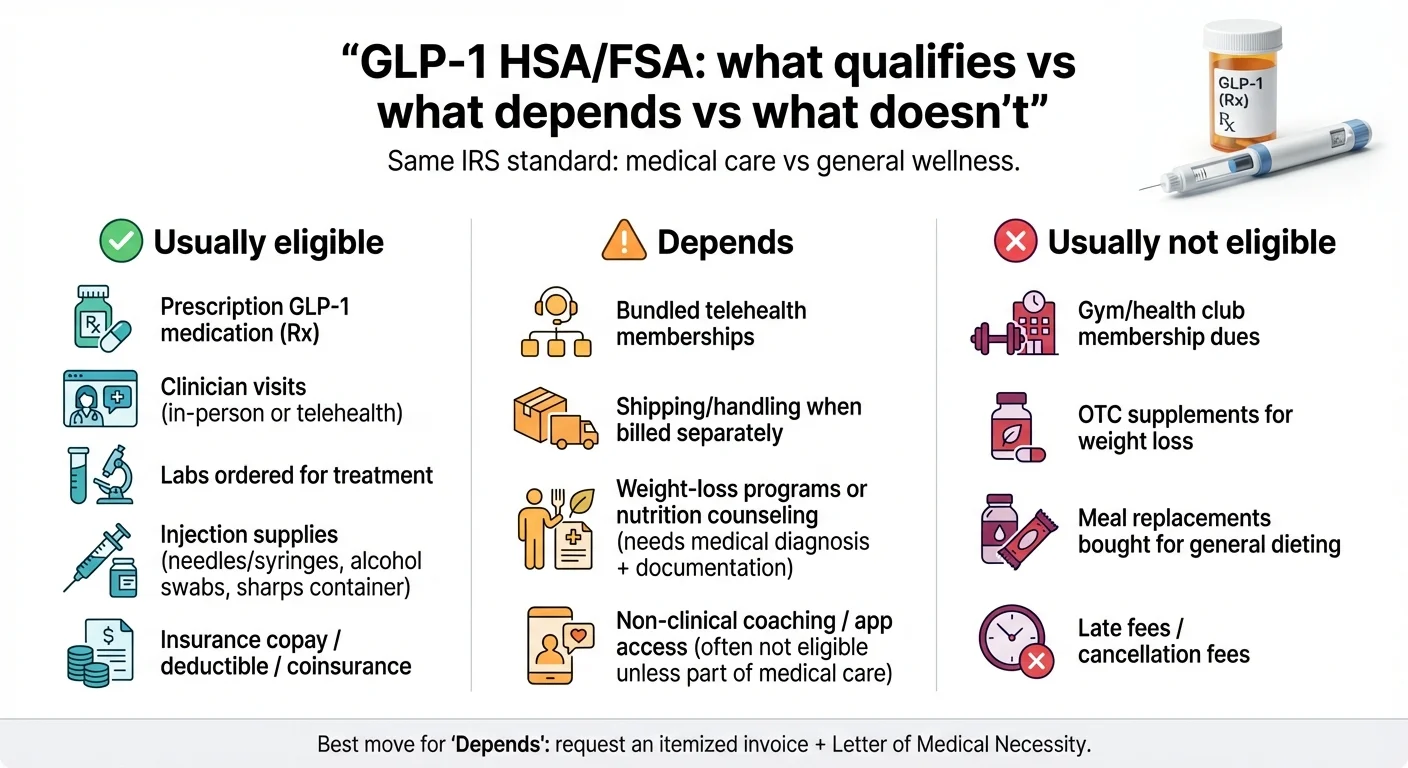

What GLP-1 Expenses Are HSA-Eligible? (The Complete Table)

This is the table we wish existed when we started researching this topic. Every expense type, clearly categorized.

| Expense | HSA/FSA Eligible? | The Rule | What to Keep |

|---|---|---|---|

| GLP-1 medication (brand-name, any pharmacy) | ✅ Yes | Prescription drug for medical condition | Pharmacy receipt + Rx label |

| GLP-1 medication (compounded, prescribed) | ✅ Yes | Prescribed medicine for diagnosed condition | Pharmacy receipt + Rx + LMN recommended |

| GLP-1 medication (online/mail-order pharmacy) | ✅ Yes | Same as above — delivery method doesn't matter | Itemized receipt + Rx |

| Telehealth medical consultation | ✅ Yes | Medical service from licensed provider | Receipt showing provider, date, service |

| Lab work / blood tests (ordered for GLP-1 treatment) | ✅ Yes | Diagnostic medical expense | Lab invoice + provider order |

| Follow-up visits / dose adjustments | ✅ Yes | Ongoing medical care | Visit receipt |

| Injection supplies (syringes, alcohol swabs, sharps container) | ✅ Yes | Medical supplies | Itemized receipt |

| Insurance copay / coinsurance for GLP-1 | ✅ Yes | Out-of-pocket medical expense | EOB + pharmacy receipt |

| Insurance deductible applied to GLP-1 | ✅ Yes | Out-of-pocket medical expense | EOB |

| Shipping/dispensing fees (if itemized as part of Rx) | ⚠️ Depends | May qualify if part of pharmacy dispensing — check with administrator | Itemized invoice |

| Bundled telehealth program fee (monthly subscription) | ⚠️ Depends | Medical portion is eligible; non-medical (coaching, app, community) may not be | Itemized invoice + LMN |

| Weight-loss program (like Calibrate, Noom Med) | ⚠️ Depends | Eligible only if treating a diagnosed disease, with documentation | LMN + program receipt |

| Nutritional counseling | ⚠️ Depends | Only if prescribed for specific medical condition | LMN + receipt |

| Gym/health club membership dues | ❌ No | IRS Pub 502 does not allow gym/health club membership dues. Separate weight-loss activity fees may qualify with documentation. | LMN + receipts for specific activity |

| Weight-loss supplements (non-prescription) | ❌ No | OTC supplements for general health don't qualify under §213(d) | — |

| Meal replacement shakes (SlimFast, Herbalife, etc.) | ❌ No | General nutrition, not medical care | — |

| Late payment / cancellation fees | ❌ No | Administrative, not medical | — |

The “Depends” items are where people get tripped up. The safest move: if you're paying for anything beyond the medication itself and direct medical services, get a Letter of Medical Necessity and ask the provider for an itemized invoice that separates medical from non-medical charges.

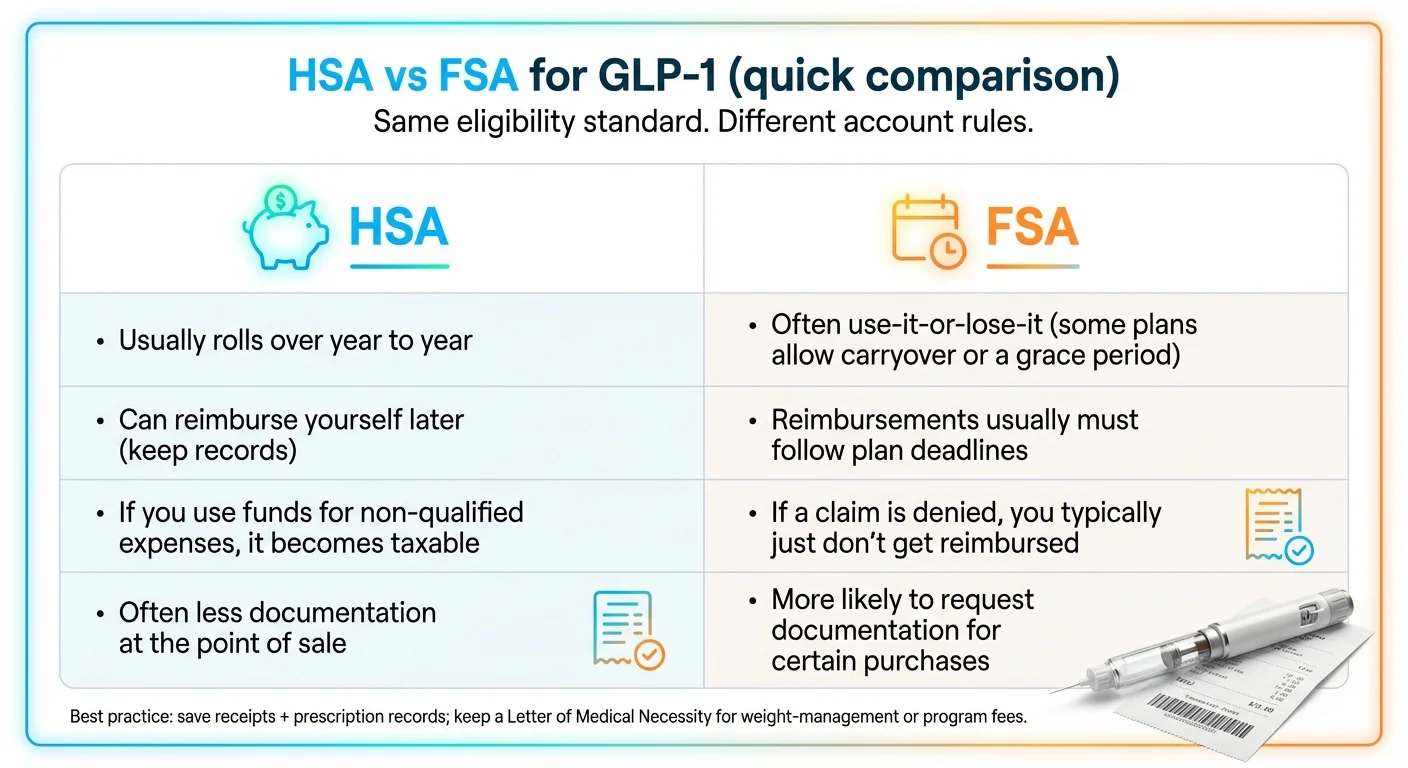

HSA vs. FSA: What's Actually Different for GLP-1 Payments?

People use “HSA” and “FSA” interchangeably. They're not the same — and the differences matter when you're paying for a $200–$300/month medication.

| Feature | HSA (Health Savings Account) | FSA (Flexible Spending Account) |

|---|---|---|

| Who can have one | Must be enrolled in a High Deductible Health Plan (HDHP) | Available through most employer-sponsored plans |

| Tax benefit | Triple tax-free: contributions, growth, and withdrawals | Pre-tax contributions only |

| Rollover | Funds never expire — rolls over every year, forever | Use-it-or-lose-it. Plans may allow up to $680 carryover (2026) or a grace period (up to 2.5 months) — but generally not both. |

| 2026 Contribution Limit (Individual) | $4,400 | $3,400 (IRS max; employer may set lower) |

| 2026 Contribution Limit (Family) | $8,750 | N/A — individual accounts |

| Catch-up (age 55+) | Additional $1,000/year | Not available |

| Payment at checkout | Swipe HSA debit card — usually instant | May work at checkout; some require reimbursement |

| Documentation for GLP-1 | Prescription usually sufficient at point of sale | More likely to require LMN, especially for weight-loss meds |

| If claim is denied | You owe income tax + 20% penalty (if under 65) on non-qualified distribution | Claim simply denied — no penalty, but no reimbursement either |

| Reimbursement deadline | None. You can reimburse yourself years later (the “shoebox rule”) | Must submit within plan year or grace period |

The Practical Takeaway

HSA is simpler for GLP-1. Swipe your card at checkout, keep your receipt, done. No pre-approval needed. The tradeoff: if you're wrong about eligibility, the penalty is real — income tax plus 20% on the amount if you're under 65 (IRS Publication 969).

FSA works but expect more friction. Weight-management prescriptions commonly trigger a “please upload documentation” request from the plan administrator. Diabetes prescriptions usually sail through. The upside: if a claim is denied, there's no penalty — you just don't get reimbursed.

The eligible expense rules are identical. The IRS applies the same Section 213(d) standard to both accounts. The difference is in how the money is managed and how much documentation the administrator requires upfront.

Which Should You Use? Real Scenarios

Scenario 1: You have an HSA and pay $299/month for compounded semaglutide through a telehealth provider. Swipe your HSA card at checkout each month. Save your receipts. Keep an LMN on file. That's it. You'll save roughly $100/month in taxes at a 35% bracket, and the money rolls over if you don't use it all.

Scenario 2: You have an FSA with $2,800 remaining and 3 months left in the plan year. Use your FSA first — those funds expire. Pay for your GLP-1 with your FSA card, and immediately upload your prescription and LMN to your administrator's portal to avoid a processing delay. Plan to use $900+ of that balance on GLP-1 before year-end rather than losing it.

Scenario 3: You have both an HSA and a limited-purpose FSA. Your limited-purpose FSA is only for dental and vision — it won't cover GLP-1. Use your HSA for the medication and save your FSA for dental cleanings and new glasses.

The “Shoebox Rule” (HSA Only)

This is one of the most useful and least-known HSA features. Under IRS Notice 2004-50 (Q&A 39), you can pay for a medical expense out of pocket today and reimburse yourself from your HSA at any point in the future — next month, next year, or a decade from now — as long as the expense was incurred after your HSA was established.

Why this matters for GLP-1: if your HSA card is declined at checkout (it happens — more on that below), pay with a regular credit card. Then reimburse yourself from your HSA later. There's no deadline. Just keep the receipt.

Do You Need a Letter of Medical Necessity (LMN)?

This is the single most common documentation question we see. Let's make it simple.

When You Probably Don't Need One

- • Your GLP-1 is prescribed for type 2 diabetes (Ozempic, Mounjaro, Rybelsus)

- • You're paying at a pharmacy with your HSA debit card

- • Your plan administrator hasn't flagged the transaction

When You Almost Certainly Need One

- • Your GLP-1 is prescribed for weight management (Wegovy, Zepbound, compounded)

- • You're submitting a reimbursement claim to your FSA administrator

- • You're paying for a telehealth program that bundles medical + non-medical services

- • Your HSA/FSA administrator has flagged a transaction and asked for documentation

What an LMN Must Include

A Letter of Medical Necessity is a short document from your licensed provider. It doesn't have to be elaborate. It needs:

- Your name and date of birth

- Your diagnosis — with the ICD-10 code if possible (e.g., E66.01 for morbid obesity, E11.9 for type 2 diabetes without complications, E66.9 for obesity unspecified)

- The medication prescribed — name, dosage, frequency

- A statement of medical necessity — one or two sentences explaining that this medication is prescribed to treat a specific medical condition, not for cosmetic or general wellness purposes

- Provider's name, credentials, and signature

- Date

How to Get an LMN (It Takes 5 Minutes)

Most providers will write one if you ask. Here's a template message you can send through your patient portal:

“Hi [Provider Name], I'm using my HSA/FSA to pay for my GLP-1 medication and my plan administrator requires a Letter of Medical Necessity. Could you provide a brief letter confirming my diagnosis and that this medication is medically necessary to treat it? I need it to include my diagnosis code, the medication name, and a statement of medical necessity. Thank you.”

If you're using a telehealth provider like MEDVi, Hims/Hers, or Calibrate, most of them can provide this documentation on request — it's a common ask. Some include it automatically as part of the enrollment process.

Our Recommendation: Get One Regardless

Even if you don't technically need an LMN right now, request one anyway. It takes five minutes, costs nothing, and protects you if your administrator questions a transaction months later, the IRS audits your HSA distributions (they can go back 3 years), or you switch FSA administrators and need to re-document. Think of it as insurance for your insurance account.

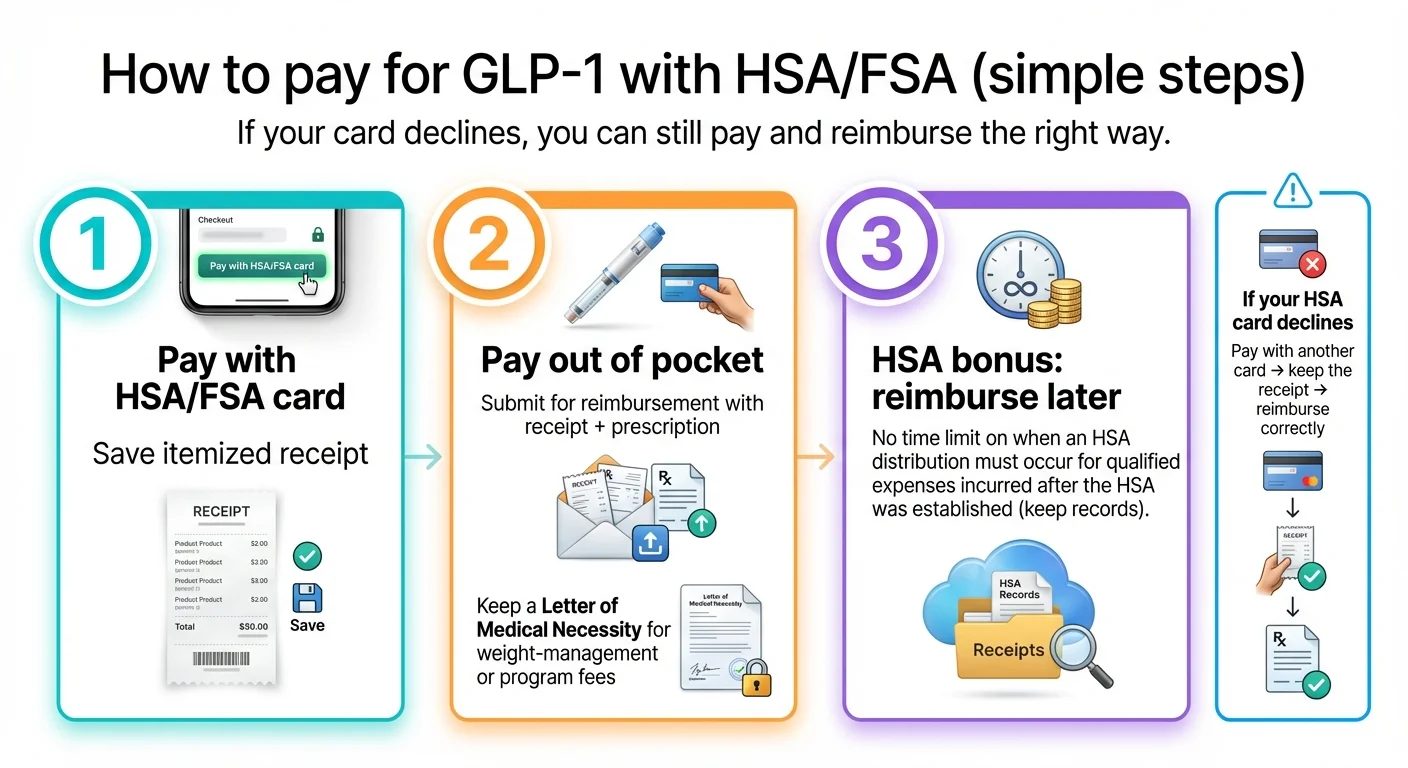

How to Pay for GLP-1 with Your HSA or FSA (Step by Step)

Three paths. Pick the one that fits your situation.

Option 1: Pay with Your HSA/FSA Debit Card at Checkout

This is the simplest path and works at most pharmacies and many telehealth providers.

Step 1: Confirm your HSA/FSA is active and check your available balance. Log into your account portal or call your administrator.

Step 2: When checking out — at the pharmacy counter, online pharmacy, or telehealth provider — select your HSA/FSA debit card as your payment method.

Step 3: Complete the transaction. For HSA, it usually processes instantly. For FSA, it may process instantly or get flagged for review (especially for weight-management medications).

Step 4: Save your itemized receipt. It should show: provider/merchant name, date of service, your name, medication name, and the amount charged.

Step 5: If your FSA flags the transaction, upload your prescription details and LMN through your administrator's portal.

Option 2: Pay Out of Pocket, Then Reimburse Yourself

Use this when the provider doesn't accept HSA/FSA cards, when your card is declined, or when you prefer to keep the spending on a rewards credit card and reimburse later.

Step 1: Pay with a regular credit card, debit card, or other payment method.

Step 2: Log into your HSA/FSA online portal.

Step 3: Submit a reimbursement claim. You'll need: itemized receipt (provider name, date, medication, amount, your name), prescription documentation, and Letter of Medical Necessity (if required by your plan).

Step 4: Wait for processing. Most HSA reimbursements process in 1–3 business days. FSA claims may take 2–5 business days, sometimes longer if documentation review is needed.

Step 5: Funds are deposited back to your bank account or HSA.

HSA bonus: There's no deadline for reimbursement. You can pay out of pocket in February and reimburse yourself from your HSA in December — or three years from now. The only requirement is that the expense occurred after your HSA was established (IRS Notice 2004-50, Q&A 39).

FSA reminder: You typically must submit claims within the plan year or grace period. Don't wait — check your plan's deadlines.

A Note on HRA (Health Reimbursement Arrangements)

If you have an HRA through your employer instead of (or in addition to) an HSA or FSA, GLP-1 medications may also be reimbursable. HRAs follow similar IRS rules for qualified medical expenses. However, HRAs are entirely employer-funded and employer-controlled — meaning your employer decides what's covered and what's not. Check your HRA plan documents or contact your benefits administrator to confirm GLP-1 eligibility.

Option 3: Insurance Pays Part, HSA/FSA Pays the Rest

If your insurance covers your GLP-1 (even partially), your out-of-pocket costs — deductible, copay, coinsurance — are HSA/FSA eligible.

Step 1: Fill your prescription through insurance.

Step 2: Pay your copay/coinsurance at the pharmacy with your HSA/FSA card.

Step 3: If you have a deductible to meet first, those out-of-pocket payments are also HSA/FSA eligible. Keep your Explanation of Benefits (EOB) and pharmacy receipts.

Important: Don't double-dip. If insurance reimburses you for an expense, you can't also reimburse yourself from your HSA/FSA for the same amount. Only your true out-of-pocket portion qualifies.

Which GLP-1 Providers Accept HSA/FSA Cards?

This is one of the biggest practical questions — and one that nobody else answers clearly. We reviewed the payment policies of the most popular GLP-1 telehealth platforms. Here's what we found.

| Provider | HSA/FSA Card at Checkout? | Receipt for Reimbursement? | LMN on Request? | Starting Price | Medication Type |

|---|---|---|---|---|---|

| MEDVi | ✅ Yes | ✅ Yes | ✅ Yes | $179/mo (first month) | Compounded semaglutide/tirzepatide |

| Hims / Hers | ✅ Yes | ✅ Yes (downloadable receipt) | Varies by provider | $199/mo | Compounded |

| Calibrate | ✅ Yes (HSA, FSA, or credit card) | ✅ Yes | ✅ Yes | $199/mo membership | Brand-name + lifestyle program |

| LifeMD / ShedRx | ✅ Yes (via HSA Store) | ✅ Yes | ✅ Yes | Varies | Compounded |

| Noom Med | ❌ No direct HSA/FSA payment | ✅ Yes (provides documentation) | ✅ Yes | Varies | Brand/compounded |

| Ro Body | Check with provider | ✅ Yes | Varies | Varies | Compounded |

| Your local pharmacy (CVS, Walgreens, etc.) | ✅ Yes (HSA/FSA card accepted) | ✅ Yes (pharmacy receipt) | N/A (get from prescriber) | Varies by insurance | Brand-name |

Table last verified: February 2026. All claims are provider-stated per official websites and FAQ pages. Policies can change — confirm with the provider before enrolling.

If You Want the Simplest HSA/FSA Experience

MEDVi stands out here for a practical reason: they accept HSA/FSA cards directly (provider-stated), and the $179/month first-month price bundles the physician evaluation, medication, treatment plan, and shipping into a single line item. That makes the HSA/FSA claim straightforward — it's one medical expense, not a pile of itemized charges to sort through. Refills run $299/month after that.

They also provide documentation for reimbursement if you'd rather pay with a regular card and submit a claim. And their clinical team can provide LMN documentation on request.

MEDVi

From $179/month

If You're Using Insurance for Brand-Name GLP-1

Use your HSA/FSA card at the pharmacy for your copay or coinsurance. If your insurance requires prior authorization and it's approved, your out-of-pocket portion is the HSA/FSA eligible expense.

If Your Provider Doesn't Accept HSA/FSA Cards

Pay with a regular card, keep your itemized receipt, and submit for reimbursement through your HSA/FSA portal. This works with any provider — the IRS doesn't care how you pay, only that the expense qualifies.

Can You Use HSA for Compounded GLP-1 Medications?

Yes. This is one of the most-searched variants of this question, and the answer is straightforward once you understand the IRS rule.

The IRS does not distinguish between brand-name and compounded medications. If a licensed healthcare provider prescribes a compounded medication to treat a diagnosed medical condition, it's a qualified medical expense under Section 213(d). The IRS cares about the prescription and the diagnosis — not the FDA approval status of the specific formulation.

What qualifies

- • Compounded semaglutide or tirzepatide prescribed by a licensed provider (MD, DO, NP, PA) through a telehealth platform or in-person clinic

- • Dispensed by a state-licensed compounding pharmacy

- • For a documented medical condition (obesity, diabetes, etc.)

What does NOT qualify

- • Medications shipped without a valid prescription

- • Products from non-compliant pharmacies or gray-market sources

- • “Semaglutide” purchased without any prescriber involvement

The LMN factor: Because compounded GLP-1s are more commonly prescribed through telehealth for weight management (rather than through traditional pharmacies for diabetes), FSA administrators are more likely to request documentation. We strongly recommend having an LMN on file for any compounded GLP-1 purchase.

A note on safety: Compounded medications are not FDA-approved as finished products. The FDA has raised concerns about certain unapproved GLP-1 products. If you're considering compounded GLP-1, verify that the provider uses a state-licensed compounding pharmacy (and if applicable, an FDA-registered outsourcing facility). Reputable telehealth providers partner with established compounding pharmacies that operate under applicable federal and state compounding regulations. Learn more about compounded semaglutide safety.

Brand-Name vs. Compounded: The Cost Reality

Here's the practical reason most people are searching this question with compounded GLP-1 specifically in mind. Brand-name Wegovy or Zepbound without insurance can cost $1,000–$1,500+ per month. Compounded semaglutide through a telehealth provider typically runs $179–$399/month. That price difference is why compounded GLP-1 through telehealth has exploded — and why “can I use my HSA for compounded semaglutide” is such a high-volume question.

The answer remains the same: if it's prescribed by a licensed provider for a diagnosed condition, the IRS treats it as a qualified medical expense. The cost savings of compounded + the tax savings of HSA/FSA can make GLP-1 treatment significantly more accessible. At $299/month through an HSA in a 35% tax bracket, your effective cost drops to about $194/month — compared to $1,200+ for brand-name out-of-pocket without tax advantages.

For a detailed price comparison, see our guides to the cheapest GLP-1 options without insurance and GLP-1 costs with and without insurance.

Telehealth GLP-1 Programs: Are Monthly Fees HSA-Eligible?

This is the section that stops a lot of people mid-search. Telehealth GLP-1 programs often charge a monthly subscription that bundles multiple services together. Is the whole thing eligible?

It depends on what's included — and how it's billed.

| Component | HSA/FSA Eligible? | Why |

|---|---|---|

| Physician consultation / medical evaluation | ✅ Yes | Medical service |

| Prescription medication | ✅ Yes | Prescribed drug for medical condition |

| Lab work | ✅ Yes | Diagnostic medical expense |

| Dose adjustment / clinical follow-ups | ✅ Yes | Medical care |

| Health coaching (non-clinical) | ⚠️ Depends | Only if treating diagnosed condition with provider documentation |

| App access / community features | ❌ Usually no | General wellness, not medical care |

| Shipping | ❌ Usually no | Not medical care (unless bundled into pharmacy dispensing fee) |

The Key Question: Bundled vs. Itemized

If the provider bundles everything into one “monthly membership fee” and the majority of the charge is for medical services (consultation + medication), most HSA administrators will accept it as a medical expense — especially with an LMN.

If the provider charges separately for medical and non-medical components, only the medical portions are eligible.

What to ask your telehealth provider:

- “Can you provide an itemized invoice that separates medical services from non-medical services?”

- “Can you provide an LMN or documentation stating that this program is medical treatment for my diagnosed condition?”

- “Does your receipt clearly show the provider name, service type, and date?”

Pro tip: Providers like MEDVi bundle the physician review, medication, treatment plan, and shipping into one flat monthly fee. Because the core of the charge is a medical consultation and prescription medication, it's straightforward to classify as a medical expense. If your plan administrator asks questions, the LMN from MEDVi's clinical team covers it.

If Your HSA Card Gets Declined (Don't Panic)

It happens more often than you'd think — and it almost never means the expense isn't eligible. Here's what's actually going on.

Common Reasons for a Declined HSA Card

Merchant Category Code (MCC) mismatch. Every merchant is assigned a category code by their payment processor. If the provider's MCC isn't flagged as “medical,” your HSA card may auto-decline. This is a payment processing issue, not an IRS eligibility issue.

The provider uses a non-medical payment processor. Some telehealth platforms process payments through general e-commerce systems rather than medical billing systems. The card thinks it's a retail purchase.

Insufficient HSA balance. Check your available balance — it may be lower than you think if you have pending transactions or recent contributions that haven't posted yet.

Your HSA administrator has a restricted merchant list. Some administrators only auto-approve transactions from pharmacies and medical offices with specific merchant codes.

What to Do

- Don't assume the expense isn't eligible. A declined card is a payment processing issue, not a tax law issue.

- Pay with a regular credit or debit card. Get an itemized receipt.

- Reimburse yourself from your HSA. Log into your HSA portal, submit the receipt, and the money goes back to your bank account. Remember — there's no deadline for HSA reimbursement.

- If using an FSA: Pay out of pocket, then submit a reimbursement claim with receipt + LMN through your administrator's portal.

- Contact your HSA administrator if it keeps happening. They may be able to whitelist the merchant or update the MCC classification.

The bottom line: A declined card doesn't mean “not eligible.” It means the payment didn't go through. The IRS eligibility of the expense is completely separate from whether a particular card transaction processes successfully.

Can You Use HSA with Insurance, GoodRx, or Savings Cards?

HSA + Insurance

Yes. If your insurance covers part of your GLP-1 cost, you can use your HSA/FSA for the remaining out-of-pocket portion — your copay, coinsurance, or deductible amount. Just don't submit the same expense for both insurance reimbursement and HSA/FSA reimbursement (that's double-dipping, and the IRS doesn't allow it).

HSA + GoodRx or Manufacturer Coupons

Yes, with a caveat. If you use a GoodRx coupon and pay a discounted price, you can use your HSA to pay that discounted amount. The HSA-eligible expense is what you actually pay out of pocket — not the retail price.

If you use a manufacturer savings card (like those offered by Novo Nordisk or Eli Lilly) that reduces your copay to $0, there's no remaining expense to reimburse. You can only use HSA/FSA for the portion you actually pay.

HSA + Cash-Pay Telehealth (No Insurance)

Yes. This is actually the most straightforward scenario. If your GLP-1 is cash-pay (no insurance involved), the entire amount you pay is potentially HSA/FSA eligible — as long as it's for medical care treating a diagnosed condition. No EOB needed, no coordination of benefits. Just your receipt and prescription documentation.

This is why cash-pay telehealth providers pair well with HSA accounts. You pay one price, you get one receipt, and the whole thing is a medical expense.

How Much Can Your HSA Save You on GLP-1?

Using your HSA or FSA for GLP-1 isn't just “allowed” — it's one of the biggest legal tax savings strategies available for an ongoing medical expense. Here's the actual math.

HSA and FSA contributions are made with pre-tax dollars. That means you typically save on federal income tax and often state income tax. If your HSA contributions are made through payroll deduction (cafeteria plan), you also save on FICA taxes (Social Security + Medicare = 7.65%). Depending on your situation, total savings typically ranges from 20–40% on every dollar you spend through these accounts.

Tax Savings Estimates by Bracket

| Combined Tax Bracket | Monthly GLP-1 Cost | Monthly Tax Savings | Annual Tax Savings | Effective Monthly Cost |

|---|---|---|---|---|

| 25% (lower bracket + FICA) | $179/mo | ~$45 | ~$537 | ~$134 |

| 30% | $179/mo | ~$54 | ~$645 | ~$125 |

| 35% | $199/mo | ~$70 | ~$836 | ~$129 |

| 35% | $299/mo | ~$105 | ~$1,255 | ~$194 |

| 40% (higher bracket) | $299/mo | ~$120 | ~$1,435 | ~$179 |

What this means practically: If you're in a 35% combined tax bracket paying $299/month for compounded semaglutide, using your HSA effectively saves you over $1,250 per year. That's like getting four months of medication for free.

2026 HSA Contribution Limits

| Coverage Type | 2026 HSA Limit | 2025 HSA Limit | Change |

|---|---|---|---|

| Self-only | $4,400 | $4,300 | +$100 |

| Family | $8,750 | $8,550 | +$200 |

| Catch-up (age 55+) | +$1,000 | +$1,000 | No change |

Source: IRS Revenue Procedure 2025-19

Open enrollment planning tip: If you know you'll be on a GLP-1 for the next year, factor that cost into your HSA/FSA contribution election during open enrollment. A $299/month GLP-1 costs $3,588/year — well within the $4,400 individual HSA limit. Contribute enough to cover it, and you're saving 30–40% on every dollar.

2026 Update: New HSA Rules That Affect GLP-1 Affordability

If you've been paying attention to tax news, you may have heard that HSA rules just changed significantly. Here's what it means for GLP-1 users.

The One, Big, Beautiful Bill Act (OBBBA)

Signed into law on July 4, 2025, the OBBBA expanded HSA eligibility in several ways that directly affect people paying for GLP-1 medications:

1. Bronze and catastrophic ACA plans now qualify as HDHPs (effective January 1, 2026). Previously, many ACA marketplace plans didn't meet the technical definition of a High Deductible Health Plan, which meant you couldn't contribute to an HSA. Now, bronze and catastrophic plans automatically qualify — even if they don't meet the traditional HDHP deductible requirements. This change makes many more ACA enrollees eligible to open and contribute to an HSA, depending on their plan and other eligibility rules (IRS Notice 2026-05, December 9, 2025).

2. Telehealth services can be covered before the HDHP deductible is met — and this is now permanent. Previously, receiving telehealth services before meeting your deductible could disqualify you from HSA contributions. That restriction is gone for good.

3. Direct Primary Care (DPC) arrangements are now HSA-compatible. Starting January 1, 2026, you can be enrolled in a DPC arrangement and still contribute to your HSA. You can also use HSA funds to pay DPC fees tax-free.

Why This Matters for GLP-1 Users

More people can now open HSAs, which means more people can use pre-tax dollars for GLP-1 medications. If you're on an ACA bronze plan and couldn't contribute to an HSA before, check your eligibility for 2026 — you may now qualify.

And the permanent telehealth exception is directly relevant: if you're using a telehealth GLP-1 provider, your HDHP can cover those telehealth visits without jeopardizing your HSA eligibility.

Source: IRS Notice 2026-05, Treasury/IRS announcement December 9, 2025

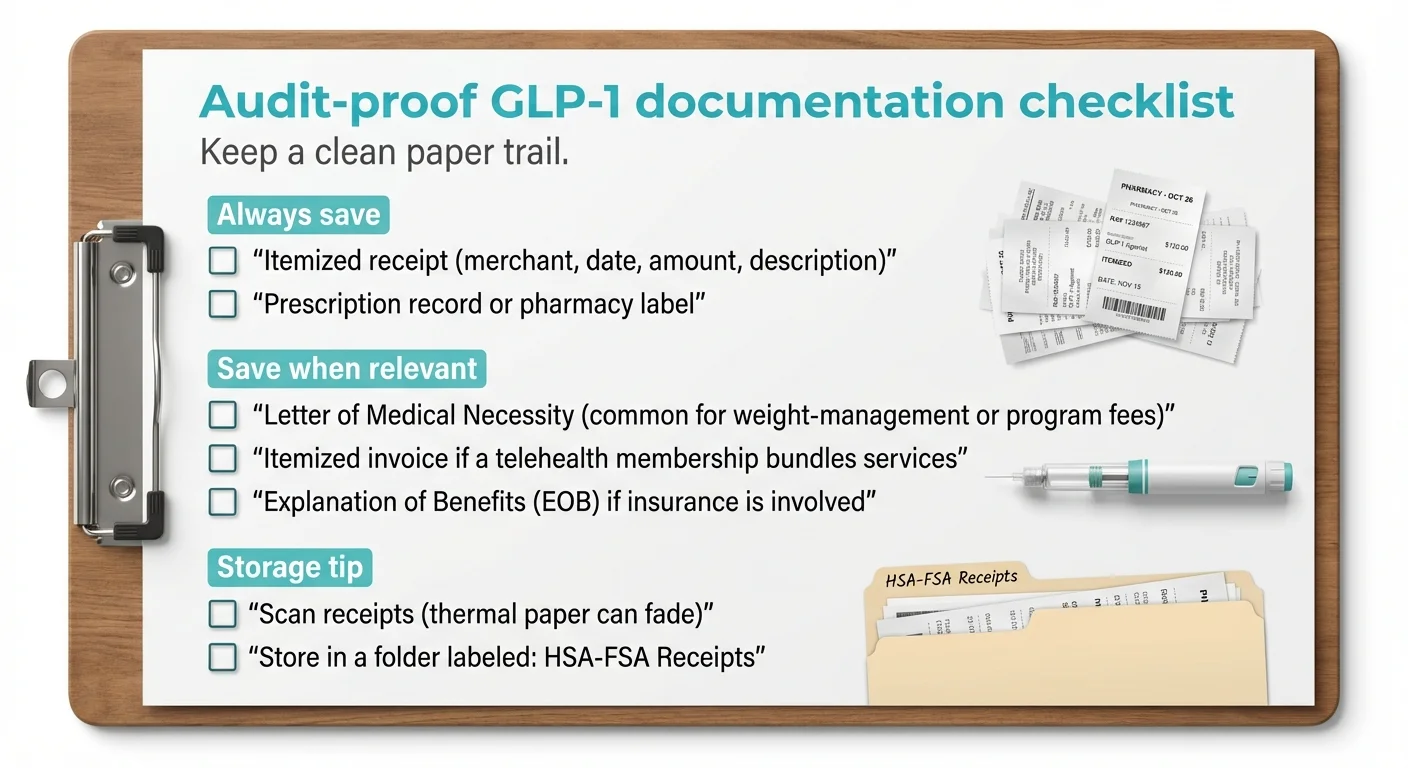

Your Audit-Proof Documentation Checklist

The IRS can review HSA distributions going back three years (six years if they suspect substantial underreporting). You don't need to submit documentation when you file your taxes — but you need to have it if they ask.

For Every Transaction

- ☐ Itemized receipt — must show: provider/merchant name, date of service, your name (or patient name), medication or service description, and dollar amount

- ☐ Prescription documentation — pharmacy printout, Rx label, or provider's prescription record showing the medication, dosage, and prescribing provider

For Weight-Management GLP-1 (Wegovy, Zepbound, Compounded)

- ☐ Letter of Medical Necessity (LMN) — from your licensed provider, stating diagnosis + medical necessity

- ☐ Diagnosis documentation — ideally with ICD-10 code in your medical records

If Using Insurance

- ☐ Explanation of Benefits (EOB) — showing what insurance covered and what you owe

- ☐ Pharmacy receipt showing your out-of-pocket amount

If Using a Telehealth Program

- ☐ Itemized invoice — separating medical services from non-medical services (if applicable)

- ☐ LMN or program documentation confirming medical treatment purpose

Storage Recommendations

- • Create a dedicated folder (physical or digital) labeled “HSA Medical Records [Year]”

- • Scan paper receipts — thermal receipt paper fades

- • Save LMNs as PDFs

- • Keep a simple spreadsheet: date, provider, expense type, amount, HSA/FSA used, documentation on file (yes/no)

- • Retain records for at least 3 years after the tax year of the distribution (6 years for extra safety)

This checklist takes 60 seconds per transaction. It could save you thousands in penalties.

When GLP-1 Is NOT HSA-Eligible (Common Mistakes)

Knowing what doesn't qualify is just as important as knowing what does. These are the scenarios that get people in trouble.

“Prescription” from a wellness clinic with no documented diagnosis

Some clinics prescribe GLP-1 for weight loss without documenting an actual medical condition in your chart. The prescription is legal, but without a coded diagnosis (obesity, diabetes, etc.), it doesn't meet the IRS standard. If your chart says “patient requests weight loss” instead of “E66.01 — morbid obesity due to excess calories,” your HSA/FSA claim is vulnerable.

General wellness programs not tied to treating a diagnosed disease

A wellness coaching app, fitness program, or nutrition plan is not a medical expense just because you're also taking a GLP-1. It would need to be specifically prescribed by your provider to treat your diagnosed condition — and you'd need documentation proving that.

Non-prescription weight-loss supplements

Over-the-counter supplements marketed for weight loss (garcinia cambogia, green tea extract, etc.) are not qualified medical expenses. They're “beneficial to general health” at best, and the IRS explicitly excludes those.

Paying for someone else's GLP-1 (who isn't your dependent)

HSA funds can only be used for qualified medical expenses for you, your spouse, or your tax dependents. Paying for a friend's or parent's (who isn't your dependent) GLP-1 is a non-qualified distribution.

Using HSA funds for the same expense that was reimbursed by insurance

If insurance already paid for the medication, you can't also reimburse yourself from your HSA. Only your actual out-of-pocket cost is eligible.

The penalty for getting it wrong: If you use HSA funds for a non-qualified expense and you're under 65, you owe income tax on the amount plus a 20% additional tax. Over 65, the 20% penalty goes away, but you still owe income tax (IRS Publication 969).

The Simple Rule to Stay Safe

When in doubt, apply the 3-question test from earlier in this article. If you can answer “yes” to all three — diagnosed condition, medical care expense, and documented — you're on solid ground. If any answer is “no” or “I'm not sure,” get clarification from your provider or plan administrator before using HSA/FSA funds.

And honestly? The easiest safeguard is an LMN. Five minutes of your provider's time can save you from a tax headache that lasts months. If you're spending $200–$300/month on GLP-1 through your HSA, the documentation is worth the effort.

What to Do Next

You now know more about using HSA/FSA for GLP-1 than 99% of people searching this topic. Here's how to put it into action based on where you are right now.

Path 1: You Already Have a GLP-1 Prescription

You're the simplest case. Here's your checklist:

- Check your HSA/FSA balance and confirm your account is active

- Pay with your HSA/FSA card at the pharmacy or telehealth provider

- Keep your itemized receipt (provider name, date, medication, amount)

- If it's for weight management, make sure you have an LMN on file

- Store your documentation in a dedicated folder — physical or digital

Path 2: You Need a GLP-1 Provider That Accepts HSA/FSA

If you don't have a prescription yet and want the smoothest HSA/FSA experience, you need a provider that makes the payment and documentation straightforward.

Our recommendation: MEDVi accepts HSA/FSA cards directly and bundles everything — physician evaluation, personalized treatment plan, medication, and shipping — into one flat monthly payment starting at $179. No insurance paperwork, no prior authorizations, no hidden fees. Their clinical team can provide LMN documentation on request, and you get a clean receipt that works for HSA/FSA reimbursement.

They prescribe compounded semaglutide and tirzepatide (injectable or oral) through licensed providers in all 50 states, with 24–48 hour approval and direct-to-door delivery.

MEDVi

From $179/month

If MEDVi isn't right for your situation — maybe you want brand-name medication, or you prefer a different provider — refer to our provider comparison table above. The key is making sure whoever you choose can give you proper documentation for your HSA/FSA records. You can also explore our full GLP-1 online program comparison.

Path 3: You're Planning Ahead for Next Year

Smart move. During your next open enrollment period, increase your HSA or FSA contribution to account for anticipated GLP-1 costs. Here's a quick planning framework:

- • Monthly GLP-1 cost × 12 = annual medication expense

- • Example: $299/month × 12 = $3,588/year

- • That's well within the $4,400 individual HSA limit for 2026

- • At a 35% combined tax bracket, you'll save roughly $1,255 in taxes — money that stays in your pocket instead of going to the IRS

If you're not currently enrolled in an HDHP but want HSA access, the 2026 OBBBA changes may help. Bronze and catastrophic ACA plans now qualify as HSA-compatible — check whether your current plan makes you eligible.

Path 4: You're Using Telehealth and Need Documentation Clarity

If you're already enrolled in a telehealth GLP-1 program and aren't sure whether your monthly fee qualifies:

- Ask your provider for an itemized invoice separating medical services from non-medical components

- Request an LMN — most telehealth providers will provide one

- Submit both to your HSA/FSA administrator with your reimbursement claim

- If the claim is denied, refer to our “claim denied” section above for next steps

The documentation takes 10 minutes. The tax savings last all year.

FAQ: HSA and GLP-1 Medications

Can you use HSA for Ozempic?

Yes. Ozempic (semaglutide) is FDA-approved for type 2 diabetes and is a qualified medical expense when prescribed by a licensed provider. Your HSA debit card should work at any pharmacy. An LMN is usually not required for diabetes-indication prescriptions.

Can you use HSA for Wegovy?

Yes. Wegovy (semaglutide) is FDA-approved for chronic weight management in adults with obesity (BMI ≥30) or overweight with at least one weight-related condition (BMI ≥27). Because it's a weight-management indication, your FSA administrator may request a Letter of Medical Necessity. For HSA, the prescription is typically sufficient at point of sale, but keep an LMN on file.

Can you use HSA for Mounjaro?

Yes. Mounjaro (tirzepatide) is FDA-approved for type 2 diabetes. If prescribed for diabetes, it's straightforward. If prescribed off-label for weight management, have an LMN ready.

Can you use HSA for Zepbound?

Yes. Zepbound (tirzepatide) is FDA-approved for weight management. Like Wegovy, the weight-management indication means you should have an LMN on file, especially for FSA claims.

Can you use HSA for compounded semaglutide?

Yes. The IRS does not differentiate between brand-name and compounded medications. If it's prescribed by a licensed provider for a diagnosed medical condition, it's a qualified medical expense. Keep your prescription documentation and an LMN.

Can you use HSA for compounded tirzepatide?

Yes. Same rule as compounded semaglutide — the IRS applies the same standard regardless of whether the medication is brand-name or compounded.

Can you use HSA for GLP-1 for weight loss (not diabetes)?

Yes, if your provider documents a qualifying medical condition. Obesity (BMI ≥30), overweight with a comorbidity (BMI ≥27 + hypertension, high cholesterol, PCOS, sleep apnea, prediabetes, cardiovascular disease), and other diagnosed conditions qualify. "I want to lose weight" without a documented diagnosis does not.

Can you use FSA for GLP-1?

Yes. FSA follows the same IRS eligibility rules as HSA. The difference is that FSA administrators are more likely to require upfront documentation (especially an LMN) before approving a weight-management expense. Diabetes prescriptions usually process without issue.

Can you use HSA for a telehealth GLP-1 program?

Yes. Telehealth medical consultations are qualified medical expenses. The medication prescribed through the program is also eligible. If the program includes non-medical components (coaching app, community access), those portions may not be eligible — ask for an itemized invoice.

Can you use HSA for online GLP-1 prescriptions?

Yes. The delivery method doesn't affect eligibility. Whether you fill your prescription at a local pharmacy, mail-order pharmacy, or online telehealth provider, the expense is eligible if it meets the IRS requirements (prescription + diagnosed condition).

Can you use HSA with GoodRx for GLP-1?

Yes. If you use a GoodRx coupon and pay a discounted price, you can use your HSA to pay that discounted amount. The eligible expense is what you actually pay out of pocket.

Do you need a Letter of Medical Necessity for GLP-1?

Not always, but we recommend getting one regardless. Diabetes prescriptions rarely require one. Weight-management prescriptions commonly do — especially for FSA claims. Having an LMN on file protects you in case your administrator or the IRS questions the expense.

Can you reimburse yourself from HSA for GLP-1 you already paid for?

Yes. Under the "shoebox rule" (IRS Notice 2004-50), you can reimburse yourself from your HSA at any time — even years later — as long as the expense was incurred after your HSA was established and you haven't already been reimbursed from another source.

What if my HSA card is declined at a GLP-1 provider?

A declined card doesn't mean the expense isn't eligible. It's usually a payment processing issue (merchant category code, non-medical processor, or insufficient balance). Pay with a regular card, keep your receipt, and reimburse yourself from your HSA later.

What happens if I use HSA for something that isn't eligible?

If you're under 65, you owe income tax on the distribution amount plus a 20% additional tax. If you're 65 or older, the 20% penalty is waived, but you still owe income tax. The best prevention: keep documentation for every HSA expense and get an LMN when in doubt (IRS Publication 969).

How much can I contribute to my HSA in 2026?

For 2026: $4,400 for individual HDHP coverage, $8,750 for family coverage. If you're 55 or older, you can contribute an additional $1,000 as a catch-up contribution. These limits are set by IRS Revenue Procedure 2025-19.

Can I use both HSA and FSA for GLP-1?

Generally, you can't use both for the same expense. If you have a limited-purpose FSA (dental/vision only) alongside an HSA, it won't cover GLP-1. If you have a general-purpose FSA and an HSA (which is uncommon — most people have one or the other), check with your plan administrator about coordination rules.

Is an HSA or FSA better for paying for GLP-1?

For most people, HSA is better for an ongoing expense like GLP-1. Funds roll over forever (no use-it-or-lose-it pressure), there's no deadline for reimbursement, documentation requirements are typically lighter at point of sale, and the triple tax advantage (contributions, growth, and withdrawals are all tax-free) makes it a more powerful financial tool. FSA works fine, but requires more planning around deadlines and documentation.

Can I use my HSA for GLP-1 injection supplies?

Yes. Syringes, needles, alcohol swabs, and sharps containers are medical supplies and qualify as HSA/FSA expenses when used as part of your prescribed treatment.

Can I use my HSA for GLP-1 lab work?

Yes. Blood tests, metabolic panels, A1C tests, and other lab work ordered as part of your GLP-1 treatment are diagnostic medical expenses — fully HSA/FSA eligible.

What if my GLP-1 FSA claim is denied?

Don't panic. Call your administrator to find out why. The most common reasons: missing LMN, incomplete receipt, or the expense was classified as "wellness" instead of "medical." Get the missing documentation from your provider and resubmit. If still denied, appeal with your LMN, prescription records, and a reference to IRS Publication 502 showing that prescription medications for diagnosed conditions are qualified medical expenses.

How We Verify This Information

We take accuracy seriously — especially on a topic where getting it wrong can mean tax penalties.

Primary sources cited in this article:

- • IRS Publication 502 (Medical and Dental Expenses)

- • IRS Publication 969 (Health Savings Accounts and Other Tax-Favored Health Plans)

- • IRS Code Section 213(d) (Definition of medical care)

- • IRS FAQ on Medical Expenses Related to Nutrition, Wellness and General Health

- • IRS Revenue Procedure 2025-19 (2026 HSA contribution limits)

- • IRS Notice 2026-05 (OBBBA guidance on HSA eligibility changes)

- • IRS Notice 2004-50 (HSA Q&As, including reimbursement timing)

- • FDA: Concerns About Unapproved GLP-1 Drugs Used for Weight Loss

Provider information: HSA/FSA acceptance policies were reviewed from each provider's official website, FAQ pages, and published materials. We update this information periodically but recommend confirming directly with any provider before enrolling.

What this article is NOT: This is educational content, not tax advice, legal advice, or medical advice. We're not CPAs, tax attorneys, or doctors. For guidance specific to your tax situation, consult a qualified tax professional. For medical decisions, consult your healthcare provider. For questions about your specific HSA/FSA plan rules, contact your plan administrator.

Update schedule: We review this article for accuracy whenever IRS rules, HSA limits, FDA guidance, or major provider policies change. The “Last Verified” date at the top reflects our most recent review.

Related Articles

Can You Use HSA/FSA for TrimRx? (2026 Verified Rules)

TrimRx accepts HSA/FSA cards — but only when prescribed for a diagnosed condition. See the 2026 IRS rules, proof packet, and real tax savings.

Does Eden Take HSA or FSA? Verified 2026 Answer & What Qualifies

Eden accepts HSA and FSA cards. See verified Eden claims, IRS qualification rules, step-by-step payment walkthrough, and what to do if your claim is denied.

Does Hers Accept HSA/FSA? 2026 Reimbursement Guide

Yes — Hers GLP-1 medications are HSA/FSA-eligible, but reimbursement-first. Verified April 2026: real pricing, 4-step process, and what to do if denied.

Does Hims Accept HSA/FSA? 2026 Verified Answer + What Qualifies

Does Hims accept HSA/FSA? Yes for weight loss — via reimbursement, not direct card swipe. Real 2026 costs, what qualifies, what doesn't, and how to file.

Does LillyDirect Accept HSA/FSA? Yes — 2026 Rules + Catch

Yes — LillyDirect takes most HSA/FSA cards for Zepbound ($299–$449/mo). See the rules, the insurance catch, and how to fix a declined card.

Does MEDVi Accept Affirm? No — Plus 3 Verified Paths

MEDVi does not publicly list Affirm at checkout. See what MEDVi does accept, whether the Affirm Card workaround actually works, and 3 verified BNPL alternatives for 2026.

This article is for informational purposes only. Consult your healthcare provider for medical advice and a qualified tax professional for tax guidance specific to your situation.