GLP-1 Providers That Provide Superbills: What We Verified in 2026

By Weight Loss Provider Guide Editorial Team · Last verified: · Next check:

Searching for GLP-1 providers that provide superbills? Here's the honest answer: very few publicly commit to issuing a true superbill — and most people looking for one don't actually need a superbill to get reimbursed. Of the major platforms we verified on April 23, 2026, Calibrate has the clearest public language confirming it will provide a superbill or itemized receipt for reimbursement. Mochi Health says it can prepare a "superbill receipt" — but that language is ambiguous and you'd need to confirm specific fields with their support before relying on it. Every other major provider we checked issues an itemized receipt at best.

Stick with us for 8 minutes. We built the one page on the internet that tells you exactly which document your plan needs, which provider publicly issues it, and where the others are quietly handing you a receipt and calling it a day.

Find Your Situation In One Line

| If your situation is… | Best first move | Why |

|---|---|---|

| You need a true superbill for out-of-network visit/program reimbursement | Calibrate (public language), or ask Mochi Health support | Explicit public superbill wording |

| Your HSA/FSA admin wants a receipt or a Letter of Medical Necessity | SHED (direct card) or MyStart Health (documentation pack) | Best-fit paperwork workflows |

| You want brand-name GLP-1 coverage (Wegovy/Zepbound/Ozempic/Foundayo) | Ro | Free coverage checker + insurance concierge |

| You're still figuring out which lane applies to you | Take our match quiz | We'll shortlist the 2–3 providers that actually fit |

Already know you're in row three — you want real insurance coverage for brand-name GLP-1s, not a reimbursement gamble? Skip the paperwork research.

For brand-name GLP-1 insurance coverage:

Check Your GLP-1 Insurance Coverage Free with RoFree checker. No obligation. If covered, Ro's concierge handles prior auth. Get started for $39, then as low as $74/month with annual plan paid upfront.

Which GLP-1 Providers That Provide Superbills Are Worth Knowing About?

Why this distinction matters

When someone on Reddit says "just request a superbill and submit it," they're usually pulling advice from therapy-billing threads. Therapists often do issue true superbills because therapy reimbursement through out-of-network PPO benefits is a developed use case. GLP-1 telehealth is different. Most of these platforms were built as cash-pay subscription models. Their billing systems generate subscription receipts — not coded medical claim documents. That's not a flaw. It's a business model choice. Subscription receipts are faster to generate, cleaner to dispute, and work perfectly for HSA/FSA documentation. But they will usually get your out-of-network insurance claim rejected.

The three providers with the clearest public paperwork language

Calibrate

True superbill — public confirmationOn its own FSA page, Calibrate states its team can provide a superbill or itemized receipt for reimbursement if FSA funds don't cover the full membership balance. Calibrate's membership is $199/month, and brand-name GLP-1 medication is billed separately through insurance or pharmacy. Best fit: PPO members with out-of-network medical benefits who want coaching-heavy care and brand-name GLP-1s.

Calibrate is not one of our affiliate partners — we don't have a tracked sign-up link for them. We're telling you about them anyway because the goal of this page is to end your search.

Mochi Health

Superbill-adjacent — verify fields with supportMochi's insurance FAQ says support can prepare a "superbill receipt" to submit for reimbursement. Treat this as superbill-adjacent until you confirm the specific fields with their support team. Membership starts at $79/month (or $69/month with qualifying insurance under their Wellness Plus plan), with medication billed separately. Mochi's Wellness Plus tier is in-network with qualifying commercial plans.

Sesame Care

Conflicting public language — verify before enrollingSesame's weight-loss program page says its support team can provide an itemized bill for HSA/FSA submission. But Sesame's general service FAQ states the booking confirmation is the receipt and that Sesame doesn't provide additional paperwork. We've flagged this contradiction — confirm with Sesame support which policy applies to your subscription tier before relying on either page.

Decision Resolution Point

If you specifically need a true superbill for out-of-network medical reimbursement — you have PPO or POS coverage, you've confirmed out-of-network benefits exist, and you want coaching + brand-name GLP-1s — Calibrate is where the public language is clearest. If you want a paperwork-capable path through a provider we do work with, the next section tells you where your money is.

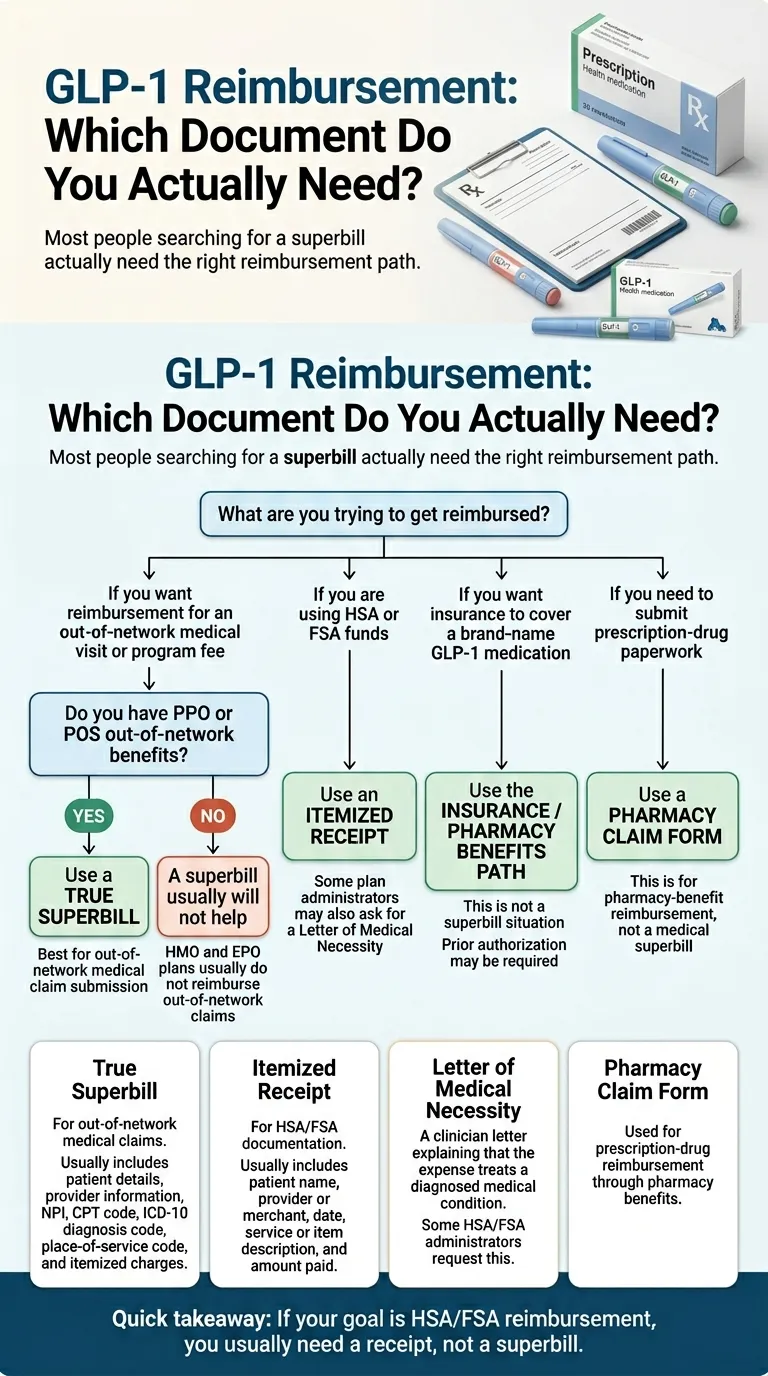

Do You Actually Need a Superbill, or Is It a Receipt, an LMN, or a Pharmacy Claim Form?

The damaging admission: We don't benefit from telling you this. It would be easier to say "here are the best superbill providers, click here" and collect commissions. But most people landing on this page Googled "superbill" because someone told them to. Half of them don't need one. If we push a superbill lane when the reader actually needs an LMN, our recommendation fails. So let's do it right.

The four-document reimbursement map

| Document | Required fields | What it does | Who issues it |

|---|---|---|---|

| True superbill | Patient info, date of service, provider NPI, CPT code, ICD-10 code, place-of-service code, itemized charges, EIN | Lets you submit an out-of-network medical claim to a PPO/POS/indemnity insurer | Providers with billing built for out-of-network claims (therapy practices, Calibrate, Mochi) |

| Itemized receipt | Date, provider name, service description, amount paid, patient name | Satisfies HSA/FSA administrators for qualified medical expense documentation under IRS Publication 502 | Nearly every GLP-1 telehealth provider (downloadable from Orders tab or via support) |

| Letter of Medical Necessity (LMN) | Clinician statement confirming the expense treats a diagnosed medical condition | Unlocks HSA/FSA reimbursement when plan admin wants more than a receipt; sometimes required for weight-loss expenses specifically | Any licensed clinician; many GLP-1 platforms provide on request |

| Pharmacy claim form | NDC, quantity, days supply, pharmacy NCPDP number, rendering pharmacy info | Lets you submit a prescription medication claim to your pharmacy benefit manager | The dispensing pharmacy (NovoCare, Costco, local pharmacy, compounding pharmacy) |

How to know which lane you're in

PPO/POS with out-of-network benefits + medical visit reimbursement wanted

True superbill

HSA or FSA funds available + medication or visit cost being paid

Itemized receipt (possibly plus LMN)

Plan admin already asked for "proof of medical necessity"

LMN

You want your Wegovy/Zepbound/Ozempic covered by insurance formulary

Not reimbursement — insurance-first path; use Ro or any pharmacy that handles prior authorization

Still unsure which lane fits your plan?

Take our free GLP-1 provider match quizFive quick questions. We'll shortlist the 2–3 providers that actually fit — including the paperwork workflow you need. No medical info required.

The Full Provider Matrix: 12 Major GLP-1 Providers Verified

| Provider | True superbill? | Itemized receipt? | LMN stated publicly? | HSA/FSA at checkout? | Handles prior auth? | Verified note |

|---|---|---|---|---|---|---|

| Calibrate | ✅ Yes | ✅ Yes | ⚠️ Confirm with support | ✅ Yes | ✅ Insurance navigation team | Clear public superbill language — clearest in GLP-1 telehealth |

| Mochi Health | ⚠️ "Superbill receipt" (ambiguous) | ✅ Yes | ⚠️ Confirm with support | ✅ Yes | ✅ Prior-auth support | Verify specific fields (NPI, CPT, ICD-10) with Mochi before enrolling |

| Sesame Care | ⚠️ Contradictory language | ✅ Yes (weight-loss support) | ⚠️ Confirm before enrolling | ✅ Yes | ✅ Provider-driven PA | Confirm paperwork tier with support before enrolling |

| Ro | ❌ Detailed receipt only | ✅ Yes (Orders tab) | ⚠️ Needs verification | ❌ Reimburse yourself | ✅ Dedicated insurance concierge | Ro's value is insurance coverage, not superbill reimbursement |

| SHED | ❌ Receipt only | ✅ Detailed portal receipt | ⚠️ Confirm on request | ✅ Yes (direct Rx payment) | ❌ No | Strong HSA/FSA workflow; optimized for direct reimbursement |

| MyStart Health | ❌ Not advertised | ✅ Documentation Pack — itemized invoice with Rx details + proof of payment | ⚠️ Confirm with support | ✅ Yes | ❌ No | Strong documentation workflow; no public superbill promise |

| Noom Med | ❌ Not a superbill | ✅ Subscription receipt + LMN | ✅ Publicly stated | ❌ Reimburse yourself | ❌ No (pharmacy separately) | LMN available; reimbursement-first model |

| WeightWatchers | ❌ Not a superbill | ✅ Membership receipt | ✅ Plan-dependent, publicly stated | ❌ Not at signup | ❌ No | Verified on WW FSA/HSA page |

| Hims | ❌ Receipt only | ✅ Downloadable receipt (Orders tab) | ⚠️ Not publicly stated | ⚠️ Sometimes (extra steps) | ❌ No | Reimbursement-first model; detailed receipt works for most HSA/FSA |

| Hers | ❌ Receipt only | ✅ Downloadable receipt (Orders tab) | ⚠️ Not publicly stated | ⚠️ Sometimes (extra steps) | ❌ No | Same workflow as Hims; detailed receipt works for most HSA/FSA |

| Embody | ❌ No public language | ✅ HSA/FSA accepted | ⚠️ Not publicly stated | ✅ Yes | ❌ No | Cash-pay, no insurance; HSA/FSA accepted; low first-month pricing — confirm paperwork with support |

| MEDVi | ❌ Needs verification | ⚠️ Not confirmed publicly | ⚠️ Needs verification | ⚠️ Needs verification | ❌ No | Feb 2026 FDA warning letter for marketing claims — factor into assessment |

All entries verified against public pages on April 23, 2026. Pricing and policies change frequently — verify before enrolling. Rows with "Needs Verification" or ⚠️ should be confirmed with provider support before relying on them.

About MEDVi: February 2026 FDA Warning Letter

MEDVi has a wide medication menu, competitive pricing, and has served a large patient base. In February 2026, the FDA issued MEDVi a warning letter regarding certain marketing claims about its compounded GLP-1 medications. If FDA enforcement context matters to you when choosing a paperwork-sensitive provider, consider alternatives: SHED, Embody, or MyStart Health.

For brand-name GLP-1 insurance coverage:

Check Your GLP-1 Insurance Coverage Free with RoIf the honest truth above has redirected your priority toward actually getting insurance to cover brand-name GLP-1s, the path forward is clear. Ro's free coverage checker runs your plan against Wegovy pen, Wegovy pill, Zepbound KwikPen, Ozempic, and Foundayo.

When Is a Superbill Actually Worth Chasing? The Honest Reality Check

You have PPO/POS out-of-network benefits, your plan covers GLP-1s for weight loss, and your deductible is close to met

This is the best case and it's rarer than people think. KFF's 2025 Employer Health Benefits Survey found that among firms with 200+ workers, 19% said their largest plan covered GLP-1s used primarily for weight loss in 2025 — still a minority. If you are in this group, a true superbill is worth getting. Expected reimbursement: a portion of the plan's allowed amount after deductible, typically on the clinician visit portion. Best-fit providers: Calibrate, Mochi Health, Sesame Care (with paperwork tier confirmed).

✅ Superbill is worth it

You have PPO/POS out-of-network benefits but your plan excludes GLP-1s for weight loss

Much more common. A superbill may still recover partial reimbursement on the clinician visit itself (under CPT codes like 99213 or 99214), even if the medication is excluded. A recovered partial reimbursement on a $75–$199 monthly visit fee, compounded over twelve months, can add up to a few hundred dollars — not life-changing, but real. Plan for the possibility of a first-pass denial and a correction-and-resubmit cycle.

⚠️ Partial recovery possible — set realistic expectations

You have HMO/EPO, no out-of-network benefits, or a plan that doesn't pay on out-of-network weight-loss claims

Stop. The superbill chase is not for you. Pay with HSA or FSA funds (pre-tax dollars — guaranteed savings, not theoretical), get an itemized receipt (universal — every provider issues one), get a Letter of Medical Necessity if your plan admin requests it, and move on. That is a cleaner, lower-friction, higher-reliability savings strategy than any superbill.

❌ Don't chase the superbill — use HSA/FSA

You have Medicare or Medicaid

Medicare Part D generally doesn't cover weight-loss GLP-1s (with some narrow exceptions). CMS is launching the Medicare GLP-1 Bridge on July 1, 2026, which will provide eligible Medicare Part D beneficiaries access to certain GLP-1 drugs at a $50 copay through December 31, 2027 using BIN/PCN 028918/MEDDGLP1BR. If you're on Medicare, focus on Bridge enrollment rather than submitting superbills. Most state Medicaid programs don't have out-of-network reimbursement benefits in the way commercial PPOs do.

❌ Superbills don't apply — focus on Bridge enrollment or formulary coverage

If you've just realized you're in Scenario 3 — HSA/FSA is your real savings vehicle — pick a provider that accepts your HSA/FSA card at checkout.

How Does HSA/FSA Reimbursement Actually Work for GLP-1s?

When you actually need a Letter of Medical Necessity

Most HSA plan administrators don't ask for an LMN for prescription medications — the prescription itself is medical necessity documentation. FSA administrators are stricter and sometimes request one, especially for weight-management expenses not clearly tied to a diagnosed condition on the receipt. An LMN is a short letter from your prescribing clinician stating that the expense treats a specific diagnosed medical condition (e.g., E66.01 morbid obesity, E11.9 type 2 diabetes).

Providers with LMN language on their public pages include Noom (subscription reimbursement FAQ explicitly notes an LMN is required) and WeightWatchers (FSA/HSA page notes plan-dependent LMN requirement). For a cash-pay compounded option that advertises HSA/FSA acceptance, Embody works through licensed clinicians who can document medical necessity on request — confirm the specifics during intake.

The tax savings math that actually matters

| GLP-1 program cost | Annual total | Pre-tax savings (22% bracket) | Pre-tax savings (32% bracket) |

|---|---|---|---|

| $229/month compounded semaglutide | $2,748/year | ~$604/year | ~$879/year |

| $349/month compounded tirzepatide | $4,188/year | ~$921/year | ~$1,340/year |

No denial risk. No filing window. For most readers on a compounded path, this is the win to focus on — not the superbill lottery.

This is the #1 failure mode in the GLP-1 HSA/FSA space — and it's almost never an eligibility problem. HSA cards sometimes get declined because the merchant category code (MCC) doesn't automatically trigger medical-expense approval. Fix: pay with your regular card, keep the itemized receipt, and submit for HSA reimbursement through your administrator's portal. Tax savings are identical.

FSA contributions are generally use-it-or-lose-it within the plan year. If you contribute $3,000 expecting to use GLP-1s all twelve months and you stop treatment in June, you can forfeit the remaining balance. HSA contributions roll over and grow tax-free indefinitely — much lower risk.

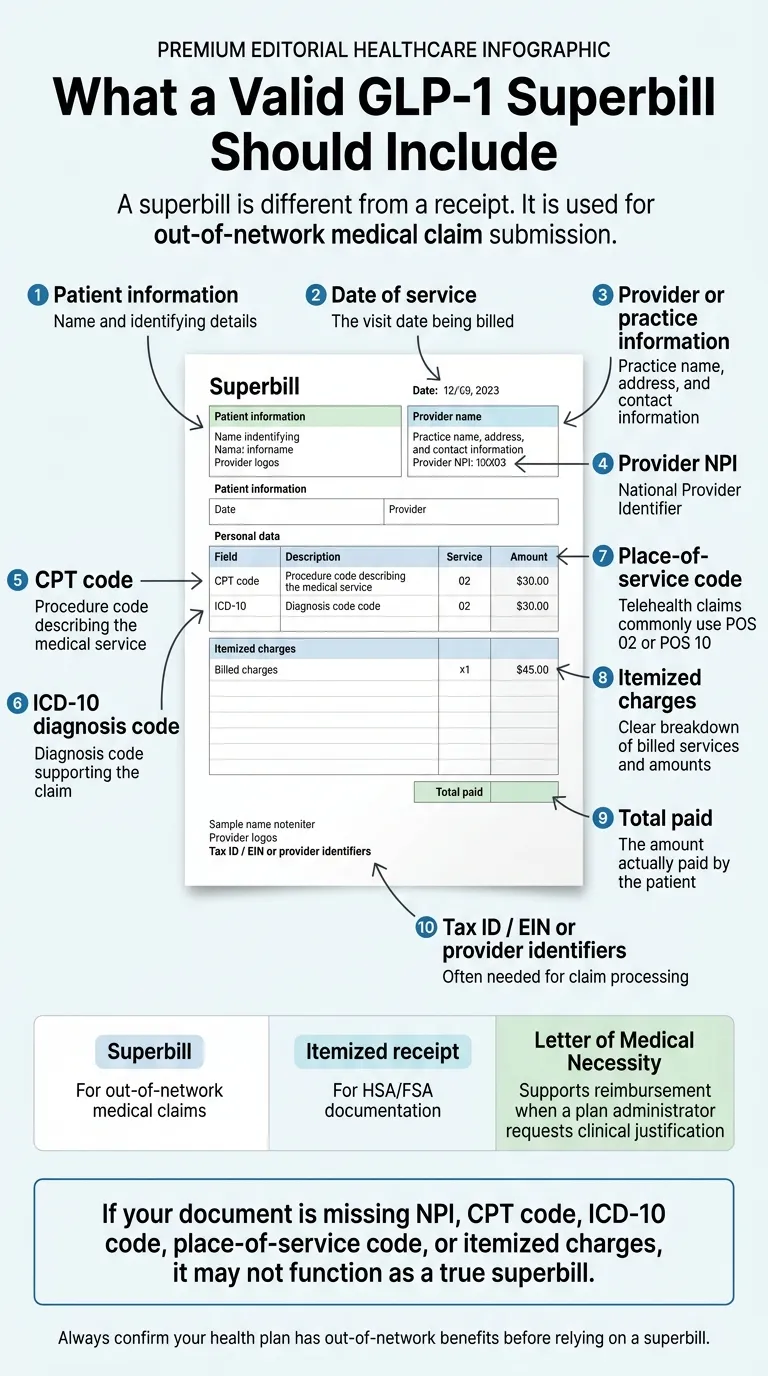

What Has to Be on a Valid GLP-1 Superbill

Required fields at a glance

| # | Field | What it is | Why it matters |

|---|---|---|---|

| 1 | Patient information | Name, DOB, address, insurance member ID | Required for insurer to identify beneficiary |

| 2 | Date of service | The visit date being billed | Required for timely-filing compliance |

| 3 | Provider NPI | 10-digit National Provider Identifier | Insurers validate the rendering provider here |

| 4 | CPT code | 99213 or 99214 for established outpatient telehealth visit | Describes the service type; required for claim processing |

| 5 | ICD-10 diagnosis code | E66.01, E66.9, E11.9, Z68.## (BMI), etc. | Documents medical necessity; wrong codes = denial |

| 6 | Place-of-service code | POS 02 (telehealth, not patient's home) or POS 10 (telehealth in patient's home) | Telehealth-specific; affects reimbursement rates |

| 7 | Telehealth modifier | Modifier 95 (synchronous audiovisual) — payer-specific | Some payers require this for telehealth claims |

| 8 | Itemized charges | Clear line-item breakdown of billed services and amounts | Needed for insurer to verify each charge |

| 9 | Total paid | Amount actually paid by patient | Determines the maximum reimbursement eligible |

| 10 | Tax ID / EIN | Provider or practice tax identifier | Often required for claim processing |

Common GLP-1 coding examples

ICD-10 codes likely to appear

| E66.9 | Obesity, unspecified |

| E66.01 | Morbid (severe) obesity due to excess calories |

| E66.3 | Overweight |

| E11.9 | Type 2 diabetes without complications |

| Z68.30–Z68.54 | BMI codes (specifies severity) |

| Z79.899 | Long-term drug therapy (non-insulin) |

| Z79.85 | Long-term use of injectable non-insulin antidiabetic drug |

CPT codes likely to appear

| 99213 | Established patient outpatient, low-moderate complexity (~15 min) |

| 99214 | Established patient outpatient, moderate complexity (~25 min) |

| Modifier 95 | Synchronous telehealth via audiovisual real-time link |

| G0447 | Face-to-face obesity behavioral counseling (if applicable) |

Exact coding decisions are your provider's, not yours. Your provider selects codes based on visit content and documentation.

Does Compounded vs. Brand-Name Change the Reimbursement Path?

Brand-name GLP-1 reimbursement path

For Wegovy, Zepbound, Ozempic, Mounjaro, or Foundayo:

- Your telehealth provider writes the prescription

- The prescription goes to a pharmacy (local, NovoCare, LillyDirect, Ro's partners, or Costco)

- The pharmacy runs the claim through your insurance pharmacy benefit manager

- If covered, you pay a copay; if prior auth required, provider or pharmacy submits documentation

- If denied, you pay cash — manufacturer savings programs come into play

The superbill plays no role in this flow. It's a pharmacy benefits conversation.

Compounded GLP-1 reimbursement path

For compounded semaglutide or tirzepatide (Embody, SHED, MyStart, Mochi, Hims, Hers, most others):

- Your telehealth provider writes the prescription

- The prescription goes to a compounding pharmacy (503A or 503B)

- The pharmacy ships medication directly to you; you pay cash

- Commercial insurance almost never reimburses compounded medications

- HSA/FSA funds reimburse both the visit and medication when documented properly

If your goal is insurance paying for the medication itself, you need brand-name on formulary. Compounded paths are HSA/FSA paths.

For brand-name GLP-1 insurance coverage:

Check Your GLP-1 Insurance Coverage Free with RoRo's free coverage checker runs your plan against every FDA-approved GLP-1. If prior authorization is required, Ro's dedicated concierge handles the paperwork. Get started for $39, then as low as $74/month with annual plan paid upfront.

How Do You Submit a GLP-1 Superbill? (Step by Step)

The six-step submission workflow

- Request the superbill from your provider — monthly cadence is most common; some providers issue on-demand

- Log into your insurance member portal — locate the "submit out-of-network claim" or "claim submission" section (wording varies)

- Download and complete your insurer's out-of-network claim form — if required (some insurers treat the superbill as the claim itself)

- Upload or attach the superbill — along with any completed claim form; verify all fields match (patient info, policy number, total charges)

- Submit and save copies of everything — both the superbill and the submission confirmation — for your records

- Watch for your EOB — if denied for a fixable reason, correct and resubmit rather than giving up

Denial reasons worth knowing in advance

| Denial reason | Fix | Fixable? |

|---|---|---|

| Missing NPI | Ask provider for corrected superbill and resubmit | ✅ Yes |

| ICD-10 code doesn't support medical necessity | Ask provider to add stronger codes (E66.01 often documents better than E66.9 unspecified) | ✅ Yes |

| Missing telehealth modifier | Check your insurer's telehealth policy; request corrected superbill with modifier 95 | ✅ Usually |

| Out-of-network benefit not active | Call member services to confirm OON benefits exist before resubmitting | ❌ No — wrong lane |

| GLP-1 / weight loss not a covered benefit | Pivot to HSA/FSA — this denial is not fixable through superbills | ❌ No — wrong lane |

Commercial plans each have their own timely-filing deadline for out-of-network claims — these vary significantly between insurers and plans within the same insurer. Check your plan's Summary of Benefits and Coverage or call the member services number on your insurance card before stockpiling superbills — missing the window kills the claim entirely.

Why Do GLP-1 Reimbursement Claims Get Denied?

Subscription receipt submitted in place of an itemized medical invoice

Many GLP-1 platforms bill as a monthly subscription. That line item — "Monthly Program Fee: $299" — doesn't give the plan admin enough detail to approve reimbursement. Request a detailed invoice with the clinician visit separated from the medication and any other services.

No Letter of Medical Necessity when the plan admin wants one

Especially common with stricter FSA administrators. If the first response is "please provide documentation of medical necessity," don't argue — get the LMN from your provider and resubmit.

Pharmacy-benefit question submitted as a medical claim

If you're trying to reimburse the medication through a superbill, most plans will deny because compounded medications aren't on their formulary and brand-name medications should be handled through the pharmacy benefit manager, not out-of-network medical claims.

No out-of-network benefit on the plan

HMO and EPO plans typically don't pay on out-of-network claims. This denial isn't fixable — you're in the wrong lane.

GLP-1s explicitly excluded for weight loss on the formulary

Some employer plans added exclusion language in 2024–2025 as GLP-1 spend exploded. Check your plan document.

Who Should Skip This Whole Strategy (And What To Do Instead)

If you have an HMO or EPO plan

Why to skip: Your plan almost certainly doesn't pay on out-of-network claims.

Do this instead: Focus on HSA/FSA reimbursement (the universal savings path) or find a GLP-1 provider in your plan's network. Mochi Health's Wellness Plus tier operates in-network with qualifying commercial plans, which is rare in the GLP-1 telehealth space.

If you want insurance to cover a brand-name GLP-1 you haven't started yet

Why to skip: Don't pay out of pocket and chase reimbursement.

Do this instead: Run the coverage check first — don't pay out of pocket and chase reimbursement.

For brand-name GLP-1 insurance coverage:

Check Your GLP-1 Insurance Coverage Free with RoIf you're on a compounded medication and expecting medication reimbursement

Why to skip: Commercial insurance almost never reimburses compounded medications — plan formularies exclude them categorically.

Do this instead: Your path is HSA/FSA reimbursement on the full cost. Pick a provider with a clean HSA/FSA workflow.

If you're on Medicare or Medicaid

Why to skip: Superbills typically don't apply.

Do this instead: Focus on the Medicare GLP-1 Bridge (launching July 1, 2026 at $50 copay, BIN/PCN 028918/MEDDGLP1BR) or formulary coverage if your state Medicaid covers GLP-1s.

Our Verification Methodology

What we verified for every provider

- Does the provider publicly promise a superbill, itemized bill, or LMN?

- Is HSA/FSA card payment accepted directly at checkout?

- Does the provider handle prior authorization for brand-name GLP-1s?

- Does the provider publish conflicting language on different pages?

- What medication lanes does the provider serve?

What we did not do

- We did not contact each provider's support team beyond public pages

- We did not verify individual insurance plan reimbursement outcomes

- We did not substitute for a tax professional's advice on HSA/FSA eligibility

Verification snapshot — April 23, 2026

✓ 12 major GLP-1 telehealth providers reviewed

✓ Each provider's own pricing/insurance/FAQ page checked on 2026-04-23

✓ Contradictions between a provider's own pages flagged

✓ Rules-layer sources: IRS Pub 502, FSAFEDS, CMS Bridge, HHS, FDA, KFF

✓ MEDVi February 2026 warning letter cited honestly

✓ All pricing flagged as "verify before enrolling" due to change frequency

✓ [NEEDS VERIFICATION] tags applied where public data was incomplete

Frequently Asked Questions About GLP-1 Superbills

Final Recommendation: What To Do In The Next 5 Minutes

You came to this page looking for a list of GLP-1 providers that provide superbills. Here's the best thing we can do for you before you leave:

- Figure out your actual lane. Out-of-network PPO reimbursement, HSA/FSA reimbursement, or brand-name insurance coverage? Different document, different provider.

- If it's out-of-network PPO reimbursement and you've confirmed OON medical benefits exist — Calibrate has the clearest public superbill language. Mochi Health is viable if you confirm fields with their support team.

- If it's HSA/FSA reimbursement, you don't need a superbill — you need a clean itemized receipt (and possibly an LMN). Pick a provider with a direct HSA/FSA card workflow.

- If it's brand-name insurance coverage for Wegovy, Zepbound, Ozempic, or Foundayo — skip the superbill entirely. Use Ro's free coverage checker.

- If you're still not sure which lane applies to your plan, take our quiz.

For brand-name insurance coverage seekers:

Check Your GLP-1 Insurance Coverage Free with RoRo's concierge fights prior auth. Get started for $39, then as low as $74/month with annual plan paid upfront.

For HSA/FSA-funded cash-pay compounded users:

For anyone still figuring out the lane:

Take the free GLP-1 provider match quizWe'll shortlist the 2–3 providers that actually fit — including the paperwork workflow you need.

Compliance and Safety Notes

Compounded GLP-1 medications are prepared by licensed compounding pharmacies and are not FDA-approved. They are not reviewed by the FDA for safety, effectiveness, or quality in the same way brand-name products are. All GLP-1 medications require a prescription from a licensed clinician. Serious warnings include risk of medullary thyroid carcinoma (MTC) and multiple endocrine neoplasia type 2 (MEN2) contraindications, pancreatitis, gallbladder disease, kidney function concerns, and gastrointestinal side effects. Consult your healthcare provider before starting treatment.

This page is educational and does not constitute medical, tax, or legal advice. IRS Publication 502 governs HSA/FSA eligibility; consult a tax professional for guidance on your specific situation. Insurance reimbursement outcomes depend on your specific plan and administrator — individual results vary. Pricing shown was verified on April 23, 2026 and is subject to change. Verify current pricing and policies on each provider's website before enrolling.

Verification Log

Last full page review:

| Provider | Verified | Source |

|---|---|---|

| Calibrate | 2026-04-23 | joincalibrate.com/resources/fsa-flexible-spending-accounts |

| Mochi Health | 2026-04-23 | joinmochi.com/blogs/mochi-insurance-cost-coverage-breakdown |

| Sesame Care | 2026-04-23 | sesamecare.com/service/online-weight-loss-program + general Sesame FAQ (contradiction flagged) |

| Ro | 2026-04-23 | ro.co/weight-loss/pricing/ + ro.co/faq/cost-pricing-services/ + ro.co/weight-loss/insurance/ |

| SHED | 2026-04-23 | tryshed.com/resources/help/fsa-hsa |

| MyStart Health | 2026-04-23 | mystarthealth.com/hsa-fsa/ |

| Noom Med | 2026-04-23 | noom.com/support FAQ (HSA/FSA subscription billing) |

| WeightWatchers | 2026-04-23 | weightwatchers.com/us/fsa-hsa |

| Hims | 2026-04-23 | hims.com/weight-loss/fsa-hsa + current weight-loss medication pages |

| Hers | 2026-04-23 | forhers.com/weight-loss/fsa-hsa + current weight-loss medication pages |

| Embody | 2026-04-23 | joinem.co FAQ + treatment pages + public pricing |

| MEDVi | 2026-04-23 | MEDVi public FAQ pages + FDA warning letter index (Feb 2026) |

Next scheduled review: Monthly for provider pricing and paperwork policy; quarterly for rules-layer sources; event-driven for FDA enforcement updates.

Authored by the Weight Loss Provider Guide editorial team. Weight Loss Provider Guide is an independent comparison resource for GLP-1 telehealth providers. We earn commissions when readers sign up with providers via our affiliate links. Our rankings, matrix entries, and editorial recommendations reflect verified public policies and editorial judgment on reader fit — not commission rates.

Last verified: April 23, 2026. Next scheduled verification: May 23, 2026 (or immediately upon any material change).