GLP-1 Providers That Accept Insurance: 10 Verified Picks (April 2026)

Real prior auth help, real total monthly costs, real denial backups — verified from official provider pages.

The fastest way to waste a month and a few hundred dollars is to sign up for a GLP-1 telehealth program that says it "accepts insurance" — only to find out at week three that it meant something completely different from what you assumed.

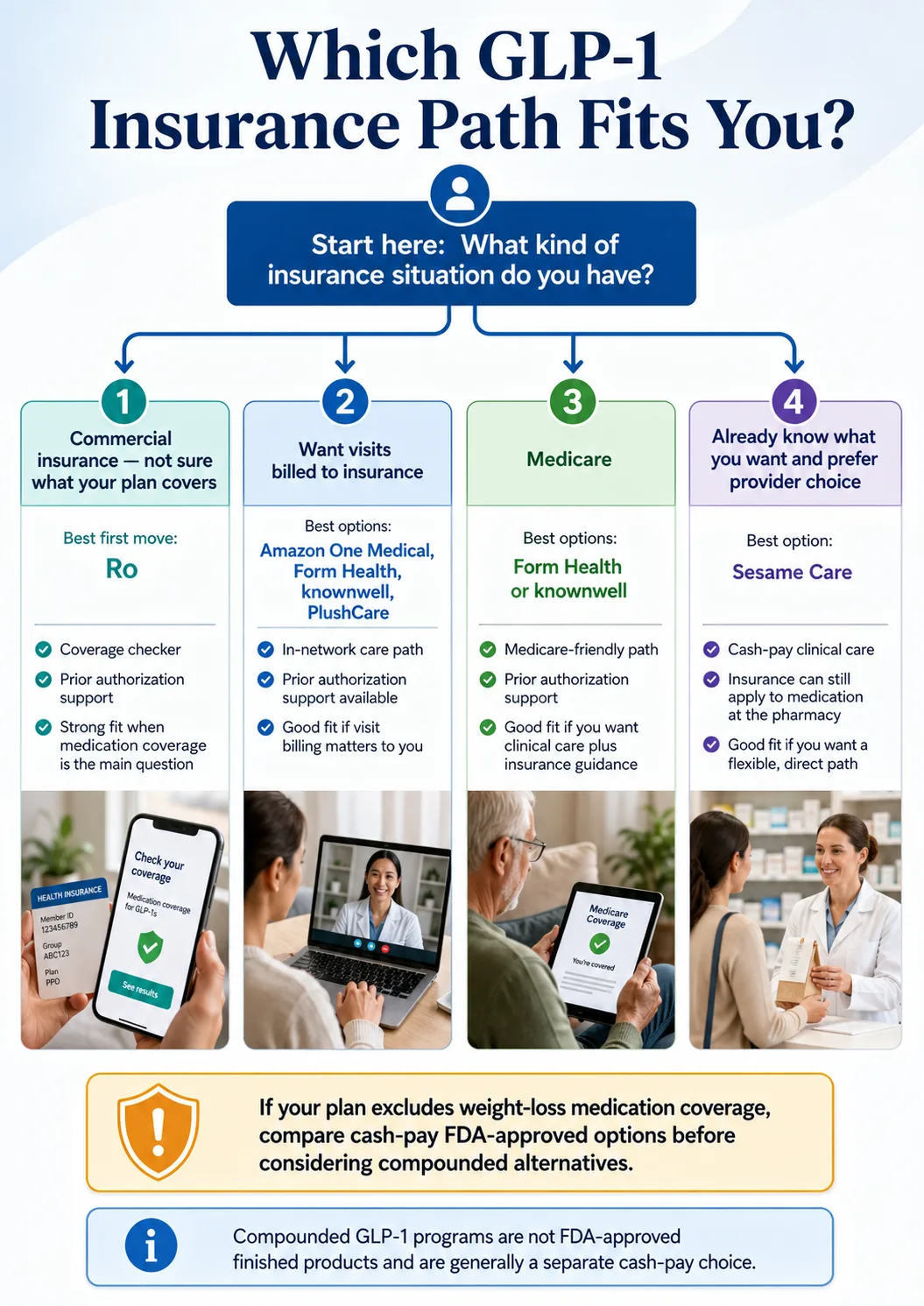

The best GLP-1 providers that accept insurance for most commercially insured adults start with Ro. Ro's free GLP-1 Insurance Coverage Checker calls your insurer for you, returns a personalized coverage report by email, and — if you decide to enroll — Ro's concierge team submits prior authorization paperwork on your behalf. If your plan covers a GLP-1, your medication cost can drop to a copay. But "accepts insurance" means four different things in this category, and the wrong assumption costs you weeks.

Best First Move for Commercial Insurance

Ro's free coverage checker calls your insurer and emails you a personalized report. No prescription required. No commitment.

Check Your GLP-1 Coverage with Ro — Free →Quick verdict: 10 GLP-1 providers that accept insurance, by use case

| Provider | Best for | Insurance model | Membership | PA help | Medicare? |

|---|---|---|---|---|---|

| Ro ⭐ | Commercial insurance, fastest coverage answer | Cash-pay membership + medication insurance concierge | $39 first month, then $149/mo (or $74/mo annual prepay) | ✅ Submits PA + fights for coverage | ❌ Not coordinated |

| Amazon One Medical | Insurance-billed visits + Amazon Pharmacy fulfillment | Visits billed to insurance + PA support | Membership not required for GLP-1 program visit | ✅ Yes (scheduled program only) | ✅ Original Medicare, Medigap, select Medicare Advantage |

| Form Health | Medicare beneficiaries who want obesity-medicine specialists | Visits billed to insurance + medication PA | Self-pay $299/mo if insurance doesn't cover | ✅ Yes | ✅ Yes |

| knownwell | Commercial + Medicare nationwide telehealth | Visits billed to insurance + medication PA | Cash-pay $299 first visit, $149 follow-up | ✅ Yes (80% PA approval rate published) | ✅ Yes |

| PlushCare | In-network virtual PCP + local pharmacy pickup | Visits billed to insurance + medication PA | $19.99/mo + visit copay | ✅ Yes (PA review 7–14 days) | ⚠️ Medicare Part B no longer accepted (1/1/26) |

| WW Clinic Med+ | Behavioral coaching + insurance coordinator | Cash-pay membership + medication insurance support | $25/mo first 2 months, $74/mo (12-mo plan) | ✅ Yes | ⚠️ Limited |

| Sesame Care | Branded provider choice + Costco self-pay pricing | Cash-pay marketplace + ongoing subscription | Success by Sesame from $59/mo annual; per-visit also available | Provider-dependent | ⚠️ Limited |

| Found | Free coverage checker + flexible insurance/cash hybrid | Coverage checker + medication PA when applicable | Plan-based; cash-pay options if uninsured | ✅ Yes | Carrier-dependent |

| Mochi Health | Insurance for branded only; also offers compounded cash-pay | $79/mo subscription + PA support for prescribed medication | $79/mo subscription | ✅ Yes (for prescribed meds) | Verify with Mochi |

| Hims / Hers | Familiar consumer brand, mostly cash-pay | Cash-pay membership + Novo Nordisk partnership pricing | $39 first month, then $149/mo | Limited | ❌ |

Last verified April 30, 2026. Pricing and coverage policies change — confirm on each provider's site before enrolling. Government insurance beneficiaries generally aren't eligible for manufacturer savings cards. State availability varies.

Run Ro's Free GLP-1 Insurance Coverage Check →

Ro's specialists call your insurance company and email you a personalized coverage report. Free. No prescription required. No commitment.

Check My Coverage with Ro — Free →What "accepts insurance" actually means (and why most pages skip this)

This is the single most important distinction in this entire category, and it's the reason readers waste weeks picking the wrong provider.

The four meanings of "accepts insurance"

Meaning #1 — In-network for visits only.

The provider is in-network with your insurer, so your video visits, follow-ups, and sometimes labs run through your medical benefit. You pay your normal copay or deductible. The medication is a separate fight. Pure examples are rare in GLP-1 telehealth — most providers in this lane also offer PA support.

Meaning #2 — Cash-pay membership + medication concierge.

The membership is not billed to insurance. But the provider has a dedicated team whose job is to check your benefits, submit prior authorization for your branded medication, and fight for coverage if it's denied. Your medication runs through your pharmacy benefit at copay rates if approved. Examples: Ro, WeightWatchers Clinic Med+, Mochi Health.

Meaning #3 — Both.

The provider bills medical visits in-network and their team handles medication prior authorization. This is the fullest insurance integration. Examples: Amazon One Medical, Form Health, knownwell, PlushCare, Found.

Meaning #4 — Cash-pay only.

"Insurance" on the marketing site usually refers to HSA/FSA card acceptance, manufacturer savings programs, or what to do if you have insurance but want to skip the wait. Visits and medication are paid out of pocket. Examples: Hims, Hers, Walgreens Weight Management, compounded providers.

Use Ro's free coverage check to find out what your specific plan actually covers before you pay for any program.

Use Ro's Free Coverage Check →Best for commercial insurance. Free report by email. No prescription required.

Ro: the best first move for commercial insurance

We start with Ro for one specific reason: it removes the most expensive uncertainty in GLP-1 telehealth — "will my plan actually cover this?" — without making you commit to a program first.

How Ro's insurance flow actually works

- Free coverage check (no prescription needed). You enter your insurance card details. Ro's specialists call your insurer to verify GLP-1 benefits. You get a personalized coverage report by email — including which medications are covered, whether prior authorization is required, and an estimated copay.

- You decide. Coverage report in hand, you choose: enroll with Ro, take it to a different provider, or pause. Either way, you now have information you didn't have before.

- If you enroll, Ro's concierge takes over. Their team handles benefits verification, prior authorization submission, and works to resubmit your PA if appropriate when there are issues. Ro states this process typically takes about 2–3 weeks.

- Approved → prescription routes to your pharmacy at copay rates. Cash-pay fallback if denied: Ro states it matches LillyDirect, NovoCare, and TrumpRx pricing on FDA-approved brand-name medication.

Real total monthly cost on Ro with insurance (worked example)

| Scenario | Month 1 | Month 2+ (annual prepay) | Month 2+ (monthly billing) |

|---|---|---|---|

| Plan covers Zepbound, $25 copay | $39 + $25 = $64 | $74 + $25 = $99/mo | $149 + $25 = $174/mo |

| Plan covers Wegovy with PA, $50 copay | $39 + $50 = $89 | $74 + $50 = $124/mo | $149 + $50 = $199/mo |

| Plan denies — Zepbound KwikPen cash-pay (Ro manufacturer match) | $39 + $299 = $338 | $74 + $399–$449 = $473–$523/mo | $149 + $399–$449 = $548–$598/mo |

In Ro's published 2025 GLP-1 Insurance Coverage Checker report, half of covered patients had a copay of $50/month or less. Verified April 30, 2026 (ro.co/weight-loss/coverage-checker-report).

The honest admission about Ro

Ro doesn't bill your insurance for visits. Ro doesn't accept HSA or FSA cards. Ro can't coordinate Medicare or other government insurance plans. If those are dealbreakers for you, Ro is the wrong provider — and we'll route you to better fits below. PlushCare bills visits in-network. Form Health and knownwell take Medicare. Several compounded providers accept HSA/FSA.

But here's the pivot: because Ro built the entire company around the medication insurance fight specifically — not visit billing — they have the deepest concierge team in the category and the cleanest published process. Visits are a $30 line item. Medication is a $900 line item. Ro chose the harder problem on purpose.

Who Ro is not for

- Medicare or Medicaid beneficiaries → see the Medicare and Medicaid section below

- You only want compounded medication → see our best self-pay GLP-1 programs guide

- You need HSA or FSA payment → check Form Health, knownwell, PlushCare, or Mochi below

- You want visits billed to insurance specifically → Amazon One Medical, Form Health, knownwell, PlushCare, or Found are better fits

Free personalized report by email. Ro's specialists do the calling. You decide what to do next.

Check My GLP-1 Coverage with Ro — Free →Best for visits billed to insurance: Amazon One Medical, Form Health, knownwell, PlushCare, Found

Amazon One Medical (the new 2026 path)

Amazon One Medical launched a dedicated GLP-1 management program in 2026 that integrates primary care, prescription, and Amazon Pharmacy fulfillment into a single workflow.

- You don't need an Amazon One Medical membership to schedule the GLP-1 program visit

- Insurance is billed for the scheduled GLP-1 program visit; copays/deductibles apply

- Accepts most major commercial plans, Original Medicare, Medigap, and select Medicare Advantage plans (per onemedical.com/insurance, April 2026) — verify your specific plan

- Amazon Pharmacy offers Same-Day Delivery to roughly 3,000 cities (expanding to ~4,500 by end of 2026), with insurance pricing for Wegovy and Foundayo starting as low as $25/month for eligible patients

Best for: Anyone who wants the cleanest "primary care + pharmacy + insurance" experience in 2026 and lives in an Amazon Pharmacy delivery zone. Limitation: Newest entry on our list — state availability and plan acceptance still expanding.

Form Health

Form Health is the obesity-medicine specialty option. Their care team is led by board-certified obesity-medicine clinicians, and they accept most major private insurance and Medicare — a rare combination in this category.

- Covered by national health insurance plans including Medicare

- Submits prior authorization paperwork for Wegovy and Zepbound when prescribed

- Does not ship medication; sends prescriptions to your pharmacy

- Does not accept Medicaid for program costs

- Self-pay $299/month if insurance doesn't cover the program

Best for: Medicare beneficiaries who want obesity-medicine specialists, or commercially insured readers who want a longer-term doctor-patient relationship rather than a transactional experience.

knownwell

knownwell offers nationwide telehealth and accepts most major commercial plans plus Medicare. They publish an 80% prior-authorization approval rate on their referral page (per knownwell.co/referral, April 2026) — a useful number if you're nervous about the PA process.

- Accepts most major commercial insurance plans and Medicare nationwide

- Accepts Medicaid in some states (verify your state)

- Has a dedicated prior authorization team

- Cash-pay self-pay paths available: $299 first visit, $149 follow-up

Best for: Adults who want true in-network clinical care across both commercial insurance and Medicare, with a published PA track record.

PlushCare

PlushCare is the most "regular doctor" of the bunch — a virtual primary-care platform owned by Accolade (NASDAQ: ACCD), in-network with most major commercial insurers including Aetna, Cigna, UnitedHealthcare, Anthem/BCBS, and Humana.

- $19.99/month membership + visit copay

- Care team submits prior authorization for branded GLP-1s

- PA review may take 7–14 days after submission

- Prescriptions go to your local pharmacy — lets you stack manufacturer savings cards directly at the counter

- Lab work required every 6 months; not included in membership

Found

Found offers a free GLP-1 insurance checker (per joinfound.com/glp1-checker, April 2026) and supports both branded and cash-pay paths depending on your coverage. Found contacts your insurance, sends a medication-by-medication coverage report, and provides PA documentation support when applicable.

Best for: Adults who want one provider that flexes between branded-with-insurance and cash-pay-without. Limitation: Carrier acceptance varies — verify your specific plan with Found before enrolling.

Real total monthly cost with PlushCare and insurance (worked example)

| Scenario | Month 1 | Ongoing |

|---|---|---|

| Commercial plan covers Wegovy, $30 visit copay + $25 med copay | $19.99 + $30 + $25 = ~$75 | $19.99 + $25 = ~$45/mo (visits less frequent after titration) |

| Commercial plan covers Zepbound, $30 + $50 | ~$100 | ~$70/mo |

| Plan doesn't cover GLP-1s | $19.99 + visit + $300–$1,500 med = expensive | Use Ro's free coverage check first; if truly excluded, compare cash-pay FDA-approved paths |

Not sure which insurance-billed provider fits your plan and state?

Tell us your insurance type, state, and goals. Get a personalized provider match in 60 seconds.

Best with a structured lifestyle program: WeightWatchers Clinic Med+

- $25/month for first two months, then $74/month for remainder of a 12-month plan

- FDA-approved medications only (Wegovy, Saxenda, Zepbound)

- Insurance coordinator works directly with your plan to maximize coverage and submit PA paperwork

- Lifestyle program included — WW's behavioral system backed by 60+ years of science

- GLP-1 medication cost is not included in membership

Best for: Adults who explicitly want a structured lifestyle program alongside their medication and plan to stay enrolled for at least 12 months.

Sesame Care: branded provider choice + Costco self-pay pricing

- Success by Sesame from $59/month with annual subscription; per-visit marketplace also available

- Branded formulary includes Wegovy® (pill and injection), Zepbound®, Ozempic®, Mounjaro®, Foundayo™, and Rybelsus

- Costco Member Prescription Program self-pay pricing available for Ozempic and Wegovy for Costco members

- Insurance is accepted for the medication itself at your pharmacy

| When Sesame beats Ro | When Ro beats Sesame |

|---|---|

|

|

Pick your own provider. Costco-member self-pay pricing on Wegovy and Ozempic available.

Compare Branded GLP-1 Pricing on Sesame Care →Mochi Health, Hims, Hers, Walgreens, CVS, and Walmart: where they fit

Several big-name brands appear in GLP-1 search results but don't fit the "accepts insurance" intent the way the providers above do. Here's the honest breakdown so you don't waste a click.

Mochi Health

$79/month subscription that supports both insurance/PA for prescribed branded medications and prominently features compounded cash-pay options on its pricing pages. Accepts HSA/FSA with letter of medical necessity. If your goal is a branded medication covered by insurance, Mochi will help with PA — but think of it as a hybrid program rather than an insurance-first one. Medicare acceptance: verify directly with Mochi.

Hims and Hers

Following the March 2026 partnership with Novo Nordisk, both platforms now offer FDA-approved Wegovy® pill, Wegovy® pen, and Ozempic® at direct-to-consumer pricing. They don't bill insurance for visits and don't run a traditional insurance concierge for prior authorization. Use Hims/Hers if you've decided to pay cash and want a familiar consumer brand. Use Ro if you want to fight for coverage first.

Walgreens Weight Management

Walgreens explicitly states it does not currently handle insurance or prior authorizations for GLP-1s. It's a cash-pay path with manufacturer-savings-card pricing. Useful if you're paying out of pocket; not the right answer if you're searching for insurance coverage.

CVS MinuteClinic

Prescribes FDA-approved GLP-1s when clinically appropriate, but the medication itself may not be covered by insurance under their workflow. State availability varies. Local-clinic alternative for people who want a pharmacy-adjacent path; not in our top tier for insurance intent.

Walmart Better Care

Marketplace model connecting you to third-party providers. Insurance support varies by which clinician you end up with. The current Curai promotion excludes Medicare and Medicaid users.

The pattern here: these are real options for the right reader, but they're the wrong answer if your search intent is specifically "GLP-1 providers that accept insurance" the way most readers mean it.

How insurance covers Wegovy, Zepbound, Ozempic, Mounjaro, and Foundayo

Wegovy® (semaglutide injection and pill)

FDA-approved for chronic weight management. The Wegovy pill is the first oral GLP-1 approved for weight loss. Coverage depends on plan formulary, BMI documentation, comorbidities, and lifestyle-program participation. Also FDA-approved to reduce cardiovascular event risk in eligible patients — which sometimes opens an alternative coverage pathway.

Manufacturer savings: Through Aug. 31, 2026, Novo Nordisk offers Wegovy oral to eligible self-pay patients at $149/month for the 1.5 mg and 4 mg doses (with restrictions). Through December 31, 2026, eligible new self-pay patients can get the first two fills of Wegovy injectables at $199/month for 0.25 mg and 0.5 mg doses. Government insurance beneficiaries are not eligible.

Zepbound® (tirzepatide injection)

FDA-approved for chronic weight management and additionally for moderate-to-severe obstructive sleep apnea in adults with obesity. The OSA indication matters: it can be a covered Part D benefit even when weight-loss-only is excluded — making Zepbound viable for some Medicare beneficiaries with sleep apnea.

Manufacturer savings: Through Dec. 31, 2026, eligible self-pay patients can get Zepbound 7.5–15 mg KwikPen (or vials) at $449 each. Verify at LillyDirect.

Ozempic® and Mounjaro® (semaglutide and tirzepatide injections)

FDA-approved for type 2 diabetes — not weight loss. Many insurance plans cover them for diabetes, often with prior authorization. Plans rarely cover them for weight loss alone. Don't assume off-label coverage; verify.

Foundayo™ (orforglipron)

The newest entry. FDA-approved April 1, 2026 for chronic weight management in adults with obesity or overweight with a weight-related condition. Foundayo is the first once-daily oral GLP-1 receptor agonist for weight loss without the strict empty-stomach restrictions of oral semaglutide. Coverage on commercial plans is still building out — check your plan or use Ro's coverage checker.

Rybelsus® (oral semaglutide)

FDA-approved for type 2 diabetes; label expanded in 2025 for cardiovascular risk reduction in high-risk patients with type 2 diabetes. Coverage typically follows diabetes-medication patterns. Has strict empty-stomach dosing requirements that Foundayo does not.

Saxenda® (liraglutide)

FDA-approved for chronic weight management. Older generation, less potent than semaglutide or tirzepatide. Sometimes covered when newer GLP-1s aren't — particularly through step-therapy requirements.

Compounded semaglutide and tirzepatide

Compounded GLP-1 medications may be prepared by licensed U.S. compounding pharmacies when federal and state conditions are met. They are not FDA-approved finished products. They are not generic drugs. The FDA does not review them for safety, effectiveness, or quality before marketing. Compounded GLP-1s are generally cash-pay.

Recency note: On April 30, 2026, the FDA proposed excluding semaglutide, tirzepatide, and liraglutide from the 503B bulk-drug-substances list, which would curb mass compounding. Comments remain open before any final rule. This may meaningfully shift the compounded landscape over the next several months.

Prior authorization explained (and who actually handles it for you)

What happens during prior authorization

- Benefits verification. Your provider's team reads your plan's fine print to see whether your medication is covered automatically or requires PA.

- Documentation submission. They submit a packet including: diagnosis with right ICD-10 code, BMI with date, comorbidities, prior treatment history, labs if requested, and a letter of medical necessity.

- Insurer review. Your plan's pharmacy benefit manager reviews the request against the plan's clinical criteria.

- Decision returned. Approval, denial, or request for additional information. Approvals typically last 6–12 months before reauthorization is needed.

How long PA actually takes

| Path | Realistic timeline |

|---|---|

| Through a concierge service (Ro) | ~2–3 weeks end-to-end (per ro.co) |

| Through a PA-supporting telehealth (PlushCare) | 7–14 days after submission, longer if documentation is incomplete |

| DIY through your own doctor's office | Often 2–6 weeks due to back-and-forth |

| With a denial and appeal | Add 1–4 weeks |

What "submits PA on your behalf" actually means

There's a real difference between these three levels of support:

- "We'll provide you a PA form" — you do the work; many providers stop here

- "Our team submits the PA on your behalf" — the provider's team prepares and files the packet

- "Our concierge handles benefits verification, PA submission, and works on your behalf if there are coverage issues" — Ro's published model

Look for the third version. It's the level of support that actually saves you time.

Get a head start — find out if you're covered before you pay for care.

Get a Free Ro Coverage Check →Medicare, Medicaid, FEHB, and TRICARE: the government-plan paths

Medicare GLP-1 Bridge (the new path, starting July 1, 2026)

The Centers for Medicare & Medicaid Services has announced the Medicare GLP-1 Bridge — a demonstration program providing eligible Medicare Part D beneficiaries access to certain GLP-1 drugs from July 1, 2026 through December 31, 2027 (per cms.gov, April 2026).

- Central processor: Humana, the existing administrator of Medicare's LI NET program

- Medications: Foundayo, Wegovy injection, Wegovy tablets, and Zepbound KwikPen

- Pharmacies collect a $50 copay from eligible beneficiaries at point of dispense

- PA criteria include BMI ≥35, or BMI ≥30 with specified weight-related conditions, or BMI ≥27 with specified conditions

- This is a demonstration — not a permanent benefit expansion

Verify current rules at cms.gov before relying on this. The program is new, eligibility is specific, and details may evolve.

Medicaid

Per KFF analysis (January 2026), 13 state Medicaid programs covered GLP-1s for obesity treatment under fee-for-service. The landscape is evolving, with some states eliminating coverage and others reinstating it. Coverage for diabetes and other FDA-approved indications is more consistent.

The CMS BALANCE Model is a separate CMS model relevant to Medicaid GLP-1 access. CMS has stated coverage under BALANCE can begin as early as May 2026, but participation depends on state, manufacturer, and beneficiary eligibility.

Which providers accept Medicare for GLP-1 care

| Provider | Medicare? | Notes |

|---|---|---|

| Form Health | ✅ Yes | National coverage; obesity-medicine specialists; submits PA |

| knownwell | ✅ Yes | Nationwide telehealth + Medicare; published 80% PA approval rate |

| Amazon One Medical | ✅ Original Medicare, Medigap, select Medicare Advantage | Verify your specific plan |

| PlushCare | ⚠️ Limited | Stopped Medicare Part B as of January 1, 2026; some Medicare Advantage may still apply |

| Ro | ❌ No | Ro states its concierge cannot coordinate government insurance plans |

| Mochi Health, Hims/Hers | ❌ Limited | Not built for Medicare |

FEHB and TRICARE / VA

FEHB plan coverage of GLP-1s varies by carrier and plan. Many FEHB plans do cover GLP-1s for weight management with prior authorization. Ro has explicitly mentioned support for FEHB members through its concierge.

For TRICARE or VA pharmacy benefits, confirm directly with your benefits coordinator before enrolling with any telehealth provider — this is a category where the wrong provider choice creates the most friction.

On Medicare?

See our dedicated guide for Medicare beneficiaries seeking GLP-1 coverage.

Read Our Medicare GLP-1 Guide →What to do if your insurance denies your GLP-1 prior authorization

Path 1 — Appeal the denial

If the denial reason is missing documentation or insufficient clinical justification, your provider can submit an appeal with additional records. Internal appeals come first, then external review. Ro's insurance concierge supports coverage paperwork and resubmission for Ro Body members. Form Health, knownwell, PlushCare, and WW Clinic Med+ also support PA documentation and resubmission.

Path 2 — Request a formulary exception

If your plan explicitly excludes weight-loss medications, an appeal won't help — you need a formulary exception. Your prescriber submits a letter of medical necessity arguing the medication is uniquely required. Some plans allow exceptions for Wegovy when prescribed for cardiovascular event reduction, even if standard weight-loss coverage is excluded.

Path 3 — Switch to a covered GLP-1

Sometimes Wegovy is denied but Zepbound is covered, or vice versa. Sometimes neither weight-loss GLP-1 is covered but Ozempic is covered for diabetes if that's your indication. Foundayo is the newest FDA-approved option (April 1, 2026) and may have different formulary status — worth asking about.

Path 4 — Pivot to cash-pay

If insurance is genuinely a dead end, the cleanest cash-pay paths in 2026 are:

- Manufacturer programs — NovoCare for Wegovy ($149/month lowest doses through Aug. 31, 2026 with restrictions), LillyDirect / TrumpRx pricing for Zepbound and Foundayo. Government insurance beneficiaries usually aren't eligible.

- Ro's cash-pay match — Ro states it matches LillyDirect, NovoCare, and TrumpRx pricing on FDA-approved branded medication. Simplest one-stop cash-pay branded path.

- Sesame Care — Branded provider choice; Costco Member Prescription Program self-pay pricing on Ozempic and Wegovy for Costco members.

- Compounded alternatives — A legitimate path for some readers, but a separate decision. See our best self-pay GLP-1 programs guide.

Get a free Ro coverage check before you assume you're denied. If you're not covered, Ro will show you the cash-pay alternatives at manufacturer-match pricing.

Get a Free Ro Coverage Check →Documents to gather before your insurance visit or coverage check

This is the practical checklist we wish more pages handed out. Screenshot it or copy it into your notes app before you talk to any provider.

Your insurance details

- Insurance card (front and back)

- Member ID / subscriber ID

- Group number

- Plan name

- Pharmacy benefit manager (PBM)

- RX BIN, RX PCN, RX Group (printed on most cards)

Your medical information

- Current weight and height (with date)

- BMI documented within the last 6–12 months

- Relevant diagnoses (T2D, hypertension, sleep apnea, MASH, CVD, PCOS, etc.)

- Current medications (especially prior weight-loss medications)

- Known contraindications (MTC history, MEN2, pancreatitis, pregnancy)

- Recent labs if available (A1C, CMP, lipid panel, thyroid)

Your prior treatment history

- Documented lifestyle change attempts (date, duration, outcome)

- Other weight-loss medications tried and outcome

- Behavioral or weight-management program participation (WW, Noom, in-person clinic)

- Bariatric surgery history if applicable

Questions to ask the provider before you pay

- Do you bill the medical visit to my insurance, or is your membership cash-pay?

- Do you submit prior authorization on my behalf, or do you provide me a form to submit?

- Do you support PA resubmission and appeals?

- Where will my prescription be sent?

- What happens if my insurance denies coverage?

- What's your refund policy if I cancel before my prescription is filled?

Compounded GLP-1s and insurance: the honest answer

- Compounded GLP-1 medications are generally cash-pay and not on commercial insurance formularies. Don't expect insurance to cover them.

- HSA and FSA cards are usable at many compounded providers as a payment method — but that's not the same as insurance coverage.

- The FDA has issued warning letters to multiple GLP-1 telehealth companies for misleading marketing about compounded products, including implying sameness with FDA-approved medications.

- The April 30, 2026 FDA proposal to exclude semaglutide, tirzepatide, and liraglutide from the 503B bulk-drug-substances list could curb mass compounding if finalized.

If your insurance won't cover any branded GLP-1 and you've evaluated the manufacturer programs above and the price gap is still meaningful, compounded is a legitimate alternative for some readers — but it's a different decision. For that lane, see our best self-pay GLP-1 programs guide.

Decision tree: which provider matches your situation

START → Do you have any health insurance?

│

├─ COMMERCIAL INSURANCE

│ ├─ Don't know if your plan covers GLP-1s?

│ │ → RO (free coverage check) or FOUND (free checker)

│ ├─ Want visits billed to insurance + Amazon Pharmacy?

│ │ → AMAZON ONE MEDICAL

│ ├─ Want a virtual PCP + retail pharmacy?

│ │ → PLUSHCARE

│ ├─ Want clinical depth + obesity specialists?

│ │ → FORM HEALTH

│ ├─ Want nationwide in-network + published PA approval rate?

│ │ → KNOWNWELL

│ ├─ Want lifestyle program + insurance coordinator?

│ │ → WW CLINIC MED+

│ └─ Want hybrid branded + compounded fallback?

│ → MOCHI HEALTH

│

├─ MEDICARE (traditional or Advantage)

│ ├─ Want obesity-medicine specialists? → FORM HEALTH

│ ├─ Want nationwide in-network telehealth? → KNOWNWELL

│ └─ Want primary care + Amazon Pharmacy? → AMAZON ONE MEDICAL

│

├─ MEDICAID

│ └─ Verify your state's coverage rules →

│ 13 state Medicaid programs covered GLP-1s for obesity

│ treatment under fee-for-service as of January 2026 (KFF)

│

└─ NO INSURANCE / PLAN EXCLUDES GLP-1s

├─ Want branded med at manufacturer-match pricing?

│ → RO (cash-pay) or SESAME CARE

├─ Want lifestyle program + cash-pay? → WW CLINIC MED+

├─ Costco member?

│ → SESAME CARE (Costco self-pay pricing on Ozempic, Wegovy)

└─ Open to compounded medication? → see our self-pay guideStill not sure which path is right for you?

Tell us your insurance, state, medication preference, and budget. Get the right provider for your situation in 60 seconds.

How we verified and ranked these GLP-1 providers

Our methodology

- Read every provider's official insurance, pricing, and FAQ pages for current April 2026 language.

- Cross-referenced FDA and CMS sources for medication approvals, the Medicare GLP-1 Bridge, and Medicaid policy direction.

- Used Reddit and forum threads only for understanding user friction language — not for medical, safety, or regulatory claims.

- Mapped each provider against four insurance models (visit billing, medication PA, both, neither) to remove ambiguity.

- Calculated realistic total-monthly-cost-with-insurance ranges for providers where the math could be reasonably illustrated.

- Stamped a verified date on the page so you can tell when this was last checked.

Our scoring framework (Insurance Usefulness Score)

| Factor | Weight |

|---|---|

| Clarity of visit insurance billing | 20% |

| Medication coverage support / coverage checker | 20% |

| Prior authorization support quality | 20% |

| Government-plan clarity | 10% |

| Transparent pricing and cash-pay fallback | 15% |

| Current FDA-approved medication availability | 10% |

| Honesty about limitations | 5% |

FAQ

Which GLP-1 providers accept insurance?

Several do, but in different ways. For commercial insurance with prior authorization help, the strongest options are Ro (cash-pay membership + dedicated medication concierge), Amazon One Medical (visits billed to insurance), Form Health (Medicare + commercial), knownwell (Medicare + commercial nationwide telehealth), PlushCare (in-network commercial), and Found (free coverage checker + flexible insurance/cash hybrid). Sesame Care, WeightWatchers Clinic Med+, and Mochi Health round out our list.

Does Ro accept insurance for GLP-1?

Ro doesn't bill insurance for visits, but Ro's insurance concierge submits prior authorization for FDA-approved GLP-1 medications on your behalf and works to resubmit if there are coverage issues. If your commercial plan covers the medication, your out-of-pocket can drop to a copay. Ro membership is $39 the first month, then $149/month — or as low as $74/month with annual prepay. Ro doesn't coordinate government insurance plans.

Does Amazon One Medical accept insurance for GLP-1 visits?

Yes for the scheduled GLP-1 management program — visits can be billed to insurance, and the program publishes insurance and prior-authorization support. Amazon Pharmacy compares insurance and cash pricing at checkout. Note: Amazon One Medical's On-Demand care is a separate path that does not accept insurance for the visit and is intended for prescription renewals, not new GLP-1 prescriptions.

Does PlushCare handle GLP-1 prior authorization?

Yes. PlushCare's care team submits prior authorization on your behalf for branded GLP-1 medications. PA review may take 7–14 days after submission. PlushCare is in-network with most major commercial insurers including Aetna, Cigna, UnitedHealthcare, Anthem/BCBS, and Humana. Membership is $19.99/month plus your visit copay. PlushCare stopped accepting Medicare Part B as of January 1, 2026.

Does Form Health accept Medicare?

Yes. Form Health is covered by national health insurance plans including Medicare. Their care team includes board-certified obesity-medicine clinicians, and they submit prior authorization for Wegovy and Zepbound. Form Health does not accept Medicaid for program costs. Self-pay is $299/month if insurance does not cover the program. Form Health does not ship medication; prescriptions go to your pharmacy.

Does knownwell accept Medicaid?

knownwell accepts Medicaid in some states — verify with your state. They accept most major commercial plans and Medicare nationwide. knownwell publishes an 80% prior authorization approval rate on their referral page.

Does Sesame Care accept insurance for GLP-1 medications?

Sesame Care says insurance is accepted for weight-loss medications. Sesame's Success by Sesame online weight-loss program is available from $59/month with annual subscription, with per-visit pricing also available through the marketplace. Costco members can use the Costco Member Prescription Program self-pay pricing on Wegovy and Ozempic.

Are compounded GLP-1 medications covered by insurance?

Compounded GLP-1 medications are generally cash-pay and not on commercial insurance formularies. They may be prepared by licensed U.S. compounding pharmacies when federal and state conditions are met, but they are not FDA-approved finished products. Some compounded providers accept HSA or FSA cards as a payment method, but the medication itself is paid out of pocket.

Can insurance cover Wegovy or Zepbound for weight loss?

Sometimes. Coverage depends on your plan's formulary, your BMI and comorbidities, and whether your plan excludes weight-loss medications. About 19% of large employer firms (200+ workers) covered GLP-1s for weight loss in their largest health plan in 2025, per the Peterson-KFF Health System Tracker. Wegovy may have an alternative coverage pathway through its FDA approval for cardiovascular event reduction; Zepbound may have one through its FDA approval for moderate-to-severe obstructive sleep apnea.

Does Medicare cover GLP-1 for weight loss in 2026?

Medicare does not currently cover GLP-1 medications when prescribed solely for weight loss. Medicare Part D covers GLP-1s for FDA-approved indications other than weight loss, including type 2 diabetes, cardiovascular event reduction (Wegovy), and moderate-to-severe obstructive sleep apnea (Zepbound). The CMS Medicare GLP-1 Bridge demonstration runs from July 1, 2026 through December 31, 2027, with a $50/month copay for eligible Part D beneficiaries who meet specified BMI and clinical criteria. Verify current rules at cms.gov.

What if my insurance denies my GLP-1 prior authorization?

You have four options: (1) appeal the denial with additional documentation, (2) request a formulary exception, (3) try an alternative GLP-1 your plan covers, or (4) pivot to cash-pay using manufacturer programs (NovoCare, LillyDirect) or Ro's price-match. Providers like Ro, Form Health, knownwell, and PlushCare can help you navigate the first three.

How long does GLP-1 prior authorization take?

When documentation is complete, prior authorization typically returns in 5–10 business days. Through a concierge service like Ro's, the end-to-end timeline is usually 2–3 weeks. PlushCare states PA review may take 7–14 days. Going through your own doctor's office often takes 2–6 weeks due to back-and-forth.

Can I use HSA or FSA funds for GLP-1 care?

Often yes for the medication portion. Many providers accept HSA/FSA cards directly — including PlushCare, Form Health, Mochi, Found, and most compounded providers. Ro states it does not accept HSA/FSA cards at this time. Hims and Hers reference HSA/FSA eligibility on certain product pages — verify per product before checkout.

The bottom line

If your commercial insurance might cover a GLP-1, the strongest first move is Ro's free coverage check — let their concierge call your insurer, get the report by email, and then decide. If you're on Medicare, route to Form Health, knownwell, or Amazon One Medical. If you want visits billed to insurance specifically, Amazon One Medical, Form Health, knownwell, PlushCare, or Found are your strongest options. If you want a behavioral program alongside medication, WW Clinic Med+ is purpose-built for that. If your plan won't cover any of it, the cleanest cash-pay paths are manufacturer programs (NovoCare, LillyDirect) or Ro's price-match before you consider compounded.

You don't need permission to start. You need the right starting point. That's what this page is for.

Run Ro's Free GLP-1 Insurance Coverage Check →Free. No prescription required. Personalized coverage report by email. Best first step for commercial insurance.

Still not sure which GLP-1 program is right for you?

Take our free 60-second matching quiz →Authorship, sources, and disclosures

By the Weight Loss Provider Guide Editorial Team. Weight Loss Provider Guide is an independent comparison resource for GLP-1 telehealth providers.

Last verified: April 30, 2026. We re-verify pricing and insurance language monthly, and update immediately on major FDA or CMS changes.

How this guide was produced: We reviewed each provider's official pricing, insurance, and FAQ pages, plus FDA and CMS published policies and KFF analyses (Peterson-KFF Health System Tracker; KFF Medicaid). Reddit and forum threads were used only for understanding user language and objections — not for medical, safety, or regulatory claims. Patient comments cited from provider sites are provider-published; they are not proof of typical medical results, and individual outcomes vary.

Affiliate disclosure: We may earn a commission when readers enroll with providers through links on this page, at no additional cost to readers. Several providers featured in this guide (Amazon One Medical, Form Health, knownwell, PlushCare, Found) are not our affiliate partners — we include them when they're the right answer for the search intent, regardless of whether we make money on the recommendation. Our editorial scoring and rankings are not influenced by affiliate relationships.

Medical disclaimer: This page is for informational purposes only and does not constitute medical advice. Always consult a licensed healthcare provider before starting any treatment. Compounded medications referenced on this page are not FDA-approved as finished products. Insurance coverage policies change frequently — verify directly with your insurer and your provider before enrolling.

Primary sources: Ro (ro.co/weight-loss/pricing, /insurance, /glp1-insurance-checker, /coverage-checker-report, /foundayo); Amazon One Medical (health.amazon.com, aboutamazon.com, onemedical.com/insurance); Form Health (formhealth.co); knownwell (knownwell.co, knownwell.co/referral); PlushCare (plushcare.com/weight-loss, plushcare.com/glp-1-prescription); Sesame Care (sesamecare.com/service/online-weight-loss-program); WeightWatchers Clinic (weightwatchers.com/us/weight-loss-medication); Mochi Health (joinmochi.com); Found (joinfound.com/glp1-checker); Hims (investors.hims.com); Walgreens (walgreens.com/topic/virtual-healthcare/weight-loss); FDA (fda.gov/news-events/press-announcements); CMS (cms.gov/medicare/coverage/prescription-drug-coverage/medicare-glp-1-bridge, cms.gov/priorities/innovation/innovation-models/balance); NovoCare (novocare.com); LillyDirect (lillydirect.com); Peterson-KFF Health System Tracker (healthsystemtracker.org); KFF (kff.org/medicaid/medicaid-coverage-of-and-spending-on-glp-1s); Reuters (April 30, 2026 FDA compounding proposal coverage).