Zepbound Prior Authorization: What's Required, How Long It Takes, and What to Do If You're Denied

Disclosure: Some links on this site are affiliate links. If you purchase through these links, we may earn a commission at no extra cost to you. Thank you for supporting our site.·For informational purposes only—not medical advice.

Bottom line: Prior authorization for Zepbound typically takes 1–7 business days. Most insurers require a BMI of 30 or higher — or 27+ with a condition like diabetes, high blood pressure, or sleep apnea — along with documented lifestyle modification and sometimes trials of cheaper medications first. The number-one cause of PA delays isn't ineligibility. It's incomplete documentation. Come to your doctor's appointment prepared, and you cut days off the process.

If you're denied, don't give up. In Medicare Advantage, KFF found only about 11% of prior authorization denials were appealed — but when patients appealed, 81% were overturned. A denial is often worth challenging, especially when the reason is missing documentation. See our complete step-by-step guide: How to Appeal a Wegovy or Zepbound Denial (7 Real Steps, 2026).

And if insurance won't work at all? You can get brand-name Zepbound through LillyDirect starting at $299/month, or explore compounded tirzepatide through telehealth providers like MEDVi starting around $279/month or less.

Medical Disclaimer: This guide is for informational purposes only and does not constitute medical advice. Always consult your healthcare provider before starting, stopping, or changing any medication. Zepbound (tirzepatide) is a prescription medication with risks and contraindications — see full prescribing information at zepbound.lilly.com.

What Is Prior Authorization for Zepbound?

Prior authorization is your insurance company's way of saying: “Before we pay for this, prove you actually need it.”

That's it. It's a coverage review — not a rejection. Your doctor's office submits documentation on your behalf, and your insurer decides whether you meet their criteria. You can't submit the PA yourself, but you can (and should) prepare everything your doctor needs before the appointment.

How the process works:

Your doctor prescribes Zepbound. The prescription hits the pharmacy.

The pharmacy flags it. Your insurance requires PA before they'll cover it.

Your doctor's office submits the PA request — clinical notes, BMI, comorbidities, treatment history.

Your insurer reviews. They'll approve it, deny it, or ask for more information.

You get a decision, typically within 1–7 business days.

Why does Zepbound need PA in the first place? Two reasons: it's a newer specialty medication, and the list price runs about $1,086 per month. Insurers want to verify medical necessity before writing that check. Nearly every insurance plan in the US requires PA for Zepbound — it's standard, not personal.

What happens behind the scenes

When your doctor's office submits the PA, it goes to your pharmacy benefit manager (PBM) — the company that actually makes drug coverage decisions for your insurer. The three biggest PBMs are CVS Caremark, Express Scripts, and OptumRx. Together, they manage pharmacy benefits for the majority of insured Americans.

Your PBM reviews the submission against a criteria checklist. A clinical pharmacist or automated system checks whether your documentation matches their published requirements — BMI thresholds, comorbidities, prior treatments, lifestyle documentation. If everything checks out, you're approved. If something's missing or doesn't match, you get denied or they request additional information.

Key insight: PA decisions are made by checklist, not by clinical judgment. That means your job is to make sure every box is checked before submission. This guide shows you exactly which boxes matter.

What PA is not

PA is not a denial. It's not your insurer saying “no.” It's your insurer saying “show me the paperwork.” The distinction matters because many patients see “prior authorization required” and assume the worst. In practice, the majority of PAs with complete documentation get approved.

Quick vocabulary decoder

| Term | What It Means |

|---|---|

| Prior Authorization (PA) | Insurer's pre-approval before covering a drug |

| Formulary | Your plan's list of covered medications |

| Step Therapy | Requirement to try cheaper drugs first before Zepbound is approved |

| Letter of Medical Necessity (LMN) | A letter from your doctor explaining why you specifically need Zepbound |

| Formulary Exception | A request for your insurer to cover a drug not on their standard list |

| PBM (Pharmacy Benefit Manager) | The company that manages your prescription drug benefits (e.g., CVS Caremark, Express Scripts, OptumRx) |

| ICD-10 Code | The standard billing code your doctor uses to describe your diagnosis |

What Insurers Require to Approve Zepbound

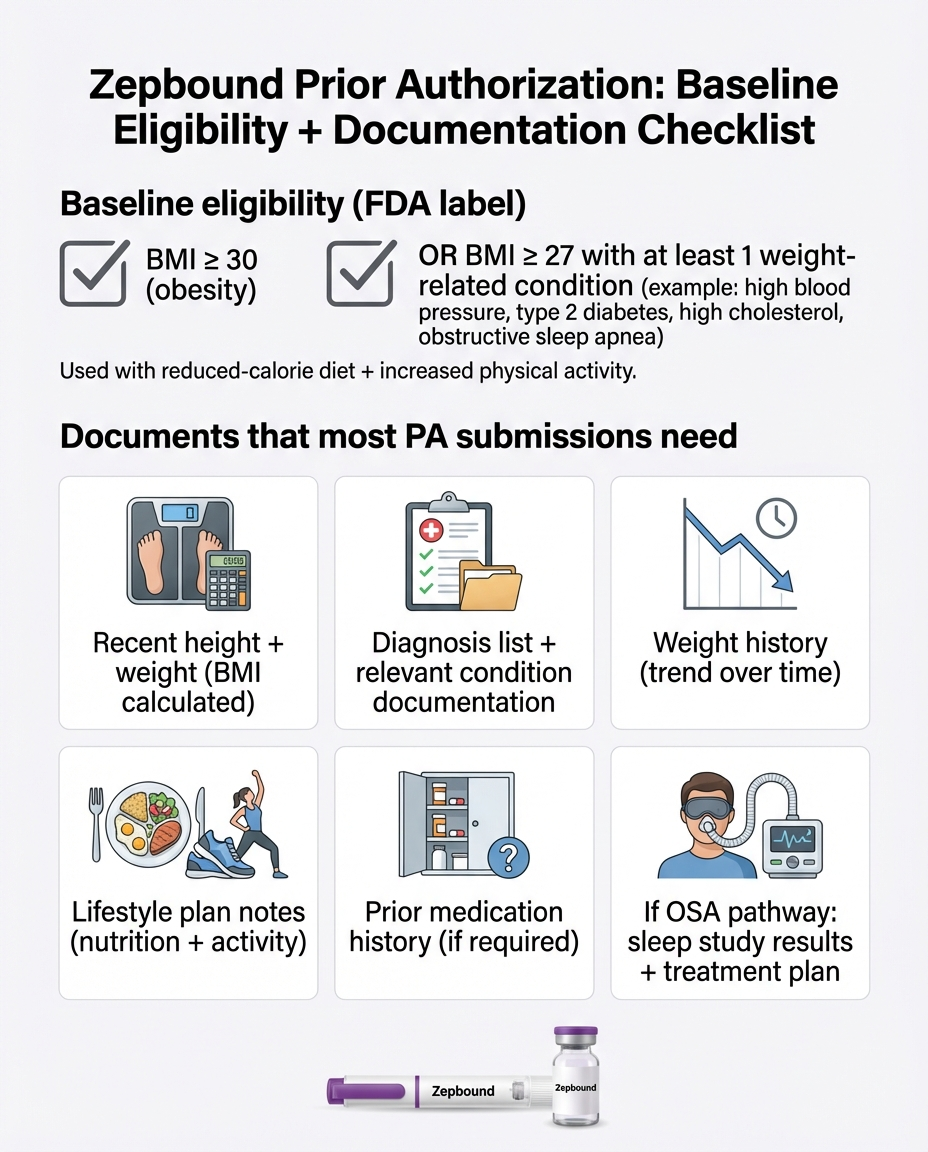

What the FDA says (the baseline)

Zepbound (tirzepatide) is FDA-approved for:

- Chronic weight management in adults with a BMI ≥30 (obesity), or BMI ≥27 (overweight) with at least one weight-related comorbid condition — used alongside a reduced-calorie diet and increased physical activity.

- Moderate-to-severe obstructive sleep apnea (OSA) in adults with obesity (FDA-approved December 2024).

What insurers add on top

Most insurers will require some combination of:

1. BMI documentation. A recent height and weight measurement with dates, calculated BMI, and the corresponding ICD-10 diagnosis code. This is non-negotiable for every insurer.

2. Comorbidity documentation. If your BMI is between 27 and 29.9, you must have at least one weight-related condition. Common qualifying conditions include type 2 diabetes, high blood pressure, high cholesterol, obstructive sleep apnea, and cardiovascular disease.

3. Lifestyle modification proof. Many insurers require documentation that you've participated in a structured weight-management program (diet, exercise, behavioral counseling) for at least 3–6 months. This is one of the most common documentation gaps that leads to denials.

4. Step therapy (prior medication trials). Some plans require you to try and fail cheaper weight-loss medications before they'll approve Zepbound. Common step therapy drugs include phentermine, Contrave, Qsymia, Saxenda, and in some cases Wegovy.

5. Adjunct therapy confirmation. The PA form typically asks your doctor to confirm you'll use Zepbound alongside a reduced-calorie diet and increased physical activity.

ICD-10 codes your doctor will use

| ICD-10 Code | Description |

|---|---|

| E66.01 | Morbid (severe) obesity due to excess calories — BMI ≥40, or ≥35 with comorbidities |

| E66.09 | Other obesity due to excess calories — BMI ≥30 |

| E66.3 | Overweight — BMI 27–29.9 |

| G47.33 | Obstructive sleep apnea |

| E11.xx | Type 2 diabetes mellitus |

| I10 | Essential hypertension |

| E78.xx | Disorders of lipoprotein metabolism (high cholesterol) |

Zepbound PA Requirements by Major Insurer (2025–2026)

Requirements vary significantly depending on who manages your pharmacy benefits. We reviewed actual PA criteria documents from major insurers and PBMs.

| Insurer / PBM | BMI Threshold | Lifestyle Documentation | Step Therapy? | Key Notes |

|---|---|---|---|---|

| Aetna | ≥30, or ≥27 + comorbidity | 6+ months diet/exercise documentation | Varies by plan | Must show ≥5% weight loss at renewal to continue coverage |

| UnitedHealthcare | ≥30, or ≥27 + comorbidity | Chart notes required | Some plans require Wegovy or Saxenda trial first | Many UHC commercial plans only cover Zepbound for OSA, not weight loss |

| Cigna | ≥30, or ≥27 + comorbidity | Detailed ICD-10 documentation | May require Saxenda trial | 8 months initial; 1 year for continuation. Requires specific diagnosis codes |

| Blue Cross Blue Shield | Varies by affiliate | Yes | Varies by plan | BCBS Michigan stopped covering GLP-1 drugs for weight loss for many members (Jan 2025). Check your specific state plan. |

| CVS Caremark | ≥30, or ≥27 + comorbidity | Chart notes + lifestyle program docs | Wegovy now preferred (since July 2025) | Removed Zepbound from standard formulary July 2025. Wegovy is preferred. |

| Express Scripts | ≥30, or ≥27 + comorbidity | 6 months behavioral/diet program docs | Varies by plan | Check current formulary status — varies by employer plan |

| TRICARE | ≥30, or ≥27 + comorbidity | Diet and exercise documentation | May require prior trials | PA submitted via Express Scripts. Separate military/VA criteria may apply. |

| Medicare Part D | N/A for weight loss | N/A | N/A | Does NOT cover Zepbound for weight loss. Only covers for OSA (since FDA approval Dec 2024). |

Important 2025–2026 Changes

- • CVS Caremark removed Zepbound from its standard commercial formulary effective July 1, 2025. Wegovy is now the preferred GLP-1.

- • BCBS Michigan stopped covering GLP-1s for weight loss for many fully insured large group members starting January 1, 2025.

- • Medicare Part D can now cover Zepbound for OSA following the FDA's December 2024 approval.

- • Some insurers are tightening step therapy requirements — extending trial periods and requiring documented trials of multiple medications.

Last verified: February 2026. Policies change frequently — always confirm with your specific plan.

How to Prepare: Your Zepbound PA Checklist

The single most important thing you can do to speed up your PA — and avoid a denial — is walk into your doctor's appointment with everything they need. Most delays happen because documentation is incomplete, not because you don't qualify.

Before your doctor appointment

- Know your current BMI. Weigh yourself on a recent date and calculate: (weight in pounds ÷ height in inches²) × 703. Better yet, have it documented by your doctor within the last 30 days.

- Bring your weight history. Dates and weights over the past 1–2 years, if you have them.

- Document all weight-loss programs you've tried. Nutrition counseling receipts, gym membership records, dietitian notes, Weight Watchers enrollment, Noom subscription, wearable fitness data — anything showing sustained effort over 3–6 months.

- List all weight-loss medications you've taken. Drug name, dates of use, doses, outcomes, and why you stopped. This is critical for step therapy requirements.

- Gather your comorbidity records. Diagnosis dates and treatment records for type 2 diabetes, high blood pressure, high cholesterol, sleep apnea, PCOS, joint disease, or any other weight-related condition.

- If you have sleep apnea: Bring your most recent sleep study results, including your AHI score. Also bring CPAP compliance records or documentation of CPAP failure/intolerance.

- Call your insurer. Before the appointment, call using your Member ID and ask: "Is Zepbound on my plan's formulary? What are the specific prior authorization requirements?"

- Ask about format requirements. Some insurers require specific forms or submission through electronic PA platforms like CoverMyMeds or Availity.

What to say to your doctor

“I've put together everything you should need for the Zepbound PA. Here's my weight history, my records of prior diet and exercise programs, the medications I've tried before, and my comorbidity diagnoses. My insurer requires [specific criteria you learned from your phone call]. Would you also be willing to write a Letter of Medical Necessity? I understand it significantly increases the chances of approval.”

This isn't pushy — it's helpful. You're saving your doctor's staff time and showing you've done your homework.

What your doctor's office will submit

- The PA form — specific to your insurer or PBM

- Clinical notes — documenting BMI, diagnosis codes, comorbidities, and current treatment plan

- Lifestyle modification evidence — chart notes showing diet/exercise counseling, program participation records

- Prior medication history — if step therapy applies

- Letter of Medical Necessity — strongly recommended. This significantly increases approval odds and is essential for appeals.

After submission

- Get the submission date from your doctor's office and the expected review timeline.

- Check your insurer's patient portal — many let you track PA status online.

- Follow up at 3–5 business days if you haven't heard back.

- If your insurer requests additional information — respond immediately. Delays can restart the review clock or lead to automatic denial.

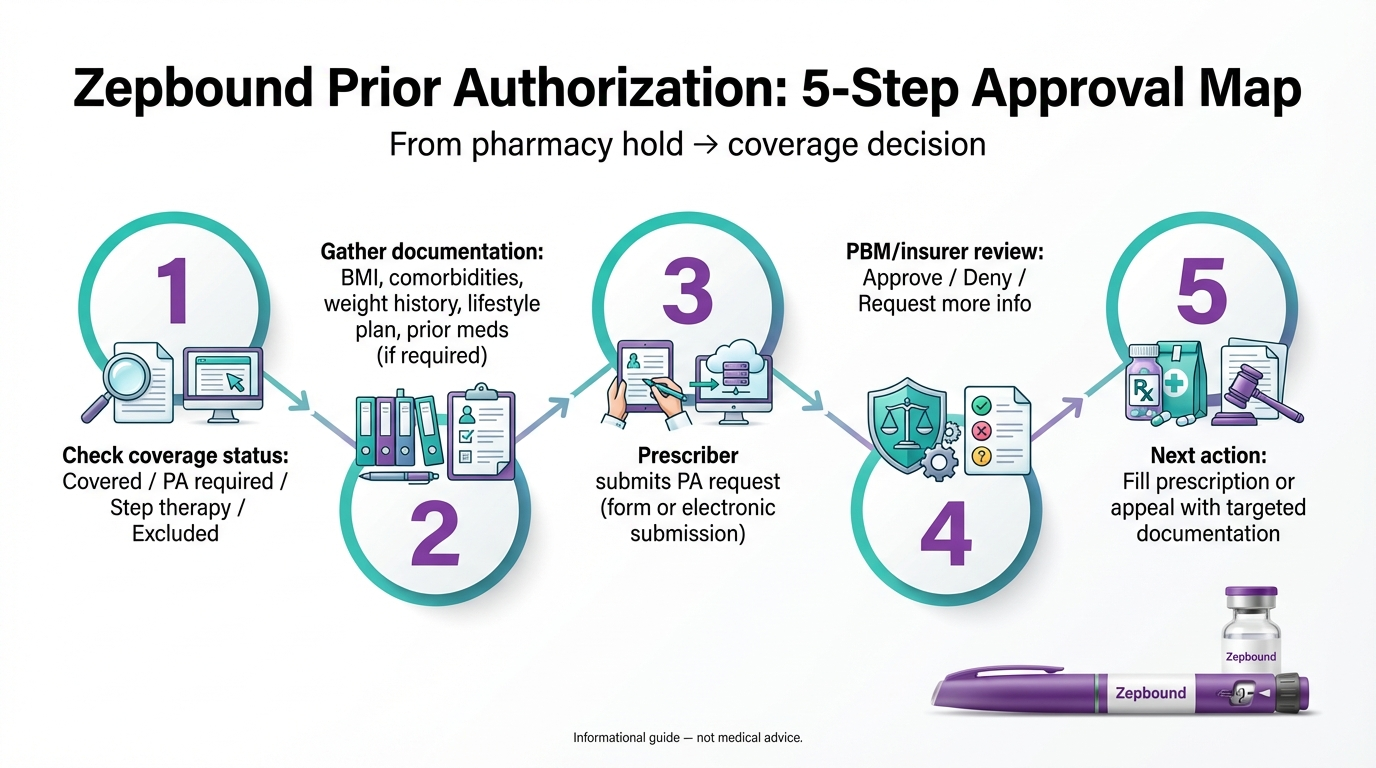

The 5-Step Approval Map

Verify Coverage

Call your insurance. Ask if Zepbound is covered and if PA is required. Get the specific criteria in writing.

Gather Your Documentation

Collect weight history, comorbidity records, lifestyle modification proof, and prior medication history. Use the checklist above.

Prepare Your Doctor

Bring your documentation to the appointment. Ask for a Letter of Medical Necessity. Make their job easy.

Track the Timeline

Get the submission date, check your portal, follow up at 3–5 days. Respond immediately to any requests for additional information.

Fill or Appeal

If approved, fill your prescription. If denied, appeal immediately — most appeals succeed.

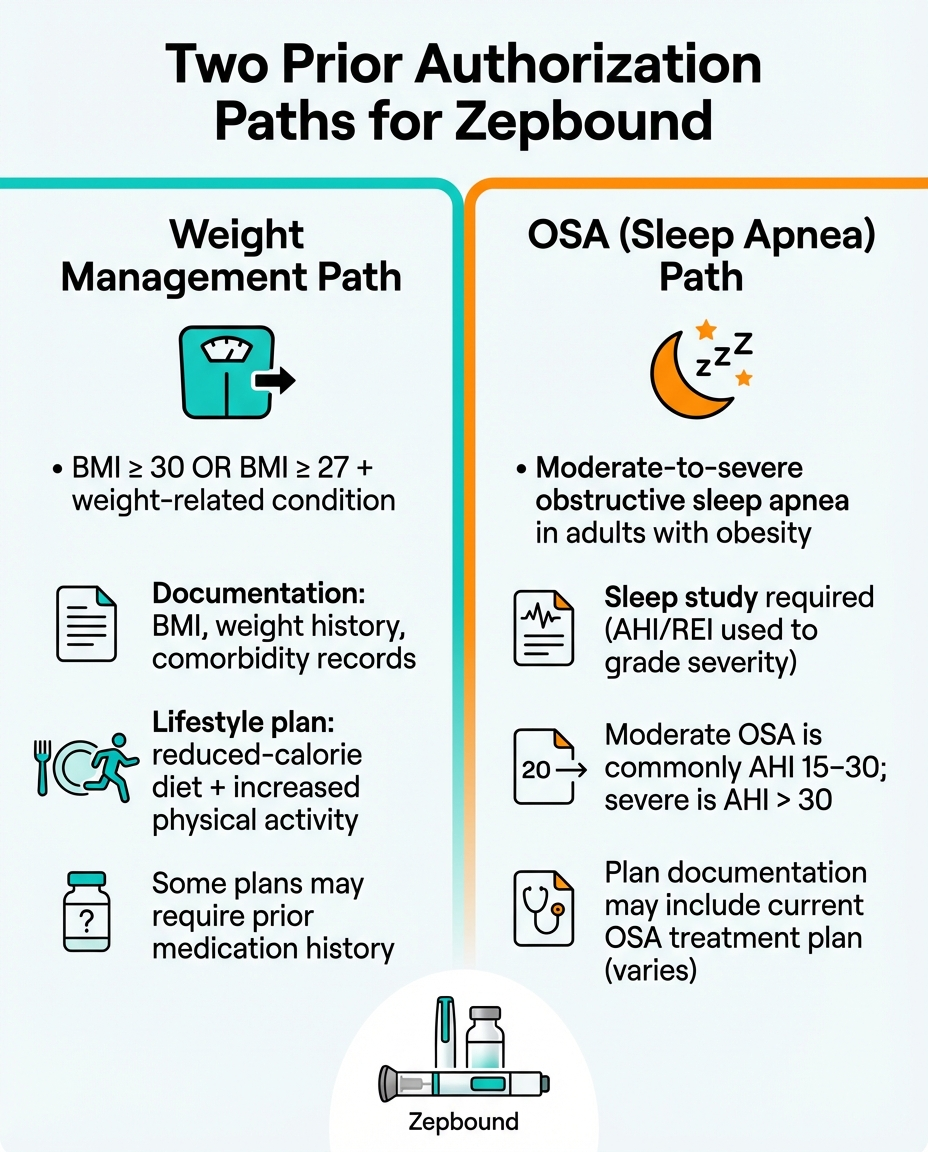

The OSA Pathway: Different Rules, Broader Coverage

If you have obstructive sleep apnea and obesity, pay close attention. This pathway may be your best route to coverage — especially if your plan excludes weight-loss medications or if you're on Medicare.

In December 2024, the FDA approved Zepbound for the treatment of moderate-to-severe OSA in adults with obesity. This was a game-changer. It opened coverage pathways that didn't exist before.

Why OSA matters for your PA

Many insurance plans that explicitly exclude anti-obesity medications still cover treatments for OSA. UnitedHealthcare, for example, has a published policy where Zepbound is available as a non-formulary PA only for OSA — not for weight loss. And Medicare Part D, which has a statutory exclusion for weight-loss drugs, can now cover Zepbound when OSA is the primary diagnosis.

Typical OSA PA criteria

- Confirmed OSA diagnosis via a sleep study (polysomnography or home sleep test)

- AHI (Apnea-Hypopnea Index) ≥15 events per hour — this is moderate-to-severe

- BMI ≥30 documented in medical records

- Evidence of CPAP/PAP therapy — many plans require documentation that you've tried positive airway pressure therapy and either failed, couldn't tolerate it, or had insufficient improvement

- Current treatment plan including diet and exercise

Weight Management PA vs. OSA PA

| Requirement | Weight Management PA | OSA PA |

|---|---|---|

| Primary diagnosis code | E66.01 or E66.09 (obesity) | G47.33 (obstructive sleep apnea) |

| BMI threshold | ≥30 or ≥27 + comorbidity | ≥30 (typically) |

| Sleep study results | Not required | Required — must show AHI ≥15 (moderate-severe) |

| CPAP documentation | Not required | Often required — trial with documented failure, intolerance, or insufficient improvement |

| Lifestyle modification | 3–6 months in many plans | Required but duration may differ |

| Step therapy (weight-loss drugs) | Often required | Usually NOT required for OSA indication |

| Renewal criteria | ≥5% weight loss | May require documented AHI improvement or stability |

Key advantage: Step therapy for weight-loss medications is usually not required for OSA indication. Since the primary indication is sleep apnea treatment, insurers typically don't demand trials of phentermine or Saxenda first. This can save months of waiting.

CVS Caremark and Zepbound: What Changed and What to Do

In July 2025, CVS Caremark removed Zepbound from its standard commercial formulary, with Wegovy as the preferred weight-loss GLP-1 effective July 1, 2025. If CVS Caremark manages your pharmacy benefit, you may need to switch to Wegovy or request an exception.

| Aspect | Before July 2025 | After July 2025 |

|---|---|---|

| Zepbound status | Covered with prior authorization on most plans | Removed from standard commercial formulary |

| Preferred GLP-1 | Varied by plan | Wegovy is the preferred GLP-1 |

| New Zepbound patients | Standard PA process | Must switch to Wegovy or request formulary exception |

| Existing Zepbound patients | Current PA valid | Existing PA may no longer be valid. Three options: switch to Wegovy, request exception, or go self-pay |

| Self-insured employers | Standard formulary | May override PBM formulary — check with HR |

If you're new to Zepbound

Wegovy is now the preferred GLP-1 on your plan. Your doctor can prescribe Wegovy instead, or request a formulary exception for Zepbound. A formulary exception requires documentation showing why Wegovy isn't appropriate for you — for example, prior Wegovy use with inadequate response, intolerable side effects, or a clinical reason your doctor prefers tirzepatide over semaglutide.

If you were already on Zepbound

Your existing PA may no longer be valid. Three options:

Switch to Wegovy

Easiest path. Talk to your doctor about transitioning.

Request a Zepbound formulary exception

Have your doctor submit documentation showing why you need Zepbound specifically. Include a Letter of Medical Necessity.

Go self-pay

LillyDirect offers Zepbound vials and KwikPen without insurance (see alternatives section).

Check if your employer is self-insured. If so, they may be able to override the PBM's formulary decision and direct CVS Caremark to continue covering Zepbound. It's worth a call to your HR department.

How Long Does Zepbound Prior Authorization Take?

Short answer: 1–7 business days from complete submission. The biggest factor isn't your insurer — it's your documentation.

| Scenario | Timeline | What's Happening |

|---|---|---|

| Best case | 24 hours | Electronic submission, complete documentation, straightforward case |

| Typical | 3–5 business days | Standard review with no missing information |

| Extended | 1–2+ weeks | Incomplete documentation, insurer requests additional info, or complex case |

| Urgent/Expedited | 24–72 hours | Your doctor certifies medical urgency — triggers faster review |

Three possible outcomes after submission:

Legal timelines you should know (ERISA)

- Urgent claims: Decision within 72 hours

- Pre-service claims (standard PA): Decision within 15 calendar days, with one 15-day extension if insurer notifies you

- Appeals: Decision within 30 days for pre-service appeals

These are maximums. Most decisions come faster. But if your insurer is dragging past these deadlines, you have legal ground to push back.

7 Common Mistakes That Delay or Kill Your PA

1. Not calling your insurer first. Before the doctor appointment, call and ask for the specific PA criteria for Zepbound under your plan. This takes 15 minutes and can save weeks.

2. Assuming your doctor knows the PA requirements. Your doctor is an expert in medicine. They may not be an expert in your specific insurer's PA criteria. Bring the requirements to them.

3. Missing the lifestyle modification documentation. This is the single most common documentation gap. If your insurer requires 6 months of diet and exercise proof and you don't have it, the PA will be denied.

4. Not documenting prior medications thoroughly. "I tried phentermine a few years ago" isn't enough. You need dates, doses, duration, and outcomes.

5. Using the wrong primary diagnosis code. If your doctor submits with E66.09 (obesity) but your plan only covers Zepbound for OSA, you'll be denied regardless of documentation quality.

6. Not following up. Submitting the PA and waiting silently is a mistake. Check your portal after 3–5 business days. Call if there's no update.

7. Giving up after the first denial. This is the biggest mistake of all. The data is clear — the majority of appeals succeed. A denial is not a final answer.

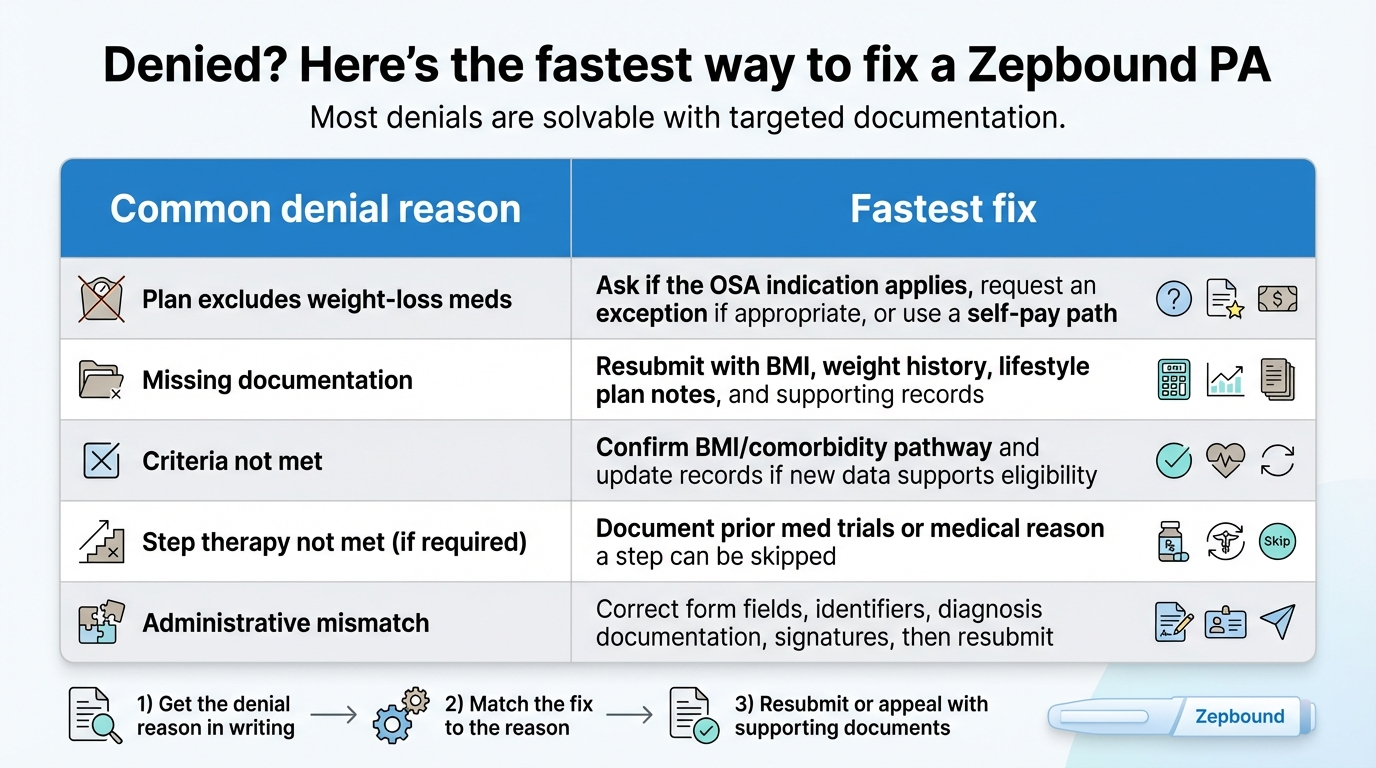

What to Do If Your Zepbound PA Is Denied

A denial feels like the end of the road. It's not. It's the start of a different conversation — and the data is overwhelmingly in your favor.

The stat that changes everything

According to KFF's analysis of Medicare Advantage data, only about 11% of prior authorization denials were appealed in 2024 — but 81% of those appeals were overturned. The vast majority of people who fight a denial win. The vast majority never fight. Appeal.

Why PAs get denied (the 6 most common reasons)

| Denial Reason | What It Means | How to Fix It |

|---|---|---|

| Not on formulary | Your plan doesn't list Zepbound as a covered drug, or removed it (CVS Caremark, July 2025) | Request a formulary exception. Document why alternatives aren't appropriate. |

| Medical necessity not established | Missing BMI documentation, insufficient comorbidity coding, or no treatment plan | Resubmit with complete documentation and a Letter of Medical Necessity. |

| Step therapy not completed | Insurer requires trials of cheaper medications first | Document previous medication use (dates, doses, outcomes). Document medical reasons if you can't take certain drugs. |

| Incomplete documentation | Wrong ICD-10 code, unsigned form, missing chart notes, lifestyle docs not included | Call your insurer to find out exactly what was missing. Often a quick resubmission fixes this. |

| Plan exclusion | Your employer plan excludes weight-loss medications entirely | Check if OSA indication applies. Contact HR about adding coverage. See OAC sample letters. |

| Medicare weight-loss exclusion | Medicare Part D has a statutory exclusion for anti-obesity medications | If you have moderate-to-severe OSA, ask your doctor about submitting with OSA as the primary indication. |

How to appeal, step by step

Read your denial letter carefully.

The specific reason matters. "Not medically necessary" is a different fight than "not a covered benefit."

Call your insurer.

Ask exactly which criteria you failed to meet. Get names, dates, and reference numbers.

Work with your doctor.

Request a Letter of Medical Necessity that specifically addresses the denial reason — not a generic letter.

Gather supporting evidence.

Updated BMI, recent lab results, prior medication records, specialist notes, sleep study results if applicable.

File your internal appeal.

Most plans allow 180 days. Don't wait. Include the LMN, supporting documentation, and a clear statement of why the denial should be reversed.

Request a peer-to-peer review.

Your doctor can speak directly with the insurer's medical director. This is often effective — it's harder to deny coverage when a physician is making the case in real time.

If internal appeal fails → External review.

You have the right to an independent third-party review. File through your state insurance department or through HealthCare.gov for Marketplace plans.

What a strong Letter of Medical Necessity includes

- Patient identification and clinical summary — Brief overview of your medical history

- Diagnosis and clinical justification — BMI, comorbidities, ICD-10 codes

- Treatment history — Previous weight-loss efforts (behavioral, dietary, pharmacological) with specific dates, durations, and outcomes

- Clinical rationale for Zepbound — Why this medication specifically, based on your clinical profile. Reference the SURMOUNT trials if helpful.

- Expected treatment plan — Dose titration schedule, planned monitoring, concurrent lifestyle modifications

- Response to the specific denial reason — Address whatever the insurer cited as the basis for denial

- Risk assessment — What happens to your health if treatment is not provided

MEDVi

Compounded tirzepatide from $279/mo

Keeping Your Coverage: Renewal and Continuation

Getting approved is step one. Staying approved is step two. Most initial Zepbound PAs last 6–8 months. After that, you'll need to reauthorize.

What insurers want to see at renewal

- Updated weight compared to baseline — most plans require at least 5% body weight loss

- Current BMI

- Documentation that treatment is ongoing and clinically beneficial

- Updated clinical notes showing continued diet and exercise

How to protect your coverage

- Start the renewal process 2–4 weeks before your current PA expires. Don't wait until the last day.

- Track your weight from day one. Document weigh-ins with your doctor or at home with dates.

- If you haven't hit 5% loss by renewal time, talk to your doctor early. Dose adjustments or documentation of other health improvements may satisfy the requirement.

- Watch for formulary changes. If your insurer modifies its formulary mid-year, you may need an entirely new PA — not just a renewal.

Renewal timeline to plan for

| Month | What to Do |

|---|---|

| Month 1 | Start tracking weight loss. Document weigh-ins with your doctor monthly if possible. |

| Month 3 | Check your progress against the 5% threshold. If you're not on track, discuss with your doctor. |

| Month 4–5 | Call your insurer to confirm: When does your PA expire? What documentation do they need for renewal? |

| Month 5 | Schedule a doctor appointment specifically for renewal documentation. Bring updated weight, lab results, and treatment notes. |

| Month 5–6 | Have your doctor submit the renewal PA 2–4 weeks before expiration. |

How Much Does Zepbound Cost? (With and Without Insurance)

Cost is inseparable from the PA conversation. If you're fighting for coverage, you need to know what you're fighting for — and what the alternatives look like if insurance doesn't come through.

| Scenario | Approximate Monthly Cost | Details |

|---|---|---|

| Commercial insurance with coverage + Savings Card | As low as $25/mo | Savings Card covers most of remaining copay (up to $100/mo savings). Max $1,300/yr. |

| Commercial insurance without coverage + Savings Card | ~$499–$650/mo (pens) | Savings Card provides up to $620/mo reduction on pens |

| LillyDirect self-pay — 2.5mg starting dose | $299/mo | Single-dose vials. No insurance needed. Price reduced December 2025. |

| LillyDirect self-pay — 5mg | $399/mo | Single-dose vials |

| LillyDirect self-pay — 7.5mg through 15mg (Journey Program) | $449/mo | Must refill within 45 days for this pricing. Available for vial or KwikPen. |

| Retail pharmacy (pens, no insurance) | ~$1,086/mo list price | GoodRx may offer some savings (~$995) |

| Compounded tirzepatide (telehealth) | ~$279–$499/mo | NOT FDA-approved. FDA has warned about risks with unapproved GLP-1 products. |

| Medicare Part D (weight loss) | Not covered | Statutory exclusion. OSA indication may be covered on some plans. |

For a complete breakdown, see our tirzepatide cost guide.

Can't Get Insurance Approval? Your Alternatives

If your PA was denied, your appeal didn't work, or your plan simply doesn't cover weight-loss medications — you're not out of options.

LillyDirect is Eli Lilly's direct-to-consumer pharmacy platform. No PA. No insurance required. You need a valid prescription.

- • 2.5mg (starting dose): $299/month

- • 5mg: $399/month

- • 7.5mg–15mg: $449/month (must refill within 45 days for Journey Program pricing)

- • Delivery: Free home delivery or Walmart pharmacy pickup (nationwide since October 2025)

45-day refill window: For doses 7.5mg and above, you must refill within 45 days of your previous delivery to maintain the $449/month Journey Program pricing. Miss that window and regular prices apply ($499–$699 depending on dose).

Compounded products marketed as tirzepatide are not FDA-approved, and the FDA has warned about risks with unapproved GLP-1 products — including dosing errors and quality concerns. If you're considering compounded options, understand they are not the same as FDA-approved Zepbound.

No PA. No insurance. Ships to your door. Typical costs range from $279–$499 per month depending on provider and dose.

Providers like MEDVi (tirzepatide starting at $279/month, partners with Belmar Pharma Solutions, LegitScript-certified) offer telehealth consultations and home delivery.

Important: Only use providers who partner with licensed, USP-compliant, accredited compounding pharmacies. The FDA has sent warning letters to more than 50 GLP-1 compounders.

Eli Lilly's patient assistance program provides free medications to qualifying patients based on financial need. Eligibility requirements and application details are available at lillycares.com. If you're uninsured and can't afford self-pay pricing, this is worth exploring.

If Zepbound specifically isn't covered, other GLP-1 medications might be:

- • Wegovy (semaglutide) — The most common alternative. Different mechanism (GLP-1 only, not dual GIP/GLP-1), but strong clinical data. Many insurers prefer it.

- • Mounjaro (tirzepatide) — Same active ingredient as Zepbound, but approved for type 2 diabetes. If you have T2D, your doctor may be able to prescribe Mounjaro, which may have different coverage.

- • Saxenda, Contrave, Qsymia — Older, less effective options, but more widely covered. May also satisfy step therapy requirements for a future Zepbound PA.

Real Patients, Real Results

Clinical trials tell one story. Real patients tell another. Here's what patient reviews say about the Zepbound experience:

“Started Zepbound in February… lost 65 lbs and went from a 42 waist to a 34.”

— User review posted on Drugs.com

“No side effects whatsoever (except lack of hunger!). Obesity is not a choice — it is genetics and a medical condition.”

— User review posted on Drugs.com

Individual results vary. These are user-submitted reviews and may not represent typical outcomes.

SURMOUNT-1 Clinical Trial Data

In the SURMOUNT-1 clinical trial (NEJM), patients taking the highest dose of Zepbound lost an average of 20.9% of their body weight over 72 weeks. Nine out of ten patients achieved at least 5% weight loss. Zepbound should be used alongside a reduced-calorie diet and increased physical activity.

How We Researched and Verified This Guide

• We reviewed PA criteria documents from 8 major insurers and PBMs

• All clinical criteria cross-referenced against FDA prescribing information and CMS guidance

• We analyzed real patient experiences from Reddit communities (r/Zepbound, r/GLP1_Drugs), Drugs.com, WebMD patient forums, and Bogleheads financial forums

• All insurer requirements are cited to published policy documents

• Pricing data verified against manufacturer sources (LillyDirect, Eli Lilly investor relations)

• “Last Verified” dates reflect when we actually re-checked each data point

• This guide is independently published. We're an affiliate site — not an insurer, not a pharmaceutical company, not a healthcare provider.

Frequently Asked Questions

Your 5-Step Action Plan

If you're staring at a “prior authorization required” message right now, here's what to do — in order:

Confirm your plan status.

Call your insurer. Ask: Is Zepbound on my formulary? Do I need PA? Is there step therapy? Or is weight-loss medication excluded entirely? This tells you which fight you're in.

Gather your evidence packet.

BMI documentation, comorbidity records, lifestyle modification proof, and prior medication history. Use the checklist above. The more complete your packet, the faster the process.

Prepare your doctor.

Bring your documentation to the appointment. Ask for a Letter of Medical Necessity. Make their job easy — a prepared patient gets a better submission.

Track the timeline.

Get the submission date, check your portal, follow up at 3–5 days. Respond immediately to any requests for additional information.

If denied — appeal.

Most appeals succeed (KFF data). Use the denial reason to build a targeted response. Request a peer-to-peer review. Escalate to external review if needed. Don't leave coverage on the table.

You've already done the hardest part — you decided to pursue treatment. The paperwork is just paperwork. And now you know exactly how to handle it.

Need to skip the PA process entirely?

Two options that don't require insurance approval:

- • Brand-name Zepbound via LillyDirect — starting at $299/month, no PA needed

- • Compounded tirzepatide via telehealth providers like MEDVi — starting at $279/month, ships to your door

Medical Disclaimer: This guide is for informational purposes only and does not constitute medical advice. Always consult your healthcare provider before starting, stopping, or changing any medication. Zepbound (tirzepatide) is a prescription medication with risks and contraindications — see full prescribing information at zepbound.lilly.com. This content is not affiliated with or endorsed by Eli Lilly and Company.